Important facts

- What is the EU taxonomy?

- A classification system that defines which economic activities are considered environmentally sustainable. It is a central element of the EU sustainability strategy.

- What is the goal?

- Steer capital flows into sustainable investments, prevent greenwashing and create a uniform basis for ESG assessments and reporting.

- Who does the regulation apply to?

- For large companies covered by the CSRD, as well as financial market participants and governments in the design of sustainable financial products.

- What environmental goals does it cover?

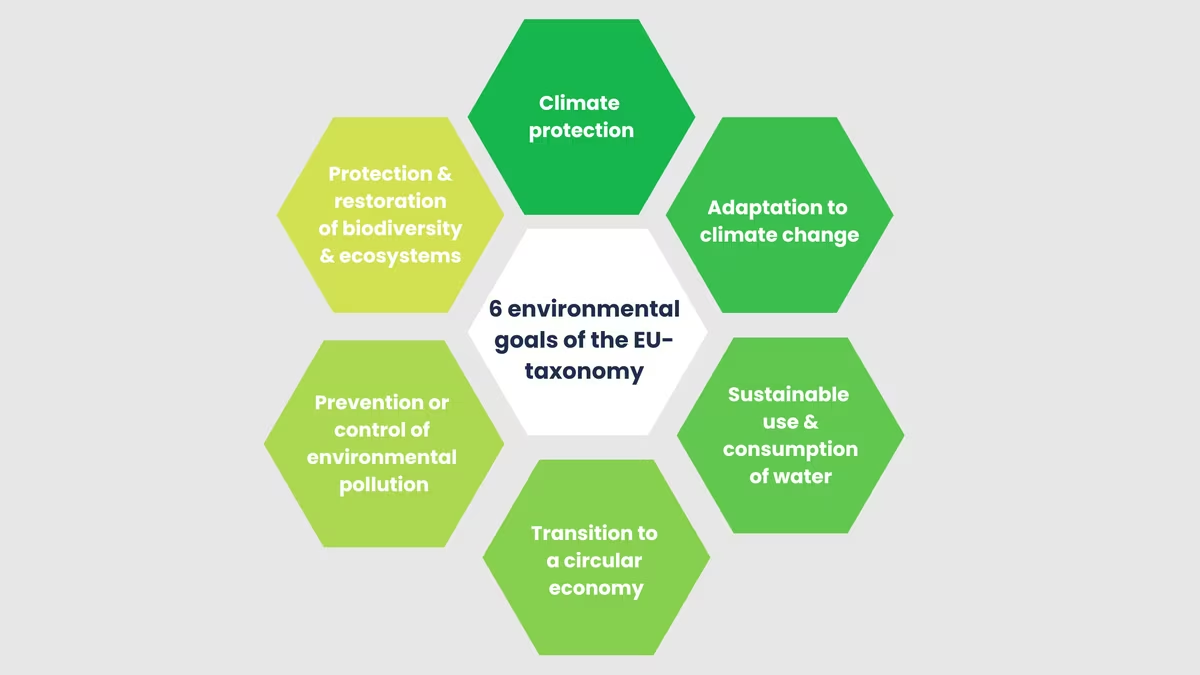

- It comprises six environmental goals, including climate protection, adaptation to climate change, circular economy, water and marine resource protection, pollution prevention and biodiversity protection.

- What are the challenges?

- The requirements are complex and data-intensive, especially for companies with diverse business areas or international supply chains.

- What advantages does the taxonomy offer?

- It improves the comparability of sustainability reports, supports investment decisions and is a key tool for credible ESG strategies.

Abstract

The EU taxonomy is an EU-wide standardized classification system for determining which economic activities are considered environmentally sustainable. It creates a verifiable definition of "green" within the European Union, increases comparability and is intended to limit greenwashing. The aim is to channel capital flows more strongly into activities that make a measurable contribution to the environmental goals of the European Green Deal.

It is based on six environmental objectives (including climate change mitigation, adaptation, circular economy, water, pollution prevention and biodiversity). An activity is only taxonomy-compliant if it makes a substantial contribution to at least one objective, does not significantly harm other objectives (DNSH), complies with minimum protection and meets the technical criteria.

For companies, this means above all that key figures on turnover, CapEx and OpEx must be disclosed. The group affected and the timetable are closely linked to the CSRD and are currently in flux due to EU simplifications. Since the beginning of 2026, new requirements have also made reporting easier (including leaner templates and a 10% materiality logic).

In short: the EU taxonomy makes sustainability measurable and thus becomes the common basis for reporting, financing and transformation.

Current update on the EU taxonomy (as of January 2026)

The current focus of the EU taxonomy is less on new obligations and more on noticeable simplification in application and reporting. The Delegated Regulation (EU) 2026/73 (published by the European Commission in the Official Journal of the EU on January 8, 2026) has streamlined the disclosure requirements in several places.

What is new or has been simplified?

- Less effort in reporting: templates and data points have been reduced. Reporting should become leaner overall.

- 10% materiality threshold: Certain activities no longer need to be audited in full depth if they are below a defined relevance threshold (per KPI, e.g. revenue/CapEx).

- Easing of the OpEx KPI: If operating expenses are not material to the business model, the OpEx taxonomy audit can be waived under certain conditions (with corresponding justification/transparency in the report).

- DNSH simplified in certain areas: Some requirements relating to "Do No Significant Harm" have been made more practical in order to reduce the amount of evidence required.

In addition, the EU Commission has published draft FAQs (17.12.2025) that explain the application of the changes and address typical implementation issues.

Important in practice:

These changes are particularly relevant for companies that have to report taxonomy KPIs as part of the CSRD (Corporate Sustainability Reporting Directive) anyway. This is because it is here that it will be decided where verification and data effort is really necessary and where companies can manage with less detail in future.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

What is the EU taxonomy?

The EU taxonomy is an EU-wide standardized classification system for ecologically sustainable economic activities. It defines when an activity is considered environmentally sustainable and thus makes the term sustainable verifiable and comparable.

Essentially, the taxonomy creates a common frame of reference for companies, investors and financial market players: instead of vague sustainability promises, there are clearly defined criteria that can be used to assess whether an activity actually makes a measurable contribution to environmental goals.

In short, the EU taxonomy is a common definition of green in terms of activities, not entire companies.

What distinguishes the EU taxonomy

- Focus on economic activities: It evaluates what a company does and not whether a company is good or bad overall.

- Uniform standard in the EU: It ensures comparability and reduces scope for interpretation.

- Criteria-based instead of promotional: Sustainability is classified according to defined requirements, not marketing terms.

What the EU taxonomy is not

- No seal of approval for companies or financial products

- No obligation to invest in green projects

- No ranking or sustainability score for entire companies

Why was the regulation adopted?

With the European Green Deal, the EU has set a clear course: Europe is to become climate-neutral by 2050 and emissions are to be significantly reduced by 2030. This is not just a political goal, but above all an investment task: the conversion of energy, industry, buildings, mobility and value chains requires enormous resources. And even if public programs provide a lot of impetus, it is clear that the transformation cannot be financed on a broad scale without private investment.

This has long been a key problem: what exactly is "sustainable"? Terms such as "green", "environmentally friendly" or "sustainable" were used very differently depending on the provider, industry or country. This has encouraged two things: Greenwashing (when something appears "green" but the effect cannot be proven) and market fragmentation (when everyone evaluates according to different standards). This has made it difficult for companies and investors to classify sustainability in a comparable and verifiable way and to direct capital flows towards genuinely sustainable activities.

The EU Taxonomy Regulation was therefore adopted to create a uniform frame of reference: it defines when an economic activity is considered environmentally sustainable, not as a question of image, but on the basis of clear criteria. Together with the SFDR (for financial market players) and the sustainability reporting framework (CSRD), it forms the foundation of the EU strategy for sustainable finance.

The common effect: sustainability should not only be formulated as a goal, but also become measurable, comparable and more transparent in the market.

As a result, the regulation pursues three central guiding principles: directing capital flows more strongly towards sustainable investments, systematically anchoring sustainability in risk management and promoting long-term investments and business practices. In this way, the EU not only creates orientation, but also legal certainty and fairer competitive conditions, as all parties involved can refer to the same benchmark.

When does the EU taxonomy apply?

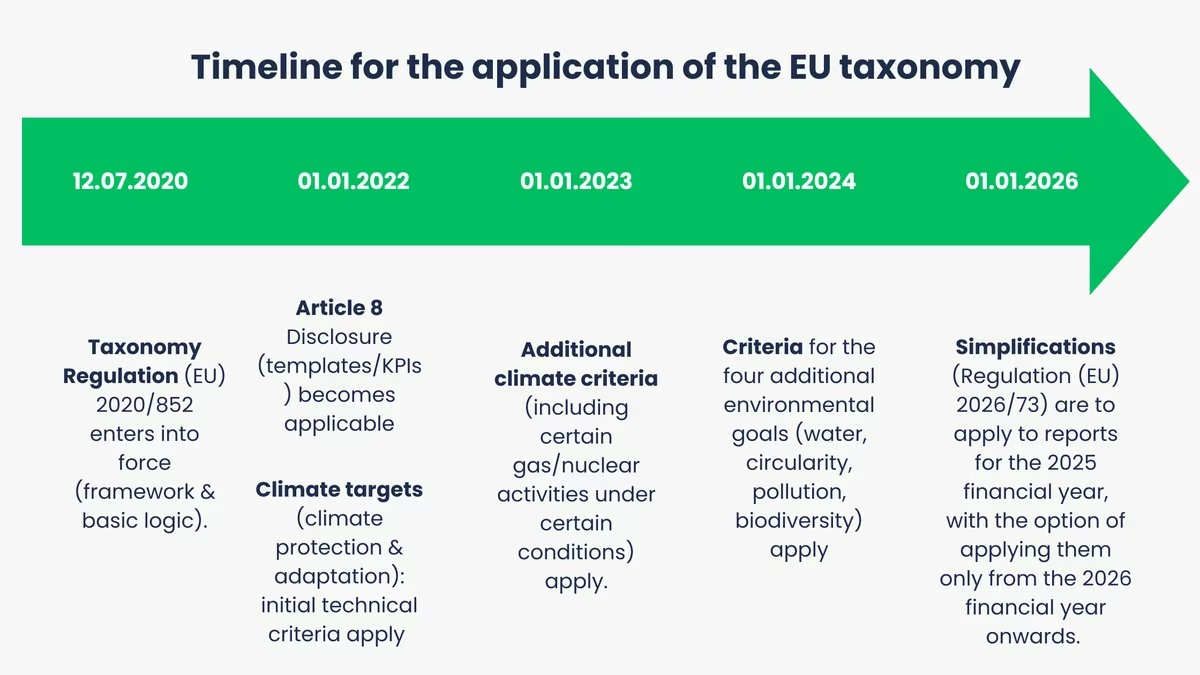

It is worth making a clear distinction in terms of timing: The taxonomy has been legally valid since 2020, but has been introduced in stages in practice (criteria + reporting) and has since been expanded and adapted via delegated acts.

When did the Taxonomy Regulation come into force?

- July 12, 2020: The EU Taxonomy Regulation (framework) comes into force.

- Since January 1, 2022: The Article 8 disclosures (taxonomy key figures/indicators) become practically relevant for reporting companies.

When do the criteria for the environmental objectives apply?

The taxonomy works with technical criteria ("Technical Screening Criteria"), which were successively implemented for each target area:

- From January 1, 2022: criteria for the first two environmental targets (climate protection and adaptation to climate change) apply

- From January 1, 2023: Supplementary criteria (including certain gas and nuclear activities as "Complementary Climate Delegated Act") apply.

- From January 1, 2024: criteria for the four other environmental goals (water/oceans, circular economy, pollution prevention, biodiversity/ecosystems) apply.

When does the report have to say something about this?

In practice, taxonomy disclosure in accordance with Article 8 depends on whether a company (or group) is subject to sustainability reporting. Groups that were already subject to the previous NFRD reporting must apply the CSRD requirements for the first time for the 2024 financial year (publication of the report in 2025).

For all other large companies and listed SMEs, the start was postponed by two years as part of the "stop-the-clock" regulation: Large companies will therefore generally only start from the 2027 financial year (2028 report), listed SMEs from the 2028 financial year (2029 report). Companies are considered "large" if they exceed at least two of three criteria on two consecutive reporting dates: more than 250 employees, more than €50 million in net sales and/or more than €25 million in total assets.

Article 8 logic was also introduced in stages, first taxonomy-compliant, later taxonomy-compliant:

- From January 2022 (reporting on FY 2021): Large companies initially report primarily on taxonomy capability and certain qualitative disclosures, for climate targets.

- From January 2023 (reporting on FY 2022): Large non-financial companies additionally report taxonomy compliance for climate targets.

- From 2024 (reporting on FY 2023): Large financial companies adopt the "eligible + aligned" logic (for climate targets).

- From 2024/2025 (for reporting years from 2024): The four new environmental targets are included in audits/disclosures because the criteria have applied since 01.01.2024.

What's new from 2026?

There have been noticeable simplifications in reporting since the beginning of 2026:

- Regulation (EU) 2026/73: Simplified templates, fewer data points, 10% materiality threshold, etc. applicable from January 1, 2026 and intended for reporting on the 2025 financial year (with option to apply only from the 2026 financial year).

Quick note: "Who exactly" is affected remains politically in motion

In practice, taxonomy disclosure is closely linked to the group of CSRD/accounting directive reporting entities. As part of the EU simplification(omnibus), application dates were postponed (stop-the-clock) and the future limitation of the group of users was discussed or provisionally agreed, which can also indirectly influence who has to report taxonomy KPIs.

The EU taxonomy is a key component in supporting the objectives of the Green Deal.

What are the objectives of the EU taxonomy?

Until the taxonomy, there was no consistent answer to the question of what "green", "sustainable" or "environmentally friendly" really means within the meaning of the EU. The aim of the regulation is therefore to establish a common reference framework that clearly describes when an economic activity is considered environmentally sustainable.

The taxonomy is intended to help channel investments more strongly into activities that make a substantial contribution to environmental goals and thus make the transformation financially viable. In short: money should flow more easily to where it has a demonstrable impact.

A key driver was the experience that "green" claims are often difficult to verify. The taxonomy counters this with clear criteria instead of advertising promises. The aim: if sustainable properties are claimed, they should be verifiable and thus strengthen trust among investors, customers and stakeholders.

Without a uniform framework, many parallel benchmarks (national, industry-related, product-related) are created. The taxonomy is intended to prevent precisely this, creating an EU-wide reference point so that sustainable activities can be compared across countries and sectors.

In addition to directing capital, it is also about the stability of decisions: Sustainability risks should not remain "optional", but should be systematically taken into account. The taxonomy supports this approach by providing a structured basis for incorporating ecological aspects into assessments and decisions.

The six environmental goals as a content framework

To make it clear what "ecologically sustainable" refers to, the taxonomy works along six environmental goals:

- Climate protection

- Adaptation to climate change

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Prevention and reduction of environmental pollution

- Protection and restoration of biodiversity and ecosystems

What is important here is that an activity should not just be "somehow good", but should support sustainability without conflicting objectives, i.e. it should not improve in one place and significantly harm in another.

Which companies are affected?

Whether a company is affected by the EU taxonomy depends less on the industry or its own sustainability claim than on whether taxonomy-related information must be disclosed. The taxonomy is therefore primarily a reporting and transparency framework: It ensures that companies and financial market players can use a uniform standard to show what proportion of their activities can be classified as environmentally sustainable.

In practice, two groups are currently particularly relevant:

Firstly, companies that were (previously) subject to non-financial reporting. Initially, these were primarily large, capital market-oriented companies that already had to publish non-financial information under the previous NFRD logic (in Germany via the CSR-RUG or Sections 289b, 315b HGB). For these companies, taxonomy disclosure has been an integral part of sustainability reporting for years - with clear key figures and presentation requirements.

Secondly, financial market players that offer financial products in the EU and have to disclose sustainability information as part of the SFDR - such as banks, insurance companies, asset managers and pension funds. For them, the EU taxonomy is particularly important because it serves as a reference to classify the sustainability characteristics of products and portfolios in a comprehensible manner.

It is important to note that the CSRD was originally intended to significantly expand the group of users and thus also the group of companies for which taxonomy disclosures are practically relevant. At the same time, this expansion has recently come under political and regulatory pressure. In the course of the EU simplifications (omnibus), deadlines have been postponed (stop-the-clock) and work is being done in parallel to refocus the future user group. For SMEs, this means that the question "Are we affected?" now depends more than ever on which reporting wave actually applies and how the final thresholds are structured in the simplified CSRD framework.

In short, the companies and financial market players most affected are those that have to report sustainability information and for whom the EU taxonomy provides the common logic to not only claim "environmentally sustainable", but to classify it uniformly.

What do companies need to do?

If your company is subject to the EU taxonomy disclosure, the core issue is to disclose the proportion of taxonomy-related activities in the company in a comprehensible and auditable manner. The EU taxonomy does not require a "green self-assessment", but rather a structured classification according to fixed specifications, including key figures, methodology and documentation.

In practice, a clear process has proven itself:

- First, your business model is translated into taxonomy-relevant activities (Which activities are basically covered?).

- This is followed by classification as taxonomy-capable and, where possible, taxonomy-compliant (i.e. the question of whether the criteria are actually met).

- The results are then converted into three key figures in accordance with Article 8: Share of Sales, CapEx and OpEx.

For this to work properly, two things are needed above all: data capability (financial/controlling logic, clean denominators/counters, clear delimitations) and governance (who provides what evidence, who checks, who consolidates). In practice, this is precisely where most friction losses occur, because taxonomy is not just a sustainability issue, but also has a deep impact on finance, investment planning and process documentation.

New and important (as of January 2026): Delegated Regulation (EU) 2026/73 has noticeably simplified reporting and datapoints. This primarily affects companies that have previously invested a great deal of effort in detailed checks. Among other things, there is now a 10% materiality threshold (certain activities can be reported separately as "non-material" instead of being audited in full) and simplifications to the OpEx KPI if OpEx is not material to the business model. In addition, templates/data points have been reduced.

For implementation, it helps to consciously plan for these simplifications: Which activities are below the materiality threshold anyway? Where can OpEx be methodically justified? Which evidence (e.g. DNSH/minimum protection) really needs to be provided - and for which parts can you reduce the effort without losing significance?

In addition, the Commission has published draft FAQs (17.12.2025), which address typical interpretation and implementation issues relating to the amended disclosure - helpful if internal discussions (e.g. on delimitation or presentation) are stuck.

When are activities considered "sustainable" within the meaning of the EU taxonomy?

According to the EU taxonomy, an economic activity is not considered sustainable if it sounds good, but if it can be classified as ecologically sustainable according to clear criteria.

It is important to note that the taxonomy evaluates activities, not the entire company. A company can therefore have both taxonomy-compliant and non-compliant activities.

For an activity to be considered taxonomy-compliant, four conditions must be met:

- Substantial contribution: The activity makes a substantial contribution to at least one of the six environmental objectives.

- No significant harm (DNSH): At the same time, it must not significantly harm any of the other environmental objectives.

- Minimum protection: The activity is carried out in compliance with minimum social standards (e.g. human rights due diligence).

- Technical evaluation criteria: The activity fulfills the specific technical screening criteria defined for each activity.

In practice, a simple distinction helps to understand the logic:

- taxonomy-capable means "the activity is generally covered by the taxonomy".

- taxonomy-compliant means "the activity actually fulfills the criteria".

It is precisely this second stage that is often the more time-consuming part, because evidence, delimitations and documentation play a central role.

EU taxonomy, CSRD and SFDR

CSRD, SFDR and the EU taxonomy are often mentioned in the same breath because together they create the European framework for making sustainability comparable in the market.

The three modules have different tasks:

- The CSRD regulates how companies report on sustainability: in a structured, verifiable manner and according to uniform standards.

- The EU taxonomy provides the content standard for the "environmentally sustainable" section: it defines which activities can be considered sustainable according to EU logic.

- The SFDR in turn obliges financial market participants to disclose sustainability information on products and portfolios and uses taxonomy data, among other things, as a reference framework.

You can think of it as a common language: Companies provide the transparency and data basis via CSRD. The taxonomy ensures that "environmentally sustainable" is not interpreted arbitrarily. And the SFDR brings this information into the financial product logic so that investors can recognize what proportion of a portfolio is actually based on activities that can be classified according to taxonomy criteria.

Mnemonic:

CSRD = reporting obligation of companies,

Taxonomy = definition/classification,

SFDR = disclosure in the financial market.

Conclusion

The EU taxonomy is not a sustainability label, but a standardized reference framework that makes environmental sustainability comparable and verifiable. The focus is not on the question "Are we sustainable?", but on which activities can be classified as environmentally sustainable according to clear criteria and how transparently this classification is reported.

The taxonomy has long been effective where it counts: in investments, financing discussions and in the expectations of stakeholders. Those who understand the logic and embed it internally not only reduce compliance risks, but can also better explain how their own business model contributes to transformation - including in conjunction with business and human rights requirements, such as the Supply Chain Due Diligence Act.

Companies should therefore not treat the EU taxonomy as a one-off project, but rather as a recurring standard process with clear responsibilities, robust data logic and documentation that also stands up to scrutiny and further development.

Frequently asked questions

The taxonomy is an EU classification system that defines which economic activities are considered sustainable. It aims to promote investment in environmentally friendly technologies and create transparency for companies and investors. The taxonomy defines six environmental goals, including climate protection and the transition to a circular economy. An activity is classified as sustainable if it makes a significant contribution to at least one of these goals, does not significantly harm any other goal and complies with minimum social standards. Since January 2022, large companies have been obliged to disclose the sustainability of their activities in accordance with the regulation.

It was introduced to create a standardized classification system for environmentally sustainable economic activities. This is intended to promote transparency, steer investment towards environmentally friendly projects and prevent greenwashing. It is a central instrument of the EU action plan for financing sustainable growth and supports the objectives of the European Green Deal, in particular climate neutrality by 2050.

The regulation currently mainly affects large, capital market-oriented companies with more than 500 employees and financial market participants that offer financial products in the EU. However, the introduction of the Corporate Sustainability Reporting Directive (CSRD) will significantly expand the group of companies subject to reporting requirements. From the 2025 financial year, all large companies that meet at least two of the following criteria will be required to report: more than 250 employees, a balance sheet total of more than 20 million euros or net revenue of more than 40 million euros. From the 2026 financial year, capital market-oriented small and medium-sized enterprises (SMEs) will also be included in the reporting obligation. This gradual expansion means that a large number of companies of different sizes and from different sectors will have to meet the requirements in future.

The main objective of the taxonomy is to channel capital flows into sustainable investments in order to achieve climate neutrality in the EU by 2050. To this end, it defines six environmental goals: Climate change mitigation, climate change adaptation, sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and reduction, and protection and restoration of biodiversity and ecosystems. By providing clear criteria for sustainable activities, the taxonomy aims to create transparency, prevent greenwashing and enable investors to make informed decisions.

It stipulates that an economic activity is considered environmentally sustainable if it fulfills four key criteria:

- Significant contribution: The activity must contribute significantly to one or more of the six defined environmental objectives, such as climate protection or transition to a circular economy.

- No significant harm: It must not have a significant negative impact on any of the other environmental objectives, in accordance with the "Do No Significant Harm" (DNSH) principle.

- Compliance with technical assessment criteria: Specific technical criteria must be met, which are defined for each economic activity and determine the conditions under which an activity is classified as sustainable.

- Minimum social standards: Minimum protective measures must be observed in social and governance aspects, such as respect for human rights and fair working conditions.

The fulfillment of these criteria is intended to ensure that activities classified as sustainable actually make a positive contribution to environmental goals without compromising other goals, while at the same time respecting social standards.

In their non-financial reporting, companies must disclose the proportion of their revenue, capital expenditure (CapEx) and operating expenditure (OpEx) that is associated with taxonomy-compliant economic activities. To do this, they first identify taxonomy-compliant activities and then check their conformity with the taxonomy's technical assessment criteria.

The regulation is primarily aimed at large, capital market-oriented companies that are already obliged to provide non-financial reporting. However, with the introduction of the CSRD, the group of companies required to report will be expanded. From the 2025 financial year, all large companies that meet certain criteria will be required to report, and from 2026, capital market-oriented small and medium-sized enterprises (SMEs) will also be included.

Although not all SMEs are required to report directly, they may be affected indirectly. For example, banks and investors may require information from them in order to assess the sustainability of their own portfolios. It therefore makes sense for SMEs to familiarize themselves with the requirements and align their business models accordingly in order to meet future requirements and ensure their competitiveness.

The taxonomy obliges financial institutions to disclose the sustainability of their financial products by indicating the extent to which their investments and financing meet the taxonomy criteria. A key instrument here is the Green Asset Ratio (GAR), which measures the proportion of taxonomy-compliant assets in a financial institution's portfolio. This disclosure is intended to channel capital flows into sustainable projects and requires financial institutions to adapt their investment strategies and internal processes in order to meet the new requirements. The taxonomy also increases transparency for investors, enables well-founded decisions and promotes the development of sustainable financial products.

These include the generation of renewable energies such as wind and solar energy, measures to increase energy efficiency, for example through building renovations, as well as activities in the area of the circular economy that support recycling and resource conservation. Sustainable forestry and environmentally friendly transportation, such as low-emission vehicles, are also classified as sustainable. This classification is intended to create transparency and help achieve the EU's climate targets.

To implement the taxonomy in your company, you should first check whether your company is obliged to report. Then identify relevant business activities, assess their compliance with the criteria and ensure compliance with minimum social standards. Collect the necessary data and integrate it into your reporting to ensure transparency about the sustainability of your activities.

The application poses challenges for companies. These include legal ambiguities and contradictory criteria that make implementation difficult. In addition, there is often a lack of complete data for the required reporting, which increases the workload. Integrating the requirements into existing company processes requires considerable adjustments and can be resource-intensive. These factors highlight the need for clear guidelines and supporting measures to ensure the successful implementation of the EU taxonomy in companies.

The taxonomy is a classification system that sets out clear criteria for defining economic activities as environmentally sustainable. It differs from other sustainability standards and ratings in that it is legally binding and focuses on scientifically based, uniform benchmarks. In contrast to voluntary standards such as the Global Reporting Initiative (GRI) or the Carbon Disclosure Project (CDP), which provide companies with guidelines for sustainability reporting, the taxonomy prescribes specific requirements that companies must meet. It also aims to provide investors with a reliable basis for sustainable investment decisions and to prevent greenwashing. The combination with guidelines such as the CSRD and the Sustainable Finance Disclosure Regulation (SFDR) creates a comprehensive framework that promotes transparency and comparability in sustainability reporting within the EU.

Environmental organizations such as Greenpeace and BUND have filed lawsuits with the European Court of Justice to stop the classification of gas and nuclear power as sustainable, as they fear that this decision contradicts the EU's climate targets. In addition, financial supervisory authorities and banks criticize the complexity and lack of practical relevance of the taxonomy, which could overburden companies and mainly favor consulting firms. Studies also show that the existing reports according to the EU taxonomy are often not very meaningful, which makes it difficult to assess the actual sustainability of companies.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.