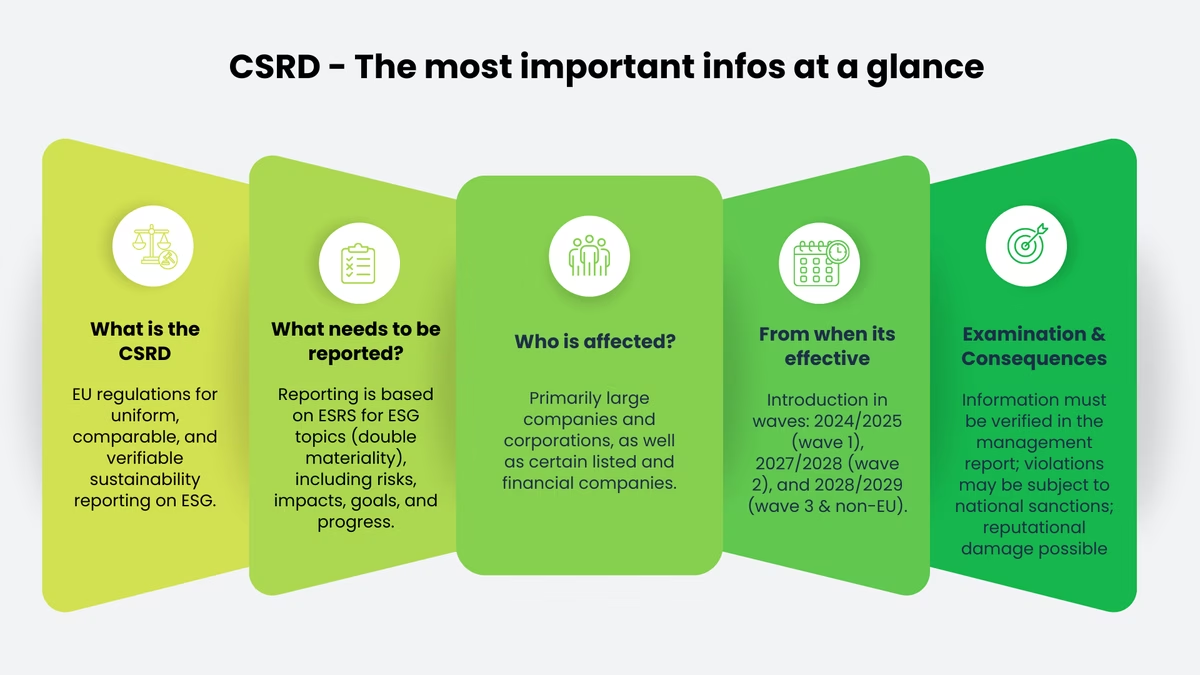

Important facts

- What is the CSRD?

- The CSRD (Corporate Sustainability Reporting Directive) is the new EU directive on sustainability reporting. It replaces the previous Non-Financial Reporting Directive (NFRD) and significantly tightens the reporting obligations.

- Who is affected?

- Companies that were already subject to the NFRD will report first, followed by other large companies (2 out of 3: ≥250 employees, ≥€50 million turnover, ≥€25 million balance sheet) from FY 2027 and listed SMEs from FY 2028.

- What needs to be reported?

- Companies must report comprehensively on environmental, social and governance (ESG) issues, structured in accordance with the European Sustainability Reporting Standards (ESRS) and on the basis of dual materiality.

- How do you go about reporting?

- Reporting is carried out in accordance with the ESRS. First, a double materiality analysis is carried out, after which relevant ESG issues are identified, evaluated and disclosed.

- What requirements must the report fulfill?

- It must contain environmental, social and governance information in accordance with the binding ESRS requirements.

- What are the challenges?

- Companies must systematically collect ESG data, adapt processes and fulfill reporting obligations in a short period of time, which is particularly challenging for first-time reporters.

Summary: The CSRD at a glance

The Corporate Sustainability Reporting Directive (CSRD) is the central EU framework for comparable and auditable sustainability reporting. In future, certain companies will have to report on environmental, social and governance (ESG) issues in a standardized manner, in accordance with the binding ESRS, integrated into the management report and generally audited externally. The aim is to make sustainability disclosures more robust, easier to compare and more reliable for investors, banks, customers and business partners.

Content is reported along the ESG dimensions, but only on those topics that are classified as relevant in the context of double materiality. Companies must not only present their impact on the environment and society, but also disclose financial risks and opportunities, specific targets, measures and measurable progress.

Prior to possible changes due to the EU Omnibus Initiative, large companies in particular are required to report if they meet at least two of the three thresholds (≥ 250 employees, ≥ € 50 million turnover, ≥ € 25 million balance sheet total). Depending on the classification, listed companies, small credit institutions or captive insurance companies may also be affected, while micro-enterprises are exempt.

The introduction will be staggered: Companies that were already subject to the NFRD will report for the first time for the 2024 financial year (publication in 2025). Other large companies will follow from the 2027 financial year (2028 report), listed SMEs and certain third-country companies from the 2028 financial year (2029 report).

Violations may result in national sanctions such as fines or orders to make improvements. In addition, reputational damage and indirect economic disadvantages can arise, as sustainability data is increasingly being factored into financing and supply chain decisions.

Update (status: February 2026)

The CSRD remains the central framework for comparable and auditable sustainability reporting in Europe, but has recently been adjusted in terms of timing and scope. As a result of the "stop-the-clock" amendment, the start dates for companies in the second and third waves have been postponed by two years. At the same time, the omnibus package is intended to significantly reduce the number of companies subject to reporting requirements (including higher thresholds; listed SMEs are to be removed from the scope). The final design is still in the legislative process.

In terms of content, the ESRS remain the binding basis, supplemented by a "quick fix" to relieve the first rapporteurs. Sector-specific ESRS and standards for third-country companies have been postponed to 2026. For non-reporting companies, the voluntary VSME standard is gaining in importance as a structured way of responding to data requests from value chains. Digital publication is also continuing to develop: ESMA is working on integrating sustainability disclosures into the ESEF regime (tagging/XBRL).

What is the Corporate Sustainability Reporting Directive (CSRD)?

Definition and key features of the CSRD

The Corporate Sustainability Reporting Directive (CSRD) is the central EU framework for comparable and verifiable sustainability reporting. It specifies which companies must systematically report on environmental, social and governance(ESG) issues in future. The focus is no longer on individual formats, but on uniform requirements.

The aim is to make sustainability reports more reliable. Investors, banks, customers and business partners should be able to classify the information more quickly and compare companies more easily.

At its core, the CSRD anchors sustainability where it is most relevant for external addressees: in the management report. Sustainability disclosures are therefore no longer a separate communication report, but part of regular corporate reporting. They also have higher requirements in terms of structure, traceability and internal approval processes.

A key feature of the CSRD Directive is the binding reporting framework provided by the European Sustainability Reporting Standards(ESRS). The ESRS define what must be reported and how the information is to be structured. This applies not only to topics and key figures, but also to methods, explanations and the way in which information should be documented. The aim is to achieve a reporting level that is more consistent than before and can be audited externally.

In terms of content, the CSRD Directive follows the principle of dual materiality. On the one hand, companies must describe which sustainability issues can influence their financial situation (risks and opportunities). On the other hand, they must explain what material impacts the company itself has on the environment and society. This creates a more complete picture of relevance - both from the company's perspective and from the perspective of external impact. This is also referred to as "double materiality". Read more about this in our article on double materiality.

Added to this is the obligation to verify: sustainability disclosures must always be verified externally, initially usually with limited assurance. This significantly increases the requirements for data quality and documentation. Companies must be able to prove where their figures come from, how they were calculated and who is responsible for them internally.

Finally, digital publication is also evolving. The direction is clear: in the future, sustainability disclosures should be more digitally readable and therefore easier to compare, for example via tagging approaches in the context of the ESEF Regulation. Overall, the CSRD is also part of the European sustainable finance approach and therefore also the SFDR (Sustainable Finance Disclosure Regulation). This means that the data is not only "communicated", but also provided in such a structured way that it can actually be used for capital market requirements and value chains.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

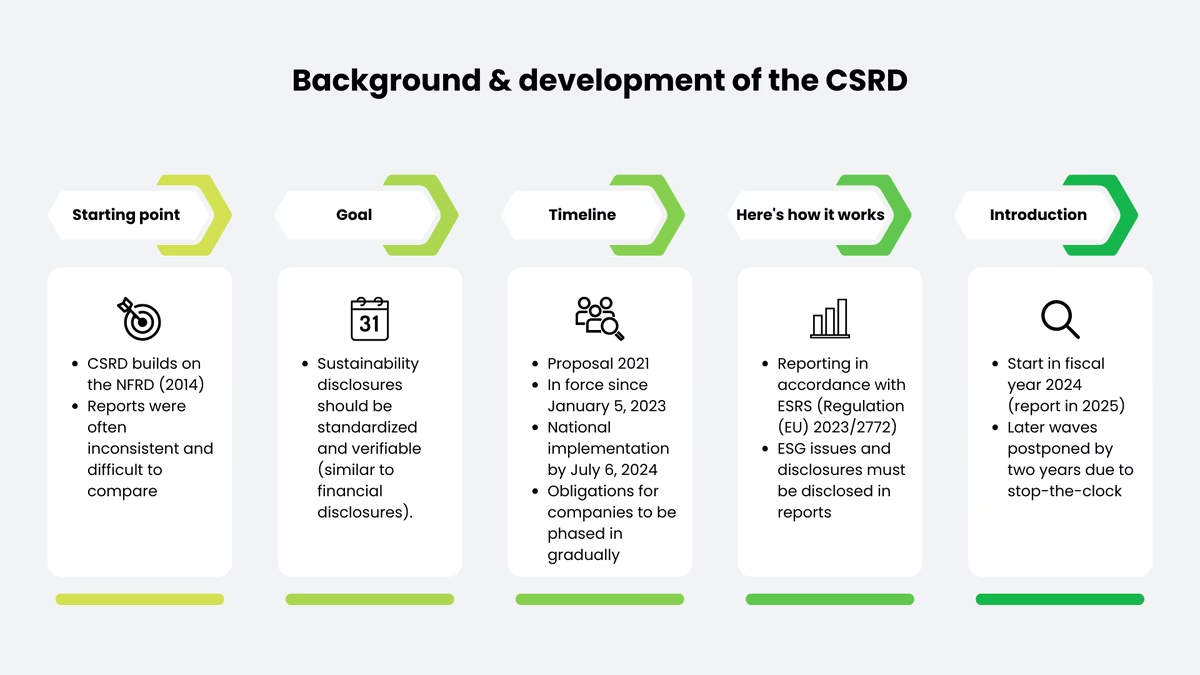

Background and development of the CSRD

The CSRD builds on the previous Non-Financial Reporting Directive(NFRD) from 2014 and its national implementation. In Germany, this was implemented via the CSR-RUG or CSRD Implementation Act, among other things. In practice, however, it quickly became apparent that the scope, comparability and verifiability of non-financial disclosures were often inadequate. Reports were structured very differently, key figures and methods were not standardized and a reliable comparison between companies was only possible to a limited extent.

This is precisely where the CSRD comes in. It aims to bring sustainability information to a similar level as financial information in the future. This means that it should be standardized, comprehensible and generally verifiable.

The reform was primarily triggered by the European Green Deal and the EU's Sustainable Finance Strategy. The European Commission presented its proposal in April 2021. Following negotiations, the Corporate Sustainability Reporting Directive was published as Directive (EU) 2022/2464 in the Official Journal of the EU and has been in force since January 5, 2023. The member states had to transpose the requirements into national law by July 6, 2024 at the latest. Here you can find the FAQ of the EU Commission.

The content of the CSRD is specified by the European Sustainability Reporting Standards (ESRS). They have been adopted as Delegated Regulation (EU) 2023/2772 and lay down binding rules on what companies must report and how the disclosures must be structured. For companies that are the first to report, there are also targeted simplifications ("quick fixes") to make it easier to get started with individual disclosures.

The timetable is staggered: Companies that were already covered by the NFRD will apply the CSRD for the first time for the 2024 financial year. Publication of the report was planned for 2025. For other groups of companies, the original timetable was recently adjusted politically. The start dates for later waves have been pushed back by two years due to so-called "stop-the-clock" changes. For many companies, this means more preparation time and greater clarity that the requirements are coming and need to be implemented in a structured manner.

Why the CSRD was introduced

The CSRD Implementation Act was introduced because the need for reliable and comparable sustainability information has risen sharply, but many previous reports were not sufficient. Investors, banks, customers and business partners want to better understand how companies deal with climate and environmental risks, what social risks exist, how supply chains are set up and how governance structures function. However, if reports are structured very differently, terms are used inconsistently or key information is missing, information gaps arise - and decisions become more difficult.

This is precisely where the CSRD comes in: it makes sustainability disclosures more binding, more standardized and generally verifiable, thereby also reducing the risks of intransparency and greenwashing. For companies, this means more demands and more effort because data, responsibilities and internal controls have to be clearly established. At the same time, the CSRD creates structure and orientation: those who start early establish robust ESG reporting and can meet requirements from financing and value chains more consistently.

The CSRD Directive pursues clear political and economic objectives.

Objectives and significance for companies

The CSRD is intended to improve sustainability information so that it can actually be used in the market by investors, banks, customers and other stakeholders. The main focus here is on transparency.

- Comparability instead of individual formats: Companies report according to a standardized framework so that stakeholders can better classify and compare information.

- Sustainability is becoming relevant to management: Those who report transparently must create clear internal targets, responsibilities and data processes. This increases commitment.

- Better basis for decision-making: Stakeholders can better assess risks, opportunities and progress, e.g. in financing, purchasing or partnerships.

- Less room for interpretation: Standardized requirements reduce "storytelling" without substance and increase consistency over the years.

Another aim is for companies to show more clearly and regularly what impact they have on the environment and society and how they deal with it. The aim is not just to make individual statements, but to systematically record, explain and manage them.

- Making environmental impacts visible: Topics such as climate, resources, emissions and biodiversity are considered in a more structured way and disclosed in a comprehensible manner.

- Addressing social risks seriously: Working conditions, human rights, supply chain risks or impacts on communities are coming more into focus.

- From report to improvement: If data is collected properly, goals can be defined more concretely, measures prioritized and progress measured.

- Increased external responsibility: Transparency means that companies are judged more by their statements, including their reputation.

The CSRD Directive also has a clear internal market logic: it is intended to create uniform minimum requirements throughout Europe so that corporate responsibility does not depend on national interpretations or voluntary standards.

- Uniform standards in the EU internal market: less fragmentation, more consistency across countries and sectors.

- Fairer competitive conditions: If basic requirements apply to many, sustainability becomes less "optional" and less of a pure communication differentiator.

- Stronger impact along the value chain: standardized data logics facilitate information flows between companies, customers and suppliers.

- Sustainability as part of good corporate governance: ESG is more closely interlinked with governance, risk and control systems and thus structurally anchored.

Affected companies & implementation

The CSRD is generally intended for large companies and certain capital market-oriented companies and will be introduced in stages. Important (as of February 2026): In addition to the classic CSRD scope, there are already effective shifts due to stop-the-clock, and in parallel, a political line is on the table with the omnibus package, which is intended to significantly reduce the scope (including higher thresholds; listed SMEs are to be excluded).

Note: Amendments through the omnibus package are in the legislative process and have not yet been finalized. Find out more about the EU Omnibus Directive here.

Criteria for determining the reporting obligation

Whether a company is subject to CSRD reporting essentially depends on three questions:

1) Does the company fall into one of the CSRD categories?

Typically these are:

- Large companies (according to the size criteria of the EU accounting system) and parent companies of large groups that meet at least two of three size criteria:

- Balance sheet total: ≥ € 25 million

- Net sales: ≥ € 50 million

- Employees: ≥ 250

- Other groups subject to reporting requirements (depending on the classification in the respective national transposition law):

- Listed companies

- small credit institutions

- Company insurance

- Micro-enterprises (CSRD definition), i.e. companies that do not exceed the following values, are exempt:

- Balance sheet total: ≤ € 450,000

- Net sales: ≤ € 900,000

- Employees: ≤ 10

Important for classification in group structures: Thresholds apply at consolidated level if a group exists.

This typically affects the following in particular:

→ Large companies and parent companies of large groups,

→ listed SMEs (in principle, with special rules, provided they remain in the final scope),

→ and in certain cases non-EU companies with significant EU activities for which reporting is triggered via an EU subsidiary or EU branch.

2) When does the obligation apply (waves/timing)?

The EU has deliberately staggered the introduction. The introduction began with companies that have already reported according to the previous logic (NFRD/CSR-RUG): for the first time for the financial year from January 2024, publication then typically in 2025.

For later waves, application has now been postponed by two years ("stop-the-clock"). This affects companies that were originally required to report for the first time for financial years 2025 and 2026.

3) What role does the Group (corporate group) and EU anchoring play?

The CSRD can apply both to individual companies and at group level. In addition, the obligation can be triggered for certain non-EU groups via the EU structure (EU subsidiary/EU branch, EU turnover threshold).

Classification according to the current legal status vs. omnibus (as of February 2026):

Parallel to the introduction of the EU omnibus package, a political discussion is underway that could reduce the number of companies subject to reporting requirements in the future. There is talk of concentrating the CSRD more on very large companies, for example those with more than 1,000 employees and a turnover threshold of over € 450 million.

Important: These changes are not yet final. They are still in the legislative process.

Differences between large companies and SMEs

Large companies are at the center of the CSRD system. They must report comprehensively in accordance with ESRS and have their disclosures audited externally. The requirements for data quality, processes and internal controls are correspondingly high. In practice, large companies are therefore usually the most affected and have to further develop their reporting structures and data management the most.

SMEs, on the other hand, should be viewed in two ways:

- In the original CSRD design, listed SMEs were always in scope (with the option of opting out). Due to "stop-the-clock", the starting point for this wave has shifted backwards.

- Non-listed SMEs are typically not directly subject to CSRD, but often feel the impact indirectly: via data requests from customers, banks or group structures.

Even if an SME is not directly required to report, it often still feels the effects of CSRD in practice. For example, through data requests from customers, banks or larger corporations in the supply chain. The voluntary SME standard(VSME) can help in such cases: It offers a clear framework for providing typical sustainability data in a structured and efficient manner.

Effects on subsidiaries and international companies

In groups, it is particularly important whether the sustainability report is prepared at group level. If so, individual subsidiaries may not have to report separately under certain circumstances because they are covered in the Group report.

The CSRD can also cover non-EU companies if they are economically relevant in the EU. In the original system, this applies in particular to cases with high EU turnover (classic: > € 150 million in the EU in two consecutive years) and an EU subsidiary (large or listed SME) or an EU branch with a relevant turnover threshold. Entry for this category is planned as a later wave (classic: from financial year 2028, report in 2029).

In the omnibus context, there are also discussions about raising thresholds and thus significantly reducing the number of companies affected (EU and non-EU). Politically, the line > 1,000 employees plus additional turnover threshold (> € 450 million) has been communicated, among other things.

Deadlines for implementation: Deadlines for large companies and SMEs

The application is carried out in several waves:

First wave: companies already subject to NFRD, generally large capital market-oriented companies

- First-time application for the 2024 financial year

- Publication of the first report in 2025

These companies already had to report in accordance with the previous NFRD regulation and are the first group to switch to ESRS.

Second wave: other large companies

- Originally planned: Financial year 2025

- Postponed to financial year 2027 due to the "stop-the-clock directive"

- Publication of the report in 2028

This affects large companies that were not previously subject to the NFRD.

Third wave: listed SMEs (if remaining in scope)

- Originally planned: Financial year 2026

- Postponed to financial year 2028

- Publication of the report in 2029

Special transitional rules apply to listed SMEs. Non-EU companies with significant EU activities:

- First-time application for the 2028 financial year

- Publication in 2029

The reporting obligation applies here if certain turnover and structural criteria are met in the EU.

Transition periods and exceptions

In addition to the staggered introduction, the CSRD provides for several transitional arrangements.

Stop-the-clock adjustment: For companies in the second and third wave, the original start of application has been postponed by two years. This is intended to give companies more time to prepare.

Opt-out rule for listed SMEs: Listed SMEs can make use of the reporting obligation for a limited transitional period, but must explicitly declare this.

Group regulations: In some cases, subsidiaries do not have to prepare their own CSRD report. This applies if they are included in the Group report and the requirements for this are met.

Political developments (omnibus package): While the CSRD is already starting, negotiations are continuing in the EU on who exactly should be subject to reporting requirements in future. The threshold values could still change. Companies should therefore continue to monitor these developments.

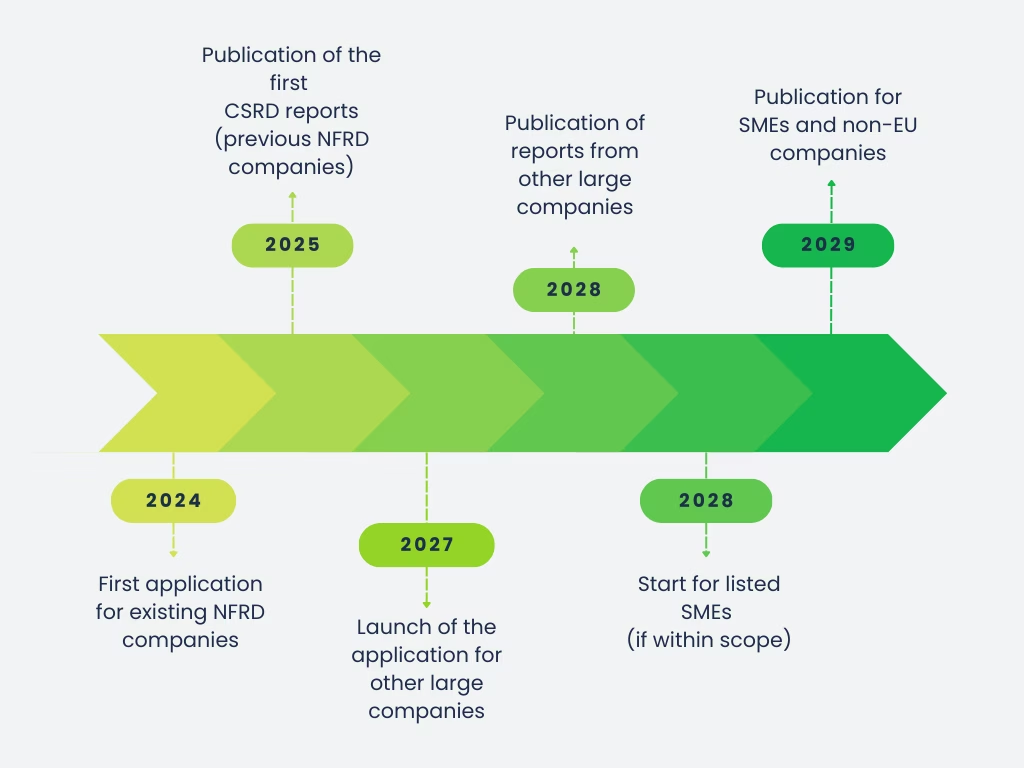

Timetable for the introduction of reporting obligations

The following chronological overview can be summarized:

- 2024: First application for existing NFRD companies

- 2025: Publication of the first CSRD reports

- 2027: Launch of the application for other large companies

- 2028: Publication of these reports

- 2028: Start for listed SMEs (if in scope)

- 2029: Publication for SMEs and non-EU companies

The staggering shows: CSRD will not happen overnight, but will be introduced step by step. Nevertheless, companies that do not have to report until later should also start early. This is because establishing ESRS-compliant data structures, internal controls and clear governance often takes several reporting cycles in practice.

What needs to be reported?

Sustainability risks and their management

Material sustainability risks and opportunities are a central component of reporting. Companies must disclose:

- which ESG issues are material to their business model,

- what impact their actions have on the environment and society,

- what financial risks and opportunities arise from sustainability issues,

- how these risks are identified, assessed and managed.

The principle of dual materiality applies here: both the external impact of the company and the effects of sustainability issues on the company's economic situation are considered.

In addition to current risks, the CSRD also requires a look ahead. Companies must set out the sustainability goals they are pursuing, how they intend to achieve them and how they will measure progress.

Environmental, social and governance aspects

In terms of content, the reporting is structured along the three ESG dimensions. The ESRS specify which topics are typically to be covered.

Environment (E):

- Climate change and greenhouse gas emissions

- Energy and resource utilization

- Circular economy

- Biodiversity and environmental pollution

Social (S):

- Working conditions and employee rights

- Diversity and equal opportunities

- Occupational health and safety

- Human rights in the supply chain

- Impact on affected communities

Governance (G):

- Corporate governance and supervision

- Compliance and anti-corruption measures

- Remuneration systems in connection with sustainability targets

- Integration of ESG issues into strategy and decision-making processes

Not every company has to cover every topic in equal depth. The decisive factor is the materiality analysis, which determines which aspects are reportable.

Financial and non-financial reporting

An important feature of the CSRD is that sustainability and financial reporting belong together. Sustainability disclosures do not stand alone, but are considered in conjunction with the economic situation of the company.

These include:

→ the linking of ESG risks with financial impacts,

→ the presentation of quantitative key figures and performance indicators,

→ the disclosure of targets and progress,

→ transparent explanations of methods, assumptions and data sources.

The sustainability disclosures are part of the management report and must be audited externally, initially usually with limited assurance. In the future, they should also be published in a digitally readable format. This makes it clear what needs to be reported. In practice, however, the main question is how companies can implement these requirements in a clean and structured manner. Pure financial reporting is no longer sufficient.

The CSRD clearly defines the content of what companies must report.

How companies set up CSRD reporting in practice

The first step is to define clear goals and indicators. Sustainability goals should be precise, measurable and defined in terms of time (SMART). Only in this way can progress be tracked and reported transparently.

Typical elements are

- quantitative targets (e.g. emissions reduction by a certain year),

- Key performance indicators for measuring environmental and social impacts,

- regular progress reports against the defined targets.

One frequently used indicator is the carbon footprint, for example. However, it is crucial that key figures match the business model and are collected consistently.

CSRD-compliant reporting requires comprehensible data processes. Companies must be able to demonstrate this:

- how data is collected,

- which systems and methods are used,

- how data is validated and released internally.

Regular monitoring is key here. Only those who continuously check whether targets are being achieved can make timely adjustments. Sustainability reporting thus becomes part of the internal control and risk management system.

The CSRD emphasizes the importance of transparency and dialogue. Companies should systematically record what stakeholders expect of them and which topics are perceived as particularly relevant.

This may include:

- Discussions with employees,

- Exchange with investors and business partners,

- Integration of suppliers,

- Consideration of social expectations.

These perspectives are incorporated into the materiality analysis and increase the credibility of the reporting.

Sustainability reporting does not always stay the same. Companies should therefore regularly check whether processes, key figures and targets are still appropriate. This is because new requirements, changes in the market or technological developments can make adjustments necessary.

Continuous improvement means:

- Regular evaluation of data quality,

- Further development of internal processes,

- Adaptation of strategies to new risks and opportunities.

Robust ESG reporting is the basis for CSRD reporting that is consistent, verifiable and efficient. This requires clear responsibilities and structured data flows. Read our article on ESG reporting to find out how to set up ESG reporting step by step, which key figures and data sources are typically required and what works in practice.

Standards and guidelines for CSRD reporting

European Sustainability Reporting Standards (ESRS)

The ESRS are the binding basis for CSRD reporting. They were developed by the European Financial Reporting Advisory Group (EFRAG) and adopted by the EU as Delegated Regulation (EU) 2023/2772.

The ESRS specifically define

→ which topics are to be covered,

→ which qualitative and quantitative disclosures are expected,

→ how information must be structured and explained,

→what role dual materiality plays.

The standards consist of general requirements and topic-specific requirements on the environment, social issues and governance. Companies start with a materiality analysis that determines which disclosure requirements are relevant and must be reported accordingly.

A key feature of the ESRS is its depth of detail. They require not only key figures, but also descriptions of strategies, objectives, measures and governance structures. This means that sustainability reporting is more formalized and integrated into corporate management. You can find out more about the ESRS here.

Reference to international standards such as GRI and TCFD

The ESRS were not developed in a "vacuum". International frameworks were taken into account during the development process so that companies have to duplicate work as little as possible.

The most important frames of reference include

- GRI (Global Reporting Initiative): Widely used standard for sustainability reporting with a focus on environmental and social impacts.

- TCFD (Task Force on Climate-related Financial Disclosures): Recommendations for the disclosure of climate-related risks and opportunities, particularly with regard to financial impacts.

The ESRS adopt important elements from these standards, particularly in climate reporting and the presentation of risks. Companies that have already reported in accordance with GRI or the TCFD recommendations therefore often have a good basis for getting started.

However, the CSRD does not simply replace national or voluntary frameworks. Rather, it creates a separate, binding EU standard. Companies can continue to use existing structures, but must adapt them to the specific ESRS requirements. The EU taxonomy also plays a significant role in sustainability reporting. Find out more about the EU taxonomy here.

Integration of CSRD into existing reporting structures

For many companies, the question arises as to how the CSRD can be practically integrated into existing reporting processes. The directive requires that sustainability information becomes part of the management report. This makes it clear that sustainability must not be managed as a separate report outside of financial communication.

In practice, this means:

→ Interlinking sustainability and financial reporting,

→ Integrating ESG issues into existing risk and control systems,

→ Coordination between sustainability, finance, compliance and legal departments,

→ Establishing clear responsibilities and internal approval processes.

Companies that have already produced sustainability reports can build on existing structures. However, the CSRD often requires a more systematic approach, particularly in terms of data quality, documentation and preparation for the external audit.

Integration into existing processes is therefore not just a formal compulsory exercise. In many companies, this means real change: responsibilities are redistributed, processes are adapted and interfaces between sustainability, finance and compliance are more closely interlinked. Sustainability reporting is thus increasingly becoming part of good corporate governance and no longer just a communication issue.

Step-by-step to the sustainability report

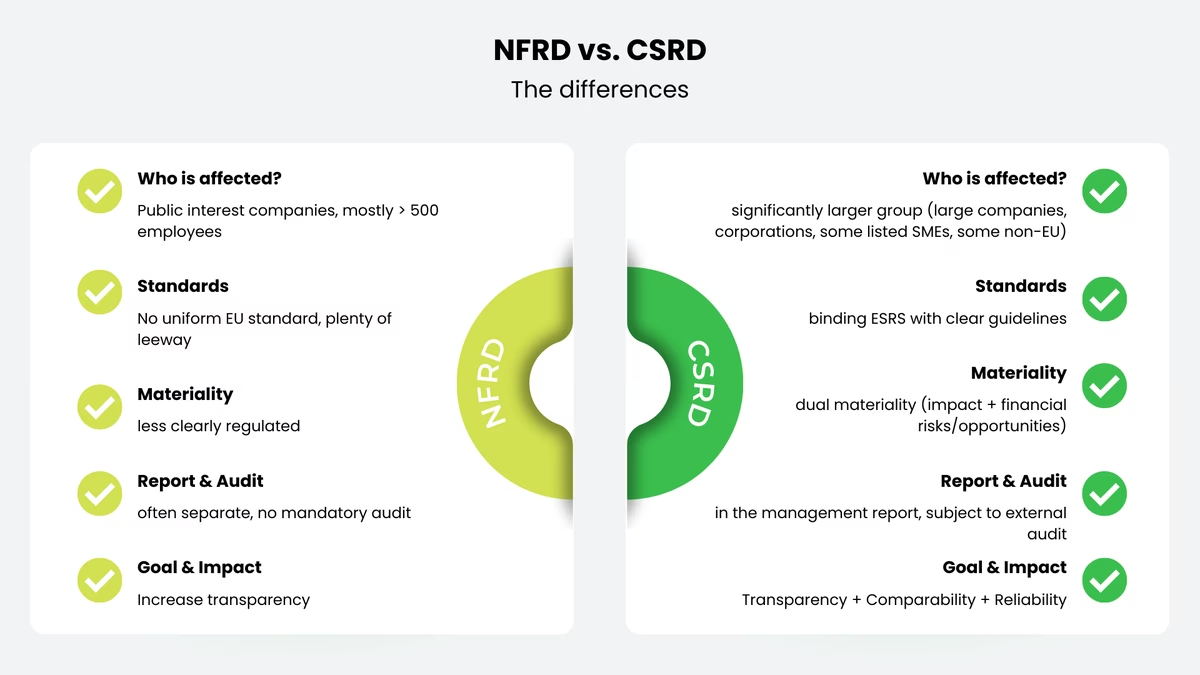

Differences between CSRD and NFRD

Extended scope of application of the CSRD

A key difference lies in the significantly expanded scope of application. The NFRD applied to large public interest entities with more than 500 employees. These included, in particular, capital market-oriented companies, banks and insurance companies. The group of companies subject to reporting requirements was therefore comparatively limited.

The CSRD expands this scope considerably. Depending on the final legal status, it covers in particular

- large companies within the meaning of the EU Accounting Directive,

- Parent companies of large groups,

- Listed small and medium-sized enterprises (SMEs with special regulations),

- certain non-EU companies with significant business activities in the EU.

This significantly increases the number of companies potentially subject to reporting requirements. While around 11,000 companies were affected under the NFRD, the number may increase many times over under the CSRD, depending on the political design. The aim of this expansion is to create a more level playing field and to make sustainability information accessible to more than just a small group of large companies.

Stricter reporting obligations and standards

In addition to the expanded scope, the CSRD differs primarily in terms of the quality and binding nature of the reporting obligations. Under the NFRD, companies were able to report with comparative flexibility. Although certain topics had to be addressed, there were no detailed, binding European standards. The reports were therefore often structured differently and difficult to compare in terms of content.

The CSRD fundamentally changes this:

- Reporting is carried out in accordance with the binding ESR).

- The principle of dual materiality is clearly anchored.

- Sustainability disclosures must be integrated into the management report.

- An external audit obligation is introduced (initially with limited security).

- In future, the reports are to be published in digital form.

These requirements make reports significantly more comparable, comprehensible and auditable. This makes sustainability reporting more standardized and brings it closer to the logic of financial reporting.

While the NFRD was primarily intended to promote transparency, the CSRD is also aimed at standardization, reliability and integration into corporate management. For companies, this means: the effort involved increases, but at the same time a clear framework is created that provides orientation and can lead to more consistent processes in the long term.

Sanctions for non-compliance

Types of sanctions: Fines and other consequences

Although the CSRD itself does not specify the level of fines, it obliges the member states to introduce appropriate sanctions for breaches of the reporting obligations. These include, for example:

- Administrative fines for missing or incorrect reporting

- Orders to rectify or disclose corrected information

- Public announcement of violations (naming and shaming)

- In certain cases, supervisory measures against board members

As the CSRD is transposed into national law in every EU country, the specific sanctions are not the same everywhere. In Germany, for example, enforcement is carried out via existing commercial and supervisory procedures, such as the Federal Office of Justice in the case of disclosure obligations or the capital market supervisory authority in the case of listed companies.

It is also important to note that sustainability information will be included in the management report in future and will be audited externally. If information is incorrect or incomplete, this can therefore also have legal consequences, especially if investors base their decisions on this information.

Supervisory authorities and their role

Compliance with the CSRD is primarily monitored by national authorities. Which authority is responsible depends on how the directive has been implemented in the respective country and which supervisory structures are already in place. In practice, several players are often involved: for example, authorities from the commercial or judicial sector when it comes to disclosure obligations and formal requirements for the management report. In the case of capital market-oriented companies, financial market supervisory authorities often also come into play, as sustainability disclosures are increasingly becoming part of regulated corporate reporting.

The mandatory external audit also plays a key role. The sustainability information is not simply published, but checked by auditors or auditing companies. This noticeably raises the bar: The content, database and documentation must be prepared in such a way that they can be clearly understood and verified.

At EU level, the CSRD will be linked to the existing accounting and capital market reporting rules. The European Securities and Markets Authority (ESMA) plays an important role here - especially when it comes to digital reporting obligations and the question of how sustainability disclosures will be embedded in existing reporting formats in future.

Reputational risks and potential loss of business

In addition to formal sanctions, the economic and reputational effects are often just as relevant. The CSRD significantly increases transparency. Incomplete, contradictory or incorrect information can therefore have negative consequences, even if no direct fines are imposed.

Possible consequences are

- Loss of confidence among investors and financial institutions

- Limited access to sustainability-related financing

- Reputational damage due to public criticism

- Competitive disadvantages compared to more transparent companies

What's more: Sustainability data is playing an increasingly important role, for example in supply chains, customer requirements or financing discussions. If you can't deliver here, in case of doubt you won't lose out because of a fine, but because business opportunities will be lost elsewhere.

CSRD therefore not only works via formal sanctions, but also via market mechanisms. Sustainability reporting is becoming a factor for competitiveness and corporate reputation.

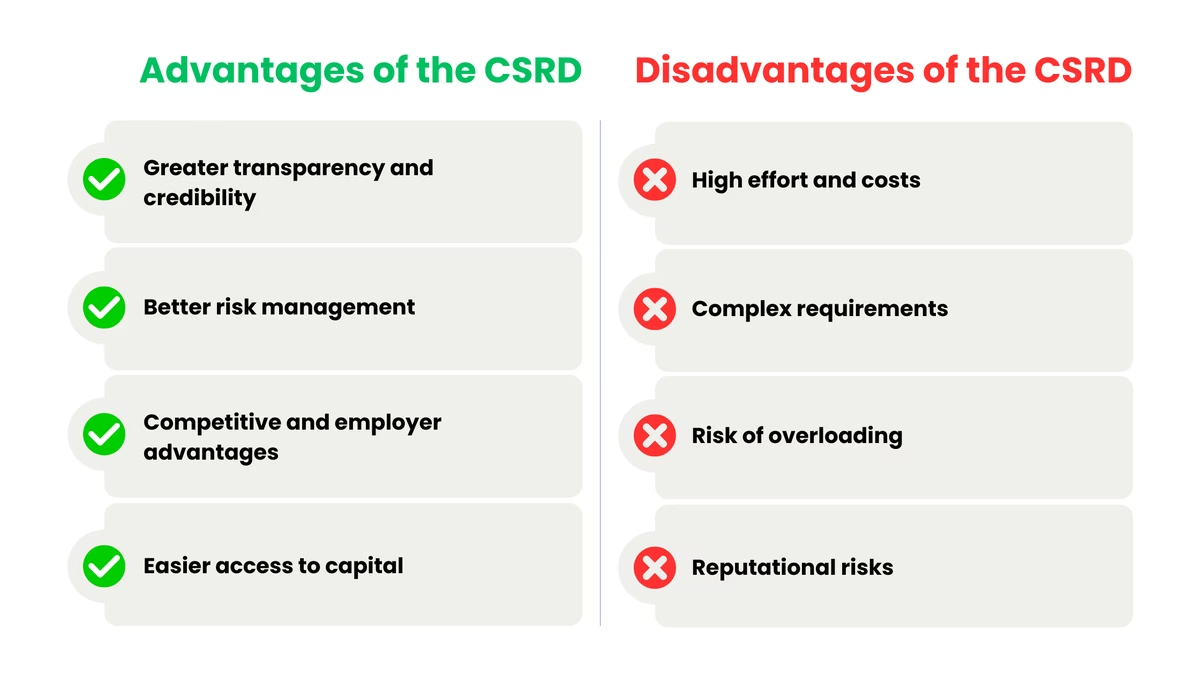

Advantages and disadvantages of reporting

The new EU regulation on corporate sustainability is an important step towards better reporting on environmental and social issues. It obliges companies to disclose their work on environmental, social and governance(ESG) issues. This should ensure that information on sustainability is easier to understand and compare. Although this rule brings many benefits, such as greater clarity for companies, investors and the general public, it also presents some challenges.

Advantages of sustainability reporting

More transparency and credibility

Those who present ESG issues in a comprehensible manner create trust among investors, customers and the public. If the reporting also remains consistent over the years, this strengthens the company's reputation and helps to credibly position the company as responsible.

Better risk management

When companies systematically record environmental and social risks, they often recognize problems earlier and can take more targeted countermeasures. This makes them more resilient, for example in the event of new requirements, changes in the market or rising stakeholder expectations.

Competitive and employer advantages

Transparency can be a differentiating factor towards customers, in competition and in recruiting. Companies with clear sustainability goals and measurable progress often appear more attractive to talent and business partners.

Easier access to capital

Investors and banks are increasingly looking at ESG criteria in their assessments. Those who report reliably here often have better cards in financing discussions, including for sustainability-related financing.

Disadvantages and typical challenges

High effort and costs

The effort involved is particularly noticeable at the beginning: data needs to be collected, processes and systems need to be put in place, internal controls need to be established and employees need to be trained. Depending on the initial situation, external support may also be required.

Complex requirements

The requirements are detailed and require a good understanding of the standards and processes. Smaller companies in particular reach their capacity limits more quickly, even if they are only indirectly affected (e.g. via supply chain inquiries).

Risk of overloading

Comprehensive reports can become confusing if the essentials and structure are not clearly defined. This results in "lots of content" but little clarity.

Reputational risks

Greater transparency also means that weaknesses become more visible. If targets are not achieved or data appears inconsistent, this can trigger criticism. At the same time, honest and comprehensible reports create trust in the long term.

Example of a report

A sustainability report shows what a company is doing for the environment, society and good corporate governance (ESG). A clear report not only shows that the company complies with the rules, but also how seriously it takes sustainability. Using the example of an invented company, "GreenTech Innovations", we show what such a report could look like.

A CSRD report could look like this

Set goals and rules: First, GreenTech Innovations considers goals and rules for the sustainability report. The company wants to show how well they are reducing CO₂ emissions, implementing a circular economy and ensuring diversity and cohesion in the workplace.

Talk to stakeholders: To find out the important points, GreenTech talks to various stakeholders, such as employees, customers, suppliers and people from the surrounding area.

Materiality analysis: GreenTech uses a materiality analysis to find out which sustainability issues are really important, both for the company and for interested parties.

Data collection: In the next step, GreenTech collects figures and information on energy consumption, waste management and employee satisfaction.

Structure of the report: GreenTech's sustainability report is divided into various important sections:

- Start and overview: What the company understands by sustainability and how it intends to tackle it.

- Environmental protection: How the company reduces emissions, saves energy and reduces waste.

- Social commitment: information on working conditions, diversity in the team and projects for the community.

- Governance: How the company is managed and adheres to fair business rules.

- Future plans: What the company wants to achieve in the next few years.

Creation and design: The report should be written in such a way that the core message is easy to understand. It also includes infographics, diagrams and case studies to better illustrate the information. GreenTech focuses on openness and honesty by showing both the successes and the difficulties.

External review: Before GreenTech publishes the report, another company reviews the information. This ensures that everything is correct and trustworthy.

Publication: The final sustainability report is published on the company's website. It is shared on social networks and through press releases to ensure that it receives sufficient coverage and attention.

Feedback and discussions: In order to obtain different opinions on the report, GreenTech engages in an exchange with various interest groups.

Continuous improvement: Following an internal review, GreenTech attempts to apply the feedback and suggestions for improvement to the report. On this basis, plans are developed for further steps to increase sustainability.

The example illustrates how a company can prepare a detailed report on its environmental performance. The report not only provides information about what the company has achieved so far, but also what it would like to implement in the future in order to continue to act in an environmentally friendly manner.

Conclusion

The importance of CSRD makes sustainability reporting in Europe much more binding. In future, companies will no longer report according to their own formats, but according to the ESRS. The sustainability indicators will then be integrated into the management report, subject to mandatory auditing and increasingly digitally readable. This brings sustainability closer to normal corporate management: materiality, risks, targets, measures and governance must not only be described, but also backed up with reliable data and clearly documented.

For companies, this initially means more work. Above all, data processes must be set up properly, responsibilities clarified and documents prepared in such a way that they stand up to scrutiny. At the same time, however, the CSRD also provides guidance. Those who set up robust ESG reporting at an early stage save time and friction later on, manage internally better and can respond more consistently to requests from banks, customers or the supply chain. It is crucial not to see the CSRD as a one-off reporting project, but as a change process that is built up and improved step by step over several reporting years.

Frequently asked questions

The CSRD (Corporate Sustainability Reporting Directive) is a European directive that obliges companies to report comprehensively on their sustainability performance. It replaces the previous NFRD and significantly expands the requirements by including more companies and requiring more detailed ESG (environmental, social and governance) information. The aim is to create transparency and comparability so that investors and other stakeholders receive reliable data on the sustainability impact of companies. Reporting is carried out in accordance with the ESRS (European Sustainability Reporting Standards) and must be audited externally. Large companies will be affected from 2024, followed by SMEs and non-EU companies in subsequent years.

CSRD reporting primarily affects large companies that meet at least two of the three criteria: more than 250 employees, a balance sheet total of more than 20 million euros or a turnover of more than 40 million euros. From 2026, capital market-oriented small and medium-sized enterprises (SMEs) will also have to report, although simplified requirements will apply to them. In addition, non-EU companies that operate in the EU and generate a turnover of more than 150 million euros there are required to report, provided they have a subsidiary or branch in the EU. It will be introduced gradually from 2024, starting with large capital market-oriented companies, thus significantly expanding the group of companies subject to reporting requirements.

The CSRD aims to improve the transparency and comparability of sustainability information in companies. It is intended to ensure that investors, consumers and other stakeholders receive reliable and consistent information on the environmental, social and governance (ESG) aspects of a company. Mandatory reporting is intended to encourage companies to better manage their sustainability strategy and risks and promote sustainable business practices. In the long term, mandatory sustainability reporting supports the achievement of European climate targets and contributes to the implementation of the European Green Deal.

Companies must disclose detailed information on environmental, social and governance issues. This includes information on greenhouse gas emissions, energy consumption, working conditions, diversity, corporate governance and anti-corruption measures. Reporting is carried out in accordance with the ESRS and is based on the principle of dual materiality - in other words, companies must take into account both their impact on the environment and society as well as financial risks through sustainability factors. The information must be presented qualitatively and quantitatively and externally audited to ensure transparency and credibility.

The CSRD significantly expands the previous NFRD by extending the scope of application to all large companies and, from 2026, to capital market-oriented SMEs. In contrast to the NFRD, companies must now report more detailed information on ESG issues in accordance with uniform ESRS standards and take into account the principle of double materiality. In addition, an external audit requirement has been introduced to increase the credibility of the reports. Another difference is the obligation to publish digitally in a machine-readable format in order to improve comparability and accessibility. The CSRD thus makes sustainability reporting more comprehensive, more binding and more transparent.

The European Sustainability Reporting Standards developed by EFRAG apply to reporting. These standards define the information that companies must disclose on environmental, social and governance issues. They consist of general standards that define basic reporting principles and the concept of double materiality, as well as thematic standards that cover specific ESG aspects such as climate change, working conditions or corporate governance. The ESRS ensure clear, uniform and comparable requirements so that companies can present their sustainability performance transparently and comprehensively.

To prepare your company for the CSRD, you should first take stock and check existing sustainability data for gaps. Identify relevant topics using double materiality and establish effective data management to collect and validate ESG data. Establish clear processes for reporting according to ESRS standards and use internal or external experts as needed. Training and a pilot report can optimize the process and ensure that requirements are met on time.

Non-compliance may result in financial penalties and other legal sanctions determined by the EU member states. In addition, a lack of or inadequate reporting can lead to significant reputational damage and damage the trust of investors, customers and other stakeholders. Companies that do not comply with ESG transparency requirements also risk more difficult access to capital, as financial institutions and investors place greater emphasis on sustainability data. In the long term, the lack of reporting can lead to internal company risks remaining unrecognized, which could result in economic and operational disadvantages.

The directive affects small and medium-sized enterprises (SMEs) in particular if they are capital market-oriented. From the 2026 financial year, these SMEs will be obliged to report on sustainability, although they will be subject to simplified requirements compared to large companies. Non-listed SMEs are generally exempt from the obligation, but may be indirectly affected if they are part of supply chains of large companies that require ESG data from their partners.

For SMEs, the CSRD primarily means additional administrative work, as they have to set up processes for data collection and reporting. At the same time, it offers opportunities by helping SMEs to make their sustainability performance more transparent and strengthen their competitiveness in the market.

Sustainability goals and risks play a central role in reporting, as companies must disclose their strategic goals and progress in the environmental, social and governance areas. At the same time, they are obliged to disclose risks to the environment and society that arise from their business activities or that affect their company due to external factors such as climate change. The dual materiality requires consideration of both the company's impact on the environment and the financial risks posed by sustainability issues. This reporting creates transparency and enables stakeholders to better assess the company's sustainability strategy and resilience.

Dual materiality means that companies must consider and report on sustainability aspects from two perspectives:

- Inside-out perspective (impact materiality): This is about how the company influences the environment and society through its business activities. This includes, for example, CO₂ emissions, effects on biodiversity or social issues such as working conditions.

- Outside-in perspective (financial materiality): This perspective looks at how external sustainability factors (e.g. climate change, scarcity of resources) can affect the company financially, for example through increased costs or risks for the business strategy.

Dual materiality ensures that both the company's impact on its environment and the risks and opportunities arising from sustainability aspects are presented transparently. This gives stakeholders a comprehensive picture of a company's sustainability performance and risks.

The reporting must be externally audited and validated by independent auditors or accredited audit bodies to ensure the quality and credibility of the information. This involves checking whether the reports comply with the ESRS and whether the principles of double materiality are adhered to. The review process assesses the completeness, consistency and comprehensibility of the sustainability data in comparison to other company reports. Initially, a "limited assurance" is performed, which could be expanded to a "reasonable assurance" in the long term. This increases transparency and ensures the comparability of reports between companies.

The CSRD offers companies the opportunity to present their sustainability performance in a transparent and comparable manner, thereby strengthening the trust of investors, customers and stakeholders. Standardized reporting helps to identify risks at an early stage, improve internal processes and develop a sustainable business strategy. It also facilitates access to capital, as many investors are increasingly focusing on ESG-compliant companies. Overall, it promotes the long-term competitiveness and future viability of companies.

Alexander Hilmar

LinkedInESG compliance expert - lawcode GmbH

Alexander Hilmar advises companies on the implementation of ESG compliance, sustainable reporting and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.