Important facts

- What is the SFDR?

- The Sustainable Finance Disclosure Regulation (SFDR) is an EU regulation that obliges financial market players to disclose their sustainability strategies and risks.

- Who is affected by the SFDR?

- The SFDR applies to financial market participants and financial advisors, including asset managers, insurers, banks, pension funds and asset managers.

- What is the aim of the SFDR?

- It aims to create transparency, prevent greenwashing and enable investors to make informed decisions based on sustainability-related information.

- What must be disclosed?

- Companies must explain how they incorporate sustainability risks into their decisions and whether negative impacts on ESG factors are taken into account.

- How does the SFDR relate to the taxonomy?

- It complements the EU taxonomy by providing transparency requirements for financial products, while the taxonomy provides the substantive definition of environmental sustainability.

- What are the challenges?

- Complex data collection, ongoing regulatory adjustments and the interaction with other EU regulations such as CSRD or taxonomy make implementation challenging.

Summary: The SFDR

The Sustainable Finance Disclosure Regulation (SFDR ) is part of the EU Sustainable Finance Framework and is intended to promote sustainable investments and curb greenwashing. It has been in force since March 10, 2021 and obliges financial market participants (e.g. banks, asset managers, funds) to disclose ESG information and take sustainability risks into account.

The SFDR distinguishes between company-related and product-related disclosures. Financial products are classified into three categories: Article 6 (no or low ESG integration/justification), Article 8 (environmental and/or social characteristics) and Article 9 (sustainable investment objective).

For companies, this means more transparency and data requirements, but also the opportunity to strengthen trust and meet the growing demand for sustainable products.

Updates & news on SFDR

The SFDR continues to evolve, which is precisely why it is worth taking a brief look at the current status. It is important to note that the current rules continue to apply, while the EU Commission has proposed a reform (SFDR 2.0) at the end of 2025. This is not yet final, but clearly shows where the journey is heading.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

SFDR 2.0: What the EU Commission wants to change

With the reform proposal, the Commission wants to make the SFDR simpler and easier to understand for companies and investors. The focus is on less complexity and more clarity, particularly with regard to greenwashing.

Planned innovations at a glance:

- Less disclosure at company level: The PAI statement at company level (Principal Adverse Impacts) is to be omitted under the proposal.

- Leaner information for private investors: shorter, more focused information instead of very extensive templates.

- New, voluntary product categories (instead of Article 8/9 as a label):

- Sustainable (products with a sustainable goal/contribution)

- Transition (products with a credible transformation path)

- ESG basics (ESG approaches without sustainable/transition quality)

- Clearer minimum requirements: For categorized products, a high portfolio share (70%) in line with the strategy and exclusions for certain harmful activities are provided for, among other things.

- Stricter rules for ESG terms in marketing: ESG claims should be more closely linked to these categories.

What will continue to apply until then

Until the legislative process is completed, the practice remains as before: Article 6/8/9, plus RTS templates for standardized disclosure.

In addition, there are ongoing interpretation aids:

- The European supervisory authorities last updated the consolidated Q&As on November 4, 2025, which is helpful for detailed implementation issues.

- The RTS were also adjusted in 2023 (including additional information on taxonomy-compliant gas and nuclear activities in the templates).

Practically important for communication

It is currently particularly relevant for companies that ESG statements in product names and marketing are under closer scrutiny. This also includes the ESMA guidelines on fund names with ESG/sustainability terms (e.g. thresholds and exclusions).

SFDR: Definition and background

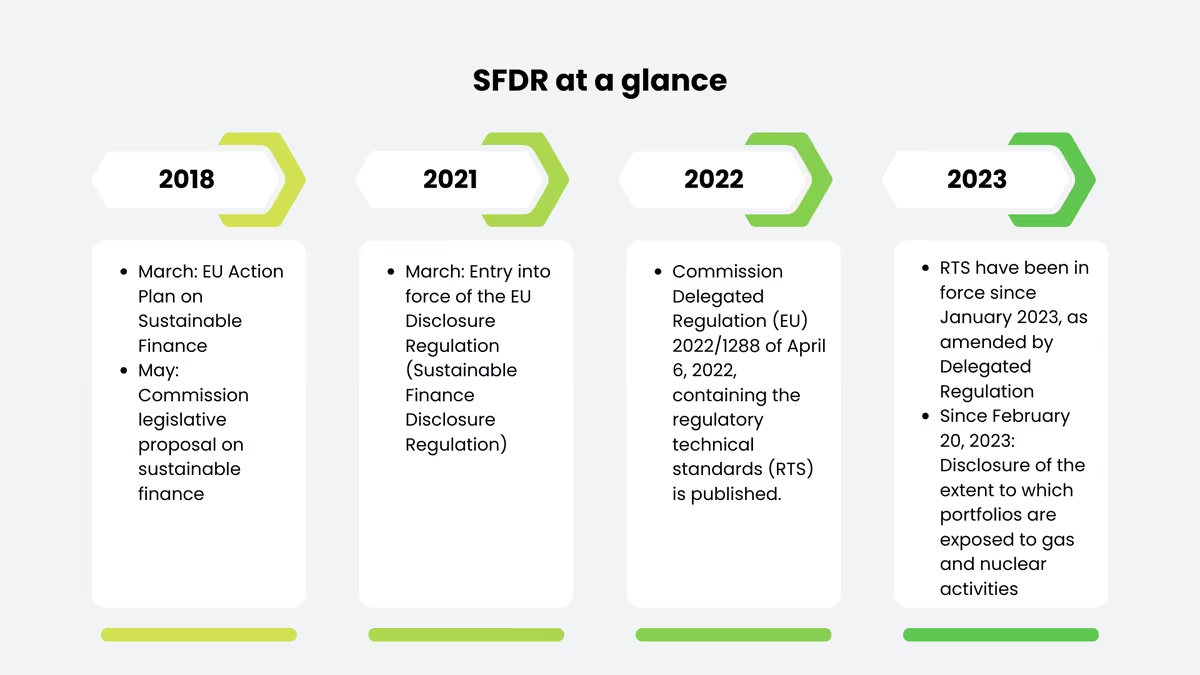

When did the SFDR come into force?

The Sustainable Finance Disclosure Regulation (SFDR) came into force on March 10, 2021 and contains a large number of disclosure requirements. With its introduction, the European Commission has created an important instrument for promoting transparency in the financial sector. Companies and investors must now disclose more detailed information about their sustainable investment strategies and products. The Sustainable Finance Disclosure Regulation affects asset managers and applies to a wide range of market participants, including financial institutions, asset managers and investment funds. The disclosure of environmental, social and governance(ESG) criteria is intended to enable investors to make informed decisions that have a positive long-term impact on sustainability. In this way, the SFDR helps to strengthen the market for sustainable investments and promote responsible capital allocation.

Delegated Regulation & RTS: What has been specified and when?

The SFDR is the framework. To turn the framework into concrete, comparable information, the EU has supplemented the requirements via a Delegated Regulation (the so-called Regulatory Technical Standards - RTS). These standards specify what information must be disclosed, how it is to be calculated and in what form it is to be presented (e.g. using fixed templates).

The most important milestones in practice:

- Since January 1, 2023: The RTS (Level 2 rules) are binding, including standardized templates for pre-contractual information and regular reports.

- Since February 20, 2023: The RTS have been amended again (including additions/refinements in the appendices and additional clarifications, particularly where products also reflect taxonomy references).

- Ongoing interpretation (important for implementation): The European supervisory authorities regularly update their Q&As to clarify typical practical issues. The most recent consolidated version was published in November 2025.

Update: SFDR 2.0 is in progress (as of January 2026)

There is a central update in parallel to the current regulations. The EU Commission has proposed a reform of the SFDR (SFDR 2.0) at the end of 2025. This is not yet final, but it shows what companies and market participants should prepare for in the medium term.

The direction is clear:

- Simplification of disclosures (less complexity, simplification of content that is difficult to understand)

- More clarity in product categories (less article-8/9-label logic, more clear classification)

- Stronger guard rails against greenwashing, especially for statements in marketing and product communication

What does the Disclosure Regulation say?

The Disclosure Regulation is intended to create greater transparency and clarity with regard to sustainable investments. It requires financial market participants and financial advisors to disclose information on environmental, social and governance criteria in order to inform investors about the sustainability of their investments. The Disclosure Regulation consists of two main parts: the obligation to disclose sustainability information and the obligation to integrate sustainability risks into the investment decision-making process. This should enable investors to make better decisions that are both financially profitable and take into account positive environmental and social impacts.

Who is subject to the disclosure obligation?

The Sustainable Finance Disclosure Regulation plays a crucial role in the financial sector, as it provides a clear framework for the integration of sustainability aspects into investment strategies. According to Article 2 of the SFDR, the regulation covers financial market participants such as investment funds, asset managers, pension funds, insurance companies and financial advisors. However, the regulation applies not only to EU-wide companies, but also to third countries such as Switzerland, provided that they offer their services within the EU or have their registered office there. Overall, the regulation should help to improve transparency and comparability in the area of sustainable finance and enable investors to make informed decisions.

Differences between company-related and product-related disclosure obligations

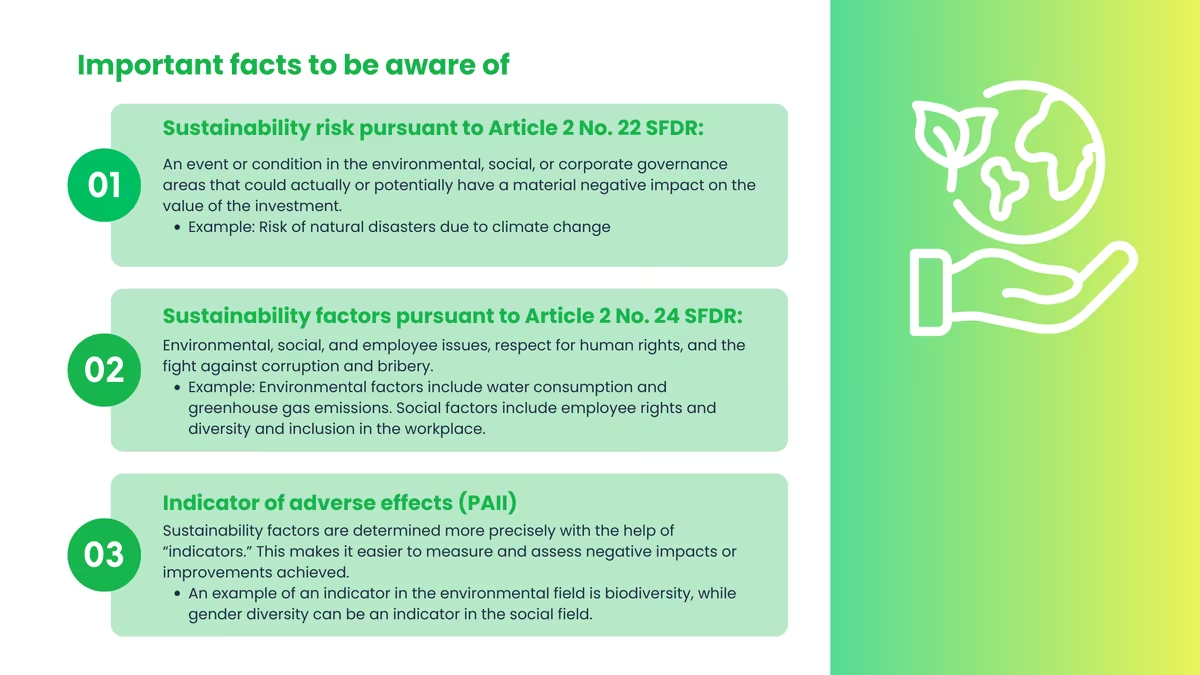

Among the company-related disclosure obligations, Article 4 SFDR is essential, as it regulates the PAI statement (Principal Adverse Impacts Statement), which requires transparency on the websites of financial market participants. Specifically, this means that financial market participants must provide information on whether they take into account the principal adverse impacts of investment decisions on sustainability factors. If they do so, they are obliged, for example, to disclose the nature and scope of their activities, including their carbon footprint. If the adverse impacts on sustainability factors are not taken into account, they must justify this.

Articles 6, 8 and 9 SFDR are relevant with regard to product-related disclosure obligations. Accordingly, financial market participants must provide information on the consideration of sustainability risks in their investment decisions for each financial product that meets the requirements of the EU Disclosure Regulation. Further requirements apply in particular if the various financial products are advertised with environmental and/or social characteristics (Article 8 SFDR) or marketed as a sustainable investment (Article 9 SFDR). Article 11 SFDR therefore applies to such financial products and provides for regular reporting on the extent to which these sustainability goals are achieved. In addition, Article 10 SFDR requires them to publish the information required under Articles 8, 9 and 11 SFDR on their website.

The EU Disclosure Regulation specifies the obligations in the Delegated Regulation, which sets out regulatory technical standards for the disclosure obligations under Articles 4, 7, 8, 9, 10 and 11 SFDR.

Role of transparency and reporting

Transparency and reporting play a central role in the Sustainable Finance Disclosure Regulation. Companies must disclose accurate information about their sustainability practices and objectives in order to meet the requirements of the regulation. This enables investors and other market participants to make informed decisions in line with their sustainability goals. Transparency promotes trust in the market and creates a solid foundation for sustainable investment. Through clear reporting, companies can effectively communicate their ESG performance and raise awareness of environmental and social issues. Transparent communication is crucial to achieve the goals and support the transition to a more sustainable finance industry.

Categorization of sustainability funds: How ESG criteria are shaping the future

The categorization of sustainability funds is an important step towards promoting sustainable investments. By providing clear guidelines and transparency, the regulations create a basis for investors to better understand the sustainability of funds. Taking ESG criteria into account, the regulation enables a differentiated classification of investment products. Investors thus receive well-founded information on the sustainability level of a fund and can invest in ESG-compliant products in a more targeted manner. The categorization also serves to protect investors' interests and promotes trust in the sustainable financial market. Companies are required to fully comply with the disclosure obligations under the regulation in order to present their sustainability efforts transparently and position themselves positively in the market.

3 Product classes according to SFDR

Before we get into the three product classes under Articles 6, 8 and 9, a brief update on the current status: The Article 6/8/9 logic still applies, but is currently undergoing further political development. In November 2025, the EU Commission presented a reform proposal for SFDR 2.0. The aim is to simplify disclosures and create a clearer category system; until then, Art. 6/8/9 will remain the standard.

The SFDR categorizes according to 3 product classes

These more traditional financial products take ESG characteristics into account in the investment decision or explain why sustainability risks were not considered relevant. This is also known as "comply or explain". The financial product does not meet the additional criteria of Articles 8 and 9 SFDR.

These products advertise with ecologically sustainable and/or social features.

These financial products describe themselves as "sustainable investments" and strive to achieve sustainable goals.

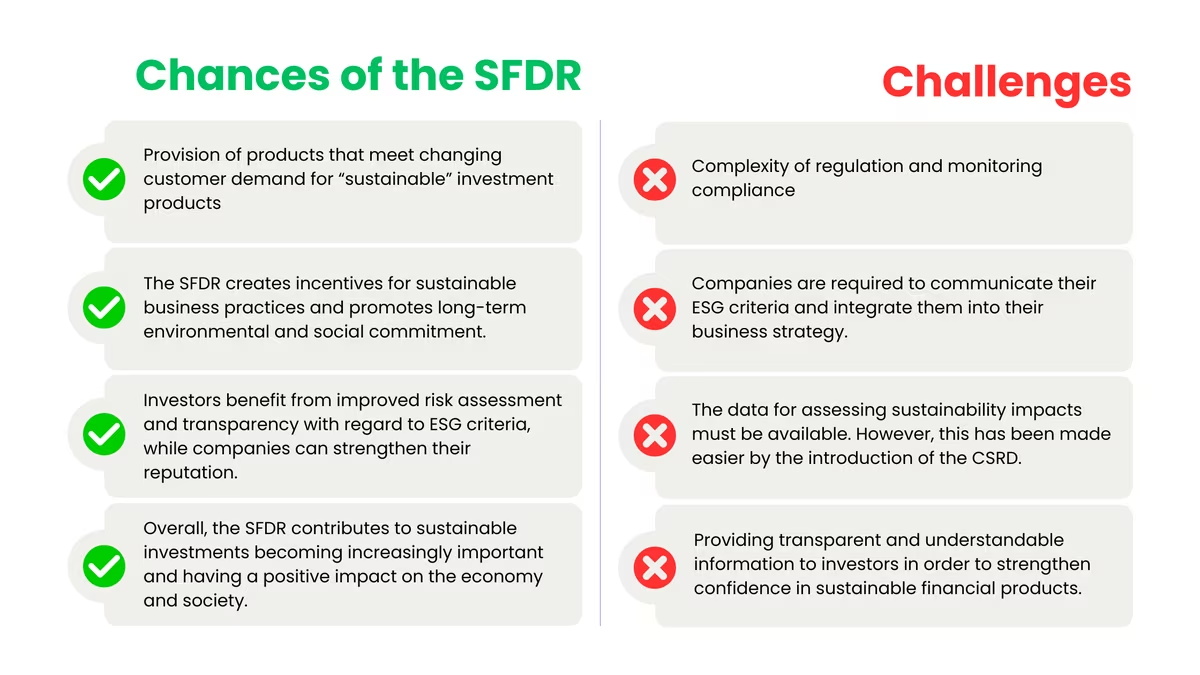

Challenges and opportunities

The integration of environmental, social and governance criteria in accordance with the regulation is of crucial importance for companies. By taking these criteria into account, they can not only minimize environmental and social impacts, but also create long-term value. The SFDR framework sets out clear requirements for the disclosure of these criteria to promote transparency and accountability. Companies that incorporate ESG factors into their investment decisions are actively contributing to sustainable development while meeting regulatory requirements. Integrating the criteria offers an opportunity to drive positive change and be successful in the long term, but also comes with particular challenges. It is therefore essential that companies address the requirements of the regulation.

SFDR and other regulations

The EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD) and the Sustainable Finance Disclosure Regulation are components of a comprehensive "Sustainable Finance Framework" of the European Union, which defines sustainability criteria for various areas of the economy.

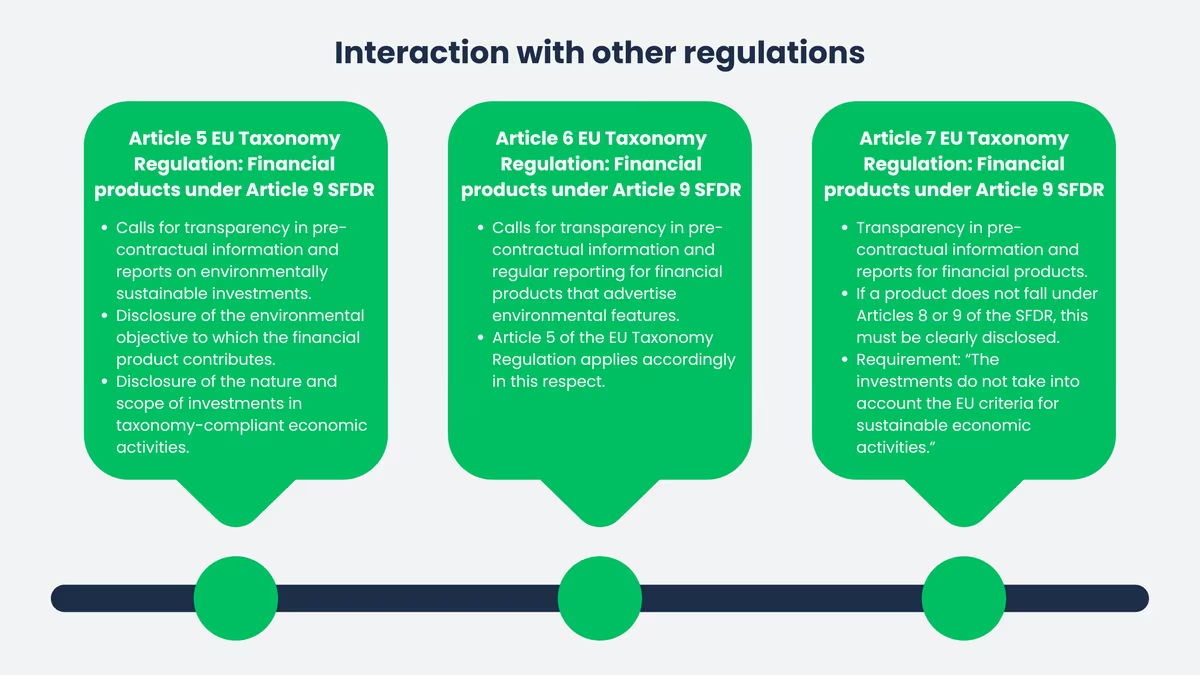

The EU taxonomy determines what is sustainable

The EU taxonomy provides the common definition of what is considered environmentally sustainable. The Taxonomy Regulation came into force on July 12, 2020. In practice, however, the criteria became applicable in stages (e.g. first for climate protection/adaptation from 2022, other environmental targets later).

For SFDR, the interaction is particularly relevant for Article 8 and Article 9 financial products: Since January 1, 2022, the product-related disclosure obligations have been supplemented by Articles 5 to 7 of the Taxonomy Regulation. This means that anyone advertising ecological features or sustainable goals must make transparent whether and to what extent investments are taxonomy-compliant (typically via a taxonomy quota).

Update on practice (taxonomy reporting becomes easier):

Delegated Regulation (EU) 2026/73 significantly simplified the taxonomy reporting requirements, including through a 10% materiality threshold that reduces detailed reviews and reporting for non-material activities/items. The amendments were published in the EU Official Journal on January 8, 2026 and have been in force since January 28, 2026 (with transition/options for first-time application).

The CSRD and SFRD also go hand in hand

CSR reporting is playing an increasingly important role in the corporate world: by publishing reports on environmental impact, social projects and ethical standards, companies demonstrate their responsibility towards society.

The CSRD came into force on January 5, 2023. The first wave will report for the first time for the 2024 financial year (reports will be published in 2025).

Update (schedule & scope in motion):

- The Stop-the-clock Directive (EU) 2025/794 postponed the start dates for later CSRD waves by two years, while the first wave remains unchanged.

- In addition, there is a provisional political agreement as part of the omnibus package (December 9, 2025), which would focus the CSRD more strongly on very large companies in future (including > 1,000 employees and > € 450 million turnover). This is an important trend, but it has not yet been finalized.

In practice, this means that CSRD data will become more standardized for many companies, but will come later depending on the wave, and this in turn affects how quickly financial market participants can back up their SFDR disclosures with reliable company data.

Tips for companies

Here are three practical tips for dealing with the regulation:

- The further development of the regulation should not be lost sight of: The guidelines and explanations of supervisory authorities such as the EBA, EIOPA and ESMA are constantly changing - so always stay up to date.

- Another important aspect is the interplay between SFDR, EU taxonomy and CSRD. It is essential to follow these developments closely in order to always be up to date.

- It is equally important to observe and take into account developments outside Europe. The global market for sustainable finance is constantly growing and international standards can have a significant impact on European regulation. We must therefore also keep an eye on trends and initiatives in other regions such as the USA or Asia.

It is therefore not only important to comply with static requirements, but also to keep up to date with new guidelines and explanations from the supervisory authorities. This is the only way to ensure that the requirements for sustainability and transparency in the financial sector are met.

Conclusion

The future prospects under the influence of regulation are promising. With its clear focus on transparency, responsibility and sustainability, it will drive positive change in the financial sector. Companies and investors will be increasingly encouraged to integrate ESG criteria into their decision-making processes and thus create long-term value. Increased disclosure of sustainability-related information will enable market participants to make more informed investment decisions while raising awareness of environmental and social issues. The SFDR will therefore not only improve financial performance, but also make an important contribution to the global shift towards a more sustainable economy.

Frequently asked questions

The Sustainable Finance Disclosure Regulation (SFDR) is an EU regulation that aims to increase transparency and comparability in the financial sector with regard to sustainable investments. It requires financial market participants and financial advisors to disclose how they consider sustainability risks in their decision-making processes - including the impact of sustainability risks on the return of financial products - and the potential negative impact of their investments on environmental, social and governance (ESG) factors.

The aim of the SFDR is to channel capital flows into sustainable economic activities and prevent greenwashing by enabling investors to make informed decisions based on standardized sustainability information.

The SFDR primarily affects financial market participants and financial advisors within the EU. Financial market participants include asset managers, fund providers, insurance companies and pension funds. These players are obliged to create transparency regarding the consideration of sustainability risks and factors in their investment decisions and advisory activities. The aim is to provide investors with clear and comparable information on the environmental, social and governance (ESG) aspects of the financial products on offer.

The SFDR also has an indirect impact on companies outside the financial sector. Financial institutions covered by the SFDR require detailed ESG information from the companies in which they invest or to which they offer financial products. Therefore, non-financial companies are also required to disclose their sustainability practices in order to meet the information requirements of financial market participants.

The SFDR obliges companies to comply with far-reaching transparency requirements. These oblige them to systematically disclose sustainability risks and the sustainability-related impacts of their investment decisions and advisory activities. These disclosures are made at company and product level and include

- Strategies for incorporating sustainability risks: Companies must explain how they take sustainability risks into account in their investment decisions.

- Consideration of adverse sustainability impacts: Companies with more than 500 employees are required to disclose the main adverse impacts of their investment decisions on sustainability factors.

- Product-related disclosures: Depending on the classification of the financial product (Article 6, 8 or 9 SFDR), specific information must be provided, in particular in pre-contractual documents, on the website and in periodic reports.

These measures aim to create transparency and enable investors to make informed decisions with regard to sustainable investments.

The SFDR classifies financial products into three categories in accordance with Articles 6, 8 and 9 in order to create transparency regarding the consideration of sustainability aspects:

- Article 6: Products that do not have specific sustainability features or do not take sustainability risks into account. Providers must disclose whether and how they include sustainability risks in their investment decisions or explain why these risks are not considered relevant.

- Article 8: Also referred to as "light green" products, they promote environmental and/or social characteristics without having an explicit sustainable investment objective. These products integrate ESG criteria into their investment process and must be transparent about how these characteristics are met.

- Article 9: Known as "dark green" products, they explicitly aim to achieve sustainable investment objectives. Such products specifically invest in activities that make a positive contribution to environmental or social objectives and must disclose in detail how these objectives are to be achieved.

This classification is intended to help investors make informed decisions and better understand the sustainability requirements of financial products.

The SFDR, the CSRD and the EU Taxonomy are central components of the EU framework for sustainable finance, each of which has a different focus. The SFDR requires financial market participants to disclose how they consider sustainability risks in their investment decisions in order to create transparency and prevent greenwashing. The CSRD expands the sustainability reporting requirements for companies by prescribing detailed disclosures on environmental, social and governance aspects in order to improve the quality and comparability of reports. The EU taxonomy serves as a classification system that defines which economic activities are considered environmentally sustainable, thus providing investors and companies with clear guidance for sustainable investments.

The Disclosure Regulation was introduced on March 10, 2021 and requires companies to comply with disclosure requirements regarding the integration of sustainability risks into their investment decisions. On January 1, 2023, the detailed technical regulatory standards (Level 2) came into force, which contain more precise requirements for these disclosures. As a first step, financial market participants are required to publish their first Principal Adverse Impacts (PAI) reports for the calendar year 2022 by June 30, 2023. This gradual implementation aims to increase transparency in the financial sector and promote sustainable investments.

Non-compliance with the requirements can have serious consequences for companies in the EU. The exact sanctions vary depending on the national legislation of the individual member states. In Germany, the Federal Financial Supervisory Authority (BaFin) monitors compliance with the SFDR obligations. In the event of violations, measures such as warnings, fines or other supervisory sanctions may be imposed. The amount of the fines depends on the severity of the breach and the relevant national legislation.

In order to meet the requirements, companies should assess their current ESG practices and collect the relevant data. Employee training is also important to ensure that all relevant individuals are aware of and can implement the SFDR requirements. In addition, companies must comply with mandatory disclosure requirements, including pre-contractual information, website publications and periodic reports. The integration of the strategy into company policy and the use of standardized templates from the European Commission also contribute to compliance.

First and foremost, it promotes transparency and comparability of sustainability information in the financial sector. By introducing standardized disclosure requirements, the regulation forces financial market participants to provide accurate and verifiable information on their sustainability-related practices and products. This makes it more difficult for companies to misrepresent themselves as environmentally friendly and protects investors from misleading information. However, there is debate as to whether the current categories are sufficient to effectively prevent greenwashing. Recently, EU advisors have proposed replacing the existing Article 8 and Article 9 categories with new classifications such as "Sustainable", "Transition" and "ESG Collection" to further increase transparency and minimize the risk of greenwashing.

The Sustainable Finance Disclosure Regulation increases transparency for investors by requiring financial market participants to disclose detailed information on the consideration of environmental, social and governance criteria in their investment decisions. This enables investors to make informed decisions and select investments according to their sustainability preferences. Standardized disclosure requirements increase comparability and trust in sustainable financial products, reducing the risk of greenwashing.

Matthias Klein

LinkedInESG compliance expert - lawcode GmbH

Matthias Klein advises companies on the implementation of supply chain laws such as the CSDDD and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.