Important facts

- What is ESG reporting?

- ESG reporting is the structured disclosure of corporate measures and ESG indicators relating to the environment, social issues and good corporate governance.

- Why is ESG reporting important?

- It fulfills legal requirements, meets the expectations of investors and business partners and forms the basis for credible sustainability communication.

- What is reported in an ESG report?

- Environmental data such as CO₂ emissions, social factors such as working conditions and governance issues such as compliance and supervisory structures are reported.

- Which companies are obliged to report on ESG?

- Currently mainly large companies, since 2025 increasingly also SMEs due to the extended CSRD.

- What standards are there for ESG reporting?

- The most common standards are GRI, ESRS, SASB, TCFD as well as ISO standards and the VSME standard specifically for small and medium-sized enterprises.

- What are the benefits of ESG reporting?

- Companies benefit from a better market position, easier access to sustainable financing and a stronger reputation.

- What challenges does ESG reporting entail?

- The biggest hurdles are the high data requirements, the need for clear processes and digital tools, and the complexity of selecting and applying the right standards.

Abstract

ESG reporting refers to structured reporting on a company's performance in the areas of the environment, social affairs and corporate governance. It has been legally binding for many companies in the EU since 2024 - regulated by the Corporate Sustainability Reporting Directive (CSRD). Not everything has to be reported, but only what is material. The basis for this is a clean materiality analysis according to the principle of double materiality.

The standards that apply depend on the regulatory framework. The European Sustainability Reporting Standards (ESRS) are binding for companies subject to CSRD. In addition, internationally recognized frameworks such as GRI, SASB, TCFD or ISSB are used. The CSRD is flanked by the EU Taxonomy Regulation and the SFDR, which together form the EU framework for sustainable finance.

The effort is real, but it pays off. Companies that see ESG reporting not as a chore but as a strategic tool gain the trust of investors, access capital more easily and can talk credibly about their sustainability performance. Those who lay the foundations now will be better positioned tomorrow.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

ESG reporting: definition & objectives

ESG stands for Environmental, Social and Governance. These three areas form the basis for responsible corporate action and are now an integral part of modern corporate governance. Many companies in the EU have been required by law to report on them since 2024.

What is ESG reporting?

ESG reporting is about disclosing how a company acts in the areas of the environment, social affairs and corporate governance. This includes both: concrete figures such as CO₂ emissions or energy consumption, but also qualitative information. For example, which strategies are pursued, how processes are organized and who bears responsibility within the company.

ESG reporting makes it possible to measure how responsibly a company really acts.

An ESG report works in a similar way to a traditional annual report: it is aimed at investors, customers, business partners and supervisory authorities and creates a comprehensible basis for their decisions. The specific content that needs to be reported depends on the regulatory framework and a company-specific materiality analysis.

Why is ESG reporting important for companies?

For years, corporate reporting revolved almost exclusively around figures: Turnover, profit, growth. That is no longer enough today. Investors, customers and legislators want to know how a company does business and not just how much it earns. ESG reporting provides a structured answer to this.

Objectives of ESG reporting

Companies can openly communicate their efforts and progress in the areas of environment, social affairs and governance, both to investors and to the public.

In the EU, more and more companies are obliged to report on sustainability, including through the CSRD, the EU Taxonomy Regulation and the SFDR. Those who report at an early stage avoid fines and are prepared for future requirements.

Addressing ESG issues helps to identify potential environmental, social and governance risks at an early stage and counteract them in a targeted manner.

Investors and lenders are increasingly taking ESG criteria into account in their decisions. A detailed ESG report can increase the attractiveness of sustainable investments and enable more favorable financing conditions.

Companies that communicate ESG practices transparently can position themselves as responsible market participants and thus clearly differentiate themselves from the competition.

Who is obliged to report on ESG?

The sustainability reporting obligation does not apply equally to all companies. It was introducedgradually by the GRI andis currently being further adapted as part of EU simplification measures. An overview of the most important stages.

Mandatory according to NFRD (since 2017)

The Non-Financial Reporting Directive (NFRD) laid the foundation for mandatory sustainability reporting in the EU. Since reports on the 2017 financial year, large companies of public interest, including listed companies, banks and insurance companies, with more than 500 employees have been obliged to disclose non-financial information. However, with the European Green Deal and the goal of climate neutrality by 2050, these requirements were no longer sufficient. The CSRD therefore took their place. Find out more about CSRD reporting in detail.

New obligations under the CSRD

The Corporate Sustainability Reporting Directive (CSRD) significantly replaces and extends the NFRD. It obliges a growing number of companies to report in accordance with the European Sustainability Reporting Standards (ESRS) and also introduces an external audit requirement. The introduction will be staggered in three so-called waves.

Wave 1 - reporting obligation from 2024

Companies that were already subject to the NFRD will report in accordance with the CSRD and ESRS for the first time for the 2024 financial year. These reports are typically published in 2025.

Wave 2 - reporting obligation from 2027

Other large companies that were originally due to start earlier are not required to report until the 2027 financial year following the so-called "stop-the-clock" postponement. The first reports from this group will generally be published in 2028.

Wave 3 - reporting obligation from 2028

Listed SMEs and certain other categories of companies will not start until the 2028 financial year, with the first publication typically in 2029. Listed SMEs also had the option of opting out in the first two years of application.

Note:

The exact scope of application of the CSRD is currently being redefined as part of EU simplification measures. In future, the ESG reporting obligation will only apply to companies with more than 1,000 employees and a net turnover of more than 450 million euros. Companies should regularly check the current thresholds and deadlines.

Does the obligation also apply to SMEs?

In principle, small and medium-sized enterprises are initially exempt from the CSRD obligation, at least as a directly obligated party. In practice, however, many SMEs are also coming under pressure: large companies with a reporting obligation are increasingly required to disclose information from their supply chain and pass these requirements on to their suppliers and partners. For listed SMEs, the CSRD also provides for a separate reporting obligation from Wave 3 onwards. SMEs can voluntarily use the specially developed VSME standard, which enables simplified and proportional reporting.

What must an ESG report contain?

An ESG report documents how a company's activities affect the environment, society and its own corporate governance, both positively and negatively. The following applies: companies do not have to report everything, but only what is material. The basis for this is a clean materiality analysis that follows the principle of dual materiality. An issue is relevant if it either has a significant impact on people or the environment or if it involves significant financial risks or opportunities for the company.

The scope of an ESG report is not based on what is possible, but on what is essential.

The European Sustainability Reporting Standards (ESRS) provide the binding framework for companies that have to report in accordance with the CSRD. The content is structured along the three ESG areas:

Environment (Environmental)

The environmental section is the most extensive reporting area for most companies. It focuses on the impact of corporate activities on natural resources and the climate. Typical report contents are

- Climate change: greenhouse gas emissions (Scope 1, 2 and 3), climate risks and targets

- Energy consumption: total energy consumption, share of renewable energies

- Water & marine resources: water abstraction, consumption and discharge

- Biodiversity & ecosystems: Impacts on natural habitats

- Resources & circular economy: waste management, use of materials, recycling rates

- Environmental pollution: emissions to air, water and soil

The EU taxonomy information also plays a role for many companies: the extent to which economic activities are to be classified as taxonomy-eligible or taxonomy-compliant must be disclosed here - typically via key figures such as turnover, CapEx and OpEx shares.

For many companies, there is another aspect to consider: the EU taxonomy. This is specifically about what proportion of a company's own business activities can be classified as environmentally sustainable. This is indicated by key figures such as turnover, capital expenditure (CapEx) and operating expenditure (OpEx).

Social (Social)

The social area covers a company's relationships with its employees, with society and with people along the supply chain. Among other things, it reports on:

- Working conditions: Working hours, fair pay, health protection

- Diversity & equal opportunities: gender balance, anti-discrimination measures

- Training and further education: training courses, skills development

- Human rights: Compliance with human rights in our own operations and in the supply chain

- Community & social responsibility: commitment in the local environment, social impact

The supply chain in particular is increasingly coming into focus. Not least due to the Supply Chain Due Diligence Act (LkSG) and the CSDDD at EU level.

Corporate governance

Governance disclosures show how a company is managed internally and which structures ensure responsible action. Relevant topics are

- Business ethics & compliance: anti-corruption, whistleblowing mechanisms

- Supervisory and control structures: composition and tasks of the Management Board and Supervisory Board

- Remuneration policy: linking remuneration with sustainability targets

- Risk management: Dealing with ESG-related risks at management level

- Transparency & reporting processes: Responsibilities for ESG reporting in the company

Standards and frameworks at a glance

Anyone preparing an ESG report is faced with the question early on: Which standard do I follow? The good news is that there is no universally "wrong" framework. The choice depends on the size of the company, the industry and the regulatory framework. An overview of the most important standards:

Standards & frameworks in detail

The European Sustainability Reporting Standards (ESRS) are mandatory for all companies covered by the CSRD. The standards were developed by EFRAG on behalf of the European Commission and adopted as a delegated regulation on July 31, 2023. They were published in the EU Official Journal on December 22, 2023 and will apply to affected companies from January 1, 2024.

The ESRS cover a broad spectrum: from overarching topics such as strategy, governance and materiality to specific requirements in the areas of environment, social affairs and corporate management. They are not a rigid set of rules. They are continuously adapted and developed further in the course of the EU simplification measures.

The ESRS are not optional for companies subject to CSRD in the EU. They are the legally prescribed framework.

The Global Reporting Initiative, or GRI for short, is one of the most widely used frameworks for sustainability reporting worldwide. What makes it particularly practical is that its modular structure allows companies to combine universal standards with topic-specific requirements and thus tailor the report to their own situation.

- Suitable for companies of all sizes and industries

- Strong focus on environmental and social impact

- Widely used as a voluntary standard - also outside the EU

- Compatible with the ESRS, which facilitates combined use

The standards of the Sustainability Accounting Standards Board (SASB) are characterized by their industry-specific approach. SASB defines its own key figures for over 77 sectors, which are particularly relevant for investors.

- Focus on financial materiality from an investor perspective

- Particularly useful as a supplement to GRI or ESRS

- Now integrated under the umbrella of the IFRS Foundation

The TCFD framework was developed with a clear objective: To help companies disclose climate-related risks and opportunities in an understandable and comparable way. The reporting is divided into four core areas:

- Governance: How does the company monitor climate-related risks?

- Strategy: What impact will climate change have on the business model?

- Risk management: How are climate risks identified and managed?

- Key figures & goals: What metrics and goals does the company pursue?

The TCFD recommendations are largely incorporated into the ESRS. Anyone reporting in accordance with CSRD already fulfills many TCFD requirements automatically.

The UNGPRF is based on the UN Guiding Principles on Business and Human Rights and helps companies to structure their reporting on human rights due diligence. This is a topic that has become relevant for many companies at EU level since the LkSG and the CSDDD.

- Focus on human rights and social responsibility along the supply chain

- Particularly relevant for companies with an international supply chain

- Usefully complements other frameworks in the social reporting area

The special approach of the CDSB framework: climate-related and environmentally relevant information should not be reported separately, but should be incorporated directly into the traditional financial report. A sensible bridge between two worlds that have long reported separately.

- Focus on integration of environmental information in financial reports

- Closely dovetailed with TCFD recommendations

- Also transferred to the IFRS Foundation in the meantime

With IFRS S1 and IFRS S2, the ISSB has published two standards that are intended to make sustainability reporting comparable worldwide. While IFRS S1 covers general sustainability risks and opportunities, IFRS S2 deals specifically with climate-related disclosures - both together form the global frame of reference outside the EU.

- Reference standard for many markets outside the EU

- Closely based on TCFD recommendations

- Not automatically mandatory under EU law - the ESRS remain relevant for companies subject to CSRD

- Convergence between ESRS and ISSB standards is being actively promoted

Which framework is right for my company?

There is no one-size-fits-all answer here. The choice depends on several factors:

Important: Many frameworks overlap in terms of content. Those who report in accordance with ESRS often fulfill requirements from GRI, TCFD and ISSB at the same time.

Regulatory requirements

ESG reporting in the EU is not a voluntary instrument. It is underpinned by a binding set of rules. Three central sets of rules form the framework: the CSRD as a reporting obligation for companies, the EU Taxonomy as a classification system for sustainable economic activities and the SFDR as a transparency obligation for financial market participants. They complement each other and together pursue the overarching goal of the European Green Deal: climate neutrality in Europe by 2050.

The CSRD, EU Taxonomy and SFDR are not three independent directives. Together they form the EU framework for sustainable finance and their content is interlinked.

CSRD - Corporate Sustainability Reporting Directive

The CSRD is the central set of rules for sustainability reporting in the EU and is a real game changer. It replaces the previous NFRD and goes significantly further: more companies with a reporting obligation, more stringent requirements, binding standards.key points of the CSRD:

- Binding reporting standard: companies must report in accordance with the ESRS - a uniform framework developed by EFRAG

- Extended scope of application: significantly more companies than before are obliged to report - staggered in three waves (2024, 2027, 2028)

- External audit requirement: The sustainability disclosures must be audited externally - initially as part of a so-called limited assurance

- Digital provision: The reports must be made available digitally, including in ESEF format with taxonomy information

- Double materiality: companies must consider both financial risks and impacts on people and the environment

Note: The scope of application of the CSRD is currently being revised as part of EU simplification measures. In future, the obligation will only apply to companies with more than 1,000 employees and a net turnover of more than 450 million euros. Companies should regularly check the current thresholds.

Implementing CSRD compliance in your company - here's how!

EU taxonomy - What counts as "green" economic activity?

The EU taxonomy answers a simple but important question: when is an economic activity truly sustainable? The classification system creates a common language for companies, investors and financial market participants and is intended to ensure that capital flows specifically to where it has a sustainable impact.

The taxonomy evaluates economic activities on the basis of six environmental objectives:

- Climate protection

- Adaptation to climate change

- Sustainable use of water and marine resources

- Transition to a circular economy

- Prevention of environmental pollution

- Protection and restoration of biodiversity and ecosystems

An activity is considered taxonomy-compliant if it fulfills three conditions: It must make a significant contribution to at least one of the six environmental objectives, must not significantly harm any of the other objectives, known as the "Do No Significant Harm" principle, and must comply with basic minimum social standards.

In practice, this means that companies disclose the proportion of their activities that are taxonomy-compliant and taxonomy-compliant - typically using three key figures:

- Revenue share (taxonomy-eligible and -aligned revenue)

- CapEx share (capital expenditure)

- OpEx share (operating expenses)

The EU taxonomy is not a sustainability label. It is a tool for classifying economic activities in a transparent and comparable manner.

SFDR - Obligations for financial market participants

The SFDR is not aimed at companies in general, but specifically at financial market participants, i.e. banks, fund managers, insurance companies and investment advisors. They must disclose how sustainability risks are incorporated into their financial products and investment decisions. In short: anyone who manages or advises money must show how they deal with ESG risks.

Key points of the SFDR:

- Sustainability risks: Financial market participants must disclose how they incorporate sustainability risks into their investment decisions

- Adverse impacts (PAI): Major market participants are required to report the principal adverse sustainability impacts of their investments (Principal Adverse Impacts)

- Product classification: Financial products are divided into three categories - Article 6 (no sustainability objectives), Article 8 (environmental or social characteristics) and Article 9 (sustainable investments as an objective)

- Detailed disclosure requirements: The Regulatory Technical Standards (RTS) of the SFDR have been in force since January 1, 2023

The SFDR is not directly relevant for companies outside the financial sector, but it is indirectly relevant: companies that raise capital from investors subject to the SFDR must increasingly provide ESG data that fulfills their disclosure obligations.

Preparation of an ESG report

Creating an ESG report is not a project that can be implemented overnight. It takes time, resources and a clear structure. The following guide will take you step by step through the entire process - from initial planning to continuous improvement.

A solid ESG report is not created single-handedly. It requires the cooperation of several departments and careful preparation.

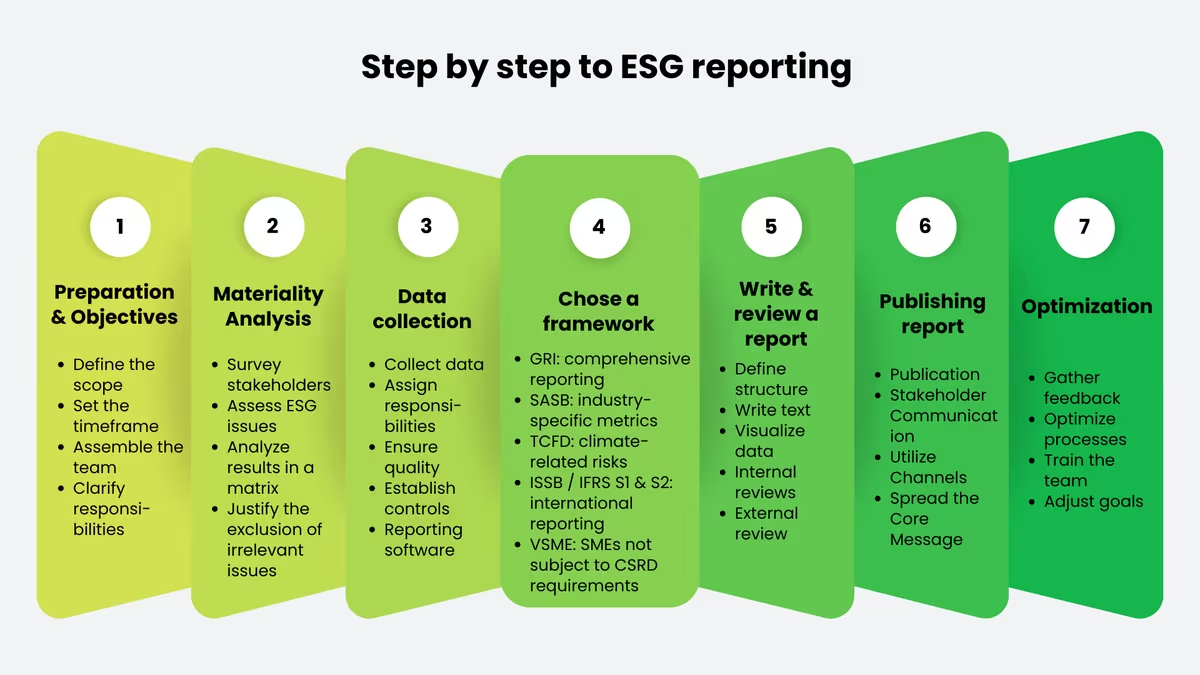

Step-by-step instructions

Before the first key figure is collected, a clear basis is needed. First define the objectives of your ESG reporting: is it primarily about regulatory compliance, transparency towards investors or the internal management of sustainability measures? This question will largely determine how extensively and in what form you report.

Important preparatory steps:

- Determine the scope of the report: Which divisions, locations and subsidiaries are included?

- Define the reporting period: As a rule, the past financial year

- Put together an interdisciplinary team: Sustainability, compliance, finance, HR and communications should be involved from the outset

- Clarify responsibilities: Who is responsible for which area, who has overall responsibility?

The materiality analysis is at the heart of every ESG report. It determines which topics a company must report on and which not. For companies subject to CSRD, the principle of double materiality applies: a topic is reportable if it either has a material impact on people or the environment or represents material financial risks or opportunities for the company.

A clean materiality analysis is the basis for a robust ESG report and at the same time protects against unnecessary reporting effort.

Procedure in practice:

- Identify and interview internal and external stakeholders

- Evaluate relevant ESG issues from a corporate and stakeholder perspective

- Document results in a materiality matrix

- Justify decisions on non-material topics in a comprehensible manner

The relevant data is collected on the basis of the materiality analysis. In practice, this is often the most time-consuming phase, especially for companies with complex supply chains or multiple locations.

- Identify data sources: Energy consumption, emissions data, HR key figures, supplier information, etc.

- Designate data controllers: Who supplies which data from which system?

- Ensure quality: Check data for completeness and plausibility

- Establish internal controls: Introduce the dual control principle and clear approval processes

- Use ESG reporting software: Digital tools can significantly simplify data collection, management and analysis and reduce sources of error

Reliable data management systems are not an optional extra. They are the prerequisite for an audit-proof ESG report.

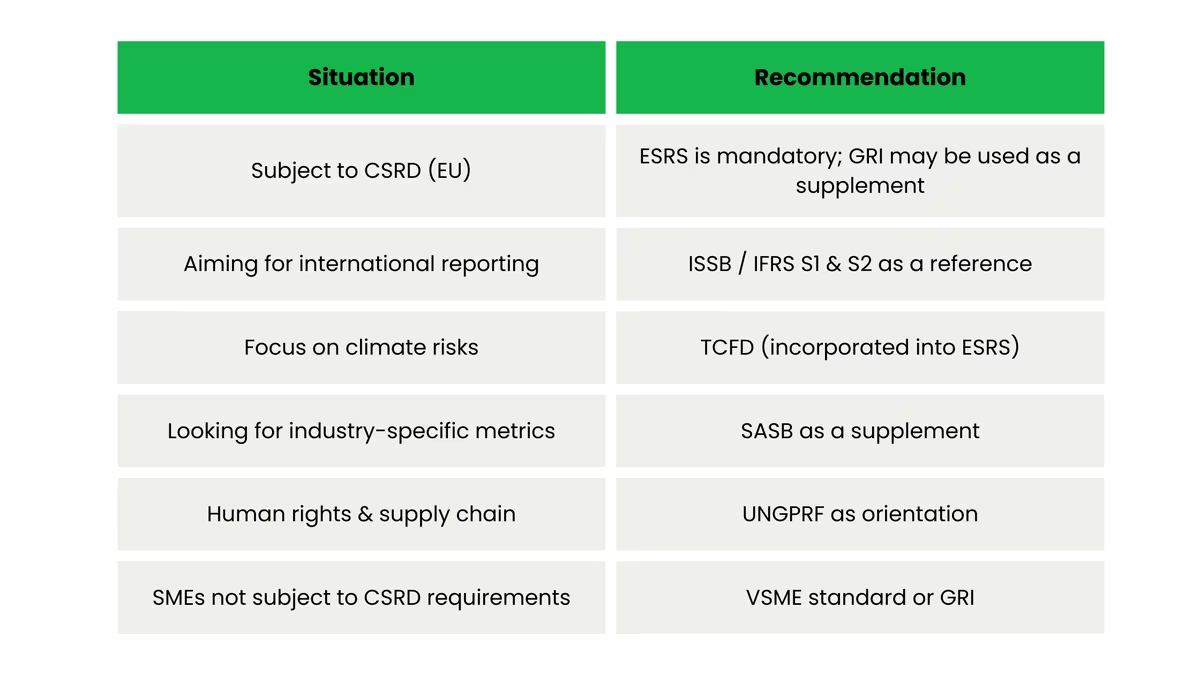

Once the key topics and indicators have been determined, select the appropriate reporting framework. The ESRS are binding for companies subject to CSRD in the EU. In addition, it may be useful to use proven international frameworks:

- GRI: For broad, stakeholder-oriented reporting

- SASB: For industry-specific, investor-relevant key figures

- TCFD: For a structured disclosure of climate-related risks

- ISSB / IFRS S1 & S2: When international reporting is required

- VSME: For SMEs without a direct CSRD obligation

There is no such thing as the wrong framework. The decisive factor is that the choice fits the size of the company, the industry and the expectations of the stakeholders.

With the data collected and the framework selected, it is time to prepare the actual report. Structure the report clearly along the ESG areas and ensure that the language used is understandable and appropriate for the target group.

What is important for the creation:

- Define structure: Company profile, ESG strategy, materiality analysis, thematic content and key figures

- Writing texts: Qualitative information on strategies, processes and measures

- Visualize data: Clearly prepare tables, graphs and key figures

- Internal review: Obtain feedback from specialist departments and management

- External audit: External limited assurance is mandatory for companies subject to CSRD - coordinate with the auditor at an early stage

The external audit is not a tiresome compulsory program. It significantly strengthens the credibility of the report and the trust of stakeholders.

The value of a completed ESG report only unfolds when it reaches the right target groups. You should therefore plan publication and communication at an early stage.

- Publication: Make the final report easy to find on the company website - for companies subject to CSRD also in ESEF format

- Stakeholder communication: actively communicating important results to investors, customers and partners

- Use communication channels: Press releases, social media, newsletters and investor presentations are suitable depending on the target group

- Work out key messages: What are the key advances and goals? These messages should be communicated clearly and concisely

Sustainability reporting is not a one-off project, but an ongoing process. Each reporting cycle offers the opportunity to further develop processes, data quality and content.

- Obtaining feedback: systematically evaluating feedback from internal and external stakeholders

- Optimize processes: Continuously improve data management, internal coordination processes and reporting workflows

- Train the team: Regular training ensures that the ESG team remains familiar with current standards and regulatory developments

- Adjust targets: Measure progress and refine ESG targets based on reporting results

Companies that see ESG reporting as a strategic tool and not just a mandatory task will benefit the most in the long term.

Challenges and advantages

Sustainability reporting involves effort, and there is no way to sugarcoat it. At the same time, it offers tangible strategic advantages to companies that take the process seriously. A realistic view of both sides.

Challenges

High costs and time expenditure

The introduction of ESG reporting is initially associated with considerable expense. In addition to the acquisition costs for suitable software, there are ongoing costs for data collection, analysis and reporting. Added to this is the time required: several departments must be coordinated, data must be checked and validated, and external auditors must be involved.

The initial effort can be a real burden, especially for smaller companies. This is where it pays to rely on digital ESG reporting tools at an early stage in order to automate processes. Are you interested in ESG reporting software? Then you should get to know our sustainability reporting tool.

Data availability and quality

Collecting reliable ESG data is one of the biggest practical hurdles - especially for companies with complex, international supply chains. The challenges are:

- Data is available in different systems and formats

- Suppliers and partners provide data of varying quality

- Scope 3 emissions are difficult to record methodically

- Missing or inconsistent data jeopardizes audit security

Regulatory uncertainty

The ESG landscape is in flux and companies are feeling this directly. Standards are changing, deadlines are being postponed, areas of application are being redrawn. The current simplification measures for CSRD are the most recent example. If you want to plan for the long term, there is no way around continuous monitoring of regulatory developments.

Standardization and comparability

The multitude of frameworks - ESRS, GRI, SASB, TCFD, ISSB, UNGPRF, CDSB - can seem overwhelming at first. Which standard suits your own company? How can reports from different companies be compared? These questions arise in particular for investors and analysts who use ESG data as a basis for decision-making.

Internal coordination

An ESG report is not produced by a single department. Rather, it is a joint project. Sustainability, finance, HR, compliance, purchasing and communication must all pull together. This sounds obvious, but in practice it is often the biggest hurdle. Clear responsibilities and functioning data management are just as important as the willingness to think across departments.

Stakeholder management

Investors want numbers. Customers want attitude. NGOs want impact. Regulators want compliance. Satisfying all of them at the same time is simply not realistic. What counts is honest and consistent communication, even if not everything has been achieved yet. This is exactly what builds trust in the long term.

Advantages

Transparency and increased stakeholder trust

A detailed ESG report creates trust among investors, customers, suppliers and the public. Those who report openly on progress, but also on gaps, are perceived as credible and responsible players. Transparency is not an end in itself, but a strategic asset.

Companies that report transparently on their ESG performance build stronger relationships with their stakeholders in the long term, which pays off.

Better access to capital and more favorable financing

Sustainable investments are no longer a niche topic. Institutional investors, banks and lenders are increasingly taking ESG criteria into account in their decisions. A well-founded ESG report can:

- Increase the attractiveness for ESG-oriented investors

- enable more favorable credit conditions

- Facilitate access to green bonds and sustainable financing instruments

Regulatory compliance and risk avoidance

Those who start early have less stress later. Robust ESG reporting protects against fines and reputational damage, but it does even more: those who deal with ESG issues in a structured manner recognize risks earlier and can take targeted countermeasures before they become a problem.

Increased efficiency and cost savings

The examination of energy consumption, waste management and the use of resources as part of ESG reporting often reveals potential savings that were not previously visible. At the same time, standardized data processes and clear responsibilities promote internal efficiency.

Competitive advantage and brand image

Sustainability is no longer a nice-to-have. Consumers and business partners are increasingly basing their decisions on it. Companies that live ESG practices credibly and communicate openly about them are perceived as pioneers. This strengthens the brand and trust.

Innovation and new business opportunities

Sustainability reporting not only looks back, it also drives forward. Anyone who takes a serious look at sustainability issues will almost inevitably come up with new ideas: more efficient processes, different business models, unexpected partnerships. Anchoring sustainability strategically also means opening new doors.

ESG reporting is not a bureaucratic compulsory program. It is an opportunity to position your own company for the future.

Conclusion

ESG reporting is no longer just a compliance issue. Companies that report transparently on their sustainability performance gain the trust of investors, manage risks better and gain a real competitive advantage. Yes, the effort involved is real: high data requirements, regulatory complexity, cross-departmental coordination. But with the right processes and tools, it can be managed.

The direction is clear: ESG reporting is becoming more important, not less. Requirements are increasing, investors are taking a closer look and ESG criteria are increasingly being incorporated into financial decisions. Companies that act now are not only better prepared, they are turning sustainability into a real growth driver.

Frequently asked questions

This depends heavily on the size of the company and the maturity of the existing data processes. Experience shows that companies should allow at least six to twelve months for the initial preparation of an ESG report.

The specific sanctions vary depending on the member state, as the CSRD is implemented nationally as an EU directive. In Germany, breaches of reporting obligations can result in fines and, in the case of capital market-oriented companies, reputational damage.

For companies subject to CSRD, yes: an external audit is mandatory. It starts with a limited assurance, i.e. a restricted audit. In the long term, this is to become a full reasonable assurance. The requirements will therefore gradually increase. Find out more about ESG ratings.

In everyday life, both terms are often used synonymously and that is not wrong. The difference lies more in the history: Sustainability reports were voluntary and not very standardized for a long time. Today, ESG reports are more regulated and include specific legal requirements.

Indeed, the CSRD even stipulates that the sustainability statement is part of the management report and does not have to be published as a separate document.

The costs vary considerably depending on the size of the company, complexity and tools used. In addition to internal personnel costs, there are often costs for ESG software, external consultants and the audit. For medium-sized companies, total costs in the five- to six-figure range are not unusual.

Yes, there are now a large number of specialized tools that support data collection, management and reporting. They help to automate processes, bundle data sources and map the requirements of the ESRS in a structured manner. Find out more about our software for creating sustainability reports.

Scope 1 comprises direct emissions from own sources, Scope 2 indirect emissions from purchased energy and Scope 3 all other indirect emissions along the value chain, for example from suppliers or the use of products by customers. Scope 3 is often the largest, but also the most difficult to record.

Double materiality means that a topic is evaluated from two perspectives: What impact does the company have on the environment and society and, conversely, what financial risks or opportunities arise for the company as a result of sustainability issues? Both perspectives must be taken into account in the materiality analysis.

Under certain conditions, yes: non-EU companies with a net turnover of over EUR 150 million in the EU and at least one subsidiary or branch in the EU may also be required to report. CSR (Corporate Social Responsibility) is to be distinguished from CSRD.

Matthias Klein

LinkedInESG compliance expert - lawcode GmbH

Matthias Klein advises companies on the implementation of supply chain laws such as the CSDDD and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.