Important facts

- What is the EUDR Regulation?

- The EU Deforestation Regulation (Regulation 2023/1115) obliges companies to ensure that certain products are deforestation-free and legally compliant.

- When does the regulation apply?

- Large and medium-sized companies must meet the requirements from December 30, 2026, while an extended deadline of June 30, 2027 applies to small and micro-enterprises.

- Which products are affected?

- The regulation covers seven raw materials and products made from them: Wood, beef, coffee, cocoa, soy, palm oil and rubber.

- What does deforestation-free mean?

- Products are considered deforestation-free if they do not originate from areas that have been deforested or degraded since December 31, 2020.

- Who is affected by the EUDR?

- All companies that place, supply or export relevant products in the EU.

- What are the main obligations?

- Companies must geolocate cultivation areas, analyze and mitigate risks and submit a due diligence declaration.

- What happens in the event of violations?

- Violations could result in penalties of up to 4% of annual turnover, a trade ban on the products concerned and public censure by the EU.

Summary - EUDR at a glance

The EU Deforestation Regulation (EUDR/VO 2023/1115) replaces the previous EU Timber Regulation (EUTR) and goes much further: it obliges companies to fulfill a comprehensive due diligence obligation before placing seven raw materials on the market. Specifically affected are wood, cocoa, coffee, soy, palm oil, cattle and rubber as well as all products made from them. Large companies must fully implement the regulations from December 2026. Small and medium-sized companies will not be affected by the regulation until July 2027. The three-stage process comprises information collection, risk assessment and risk mitigation, with transparency and traceability back to the cultivation area being crucial.

The regulation defines deforestation as the conversion of forests into agricultural land, regardless of whether it is caused by humans or not. The cut-off date is December 31, 2020: products may not originate from areas that have been deforested or damaged since then. The EUDR sets out clear responsibilities, not only in relation to deforestation, but also with regard to fair working conditions, human rights and, in particular, the rights of indigenous peoples.

Companies need to analyze their supply chains, clarify responsibilities, record geodata correctly and keep a constant eye on legal developments. Although the regulation entails additional effort, it also offers real opportunities: those who act early can build sustainable supply chains, strengthen long-term partnerships and position themselves better in a competitive environment.

Never miss an update on the EUDR again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

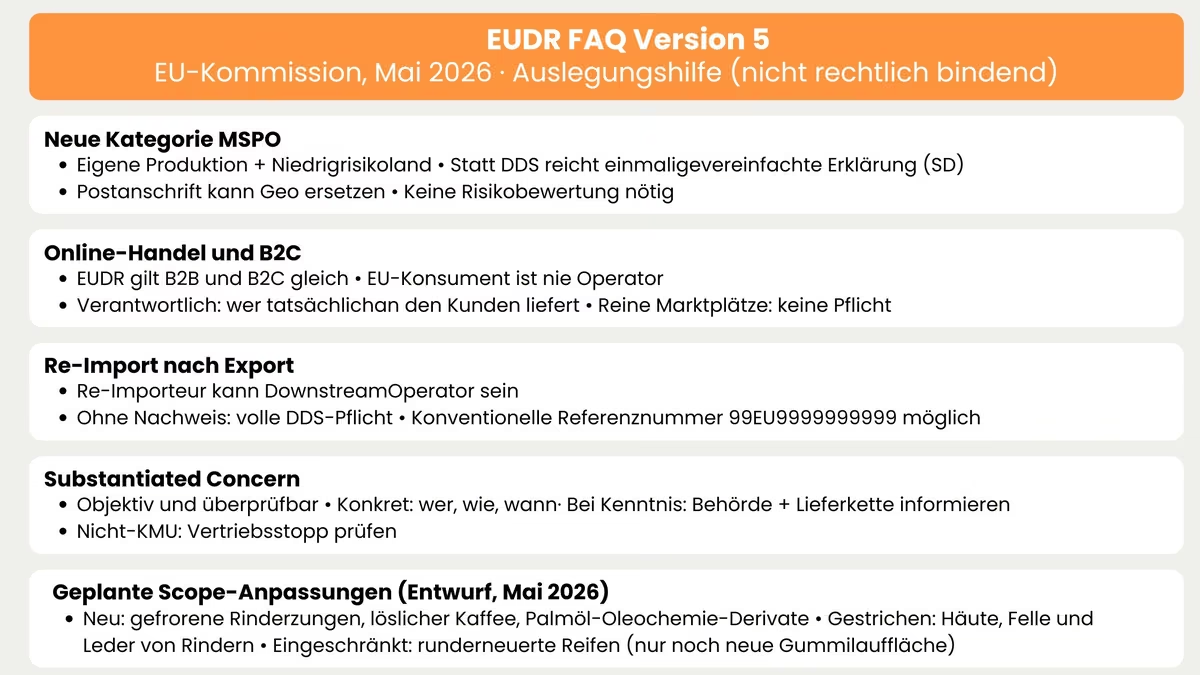

Update from 04.05.2026: FAQ version 5 of the EU Commission

In April 2026, the EU Commission published the fifth iteration of its FAQ document on EUDR implementation. Not yet legally binding, but an important interpretation aid for practitioners.

New category "Micro or Small Primary Operator" (MSPO)

Micro and small enterprises as well as natural persons who produce themselves (e.g. farmers or foresters) and place their products directly on the EU market benefit from simplified obligations, provided they are based in a low-risk country. Instead of a due diligence declaration (DDS), a one-off simplified declaration (SD) is sufficient and a risk assessment is generally not required. Under certain circumstances, the postal address may replace geolocation. If a Member State provides the necessary data from national databases, the SD is not required at all.

Clear rules for online trading and B2C business

The EUDR applies to all deliveries "in the course of a business activity", regardless of whether B2B or B2C. The entity that actually delivers the product to the customer - manufacturer, online retailer or fulfillment service provider - is always responsible. EU consumers, on the other hand, are never operators, not even for direct orders from abroad. Pure online marketplaces without a delivery function have no EUDR obligations.

Re-import of previously exported goods

Anyone who re-imports products that were previously carefully exported from the EU can be considered a downstream operator, even if they are processed in a third country. Instead of a separate DDS, a conventional reference number (format: 99EU999999999999) in the customs declaration is sufficient, provided the previous placing on the market can be clearly proven. Without proof: full DDS obligation.

Specification of "substantiated concerns" (Substantiated Concern)

A report must be objective and verifiable and have a clear reference to a specific company or a specific supply chain. General references to problems in the country of production are not enough, it must be specific: who, how and when. As soon as a company becomes aware:

- All downstream operators and traders must inform the competent authority and downstream actors immediately

- Non-SMEs must also check due diligence, until then a sales ban applies

- Member States must guarantee the protection of whistleblowers' identities

The following adjustments to the scope are also planned:

- New: frozen bovine tongues (HS ex 0206 21 00), soluble coffee (HS 2101 11 00), additional palm oil oleochemical derivatives (e.g. ex 1516 20, ex 2905 16, ex 3401 11 00)

- Deleted: Hides, skins and leather of bovine animals (ex 4101, ex 4104, ex 4107)

- Restricted: retreaded tires, obligations only for the new rubber tread (ex 4012 90 30)

The thrust is to close loopholes where it makes sense to do so and to reduce the burden where the cost and benefit are disproportionate.

All updates: EUDR current status

The thrust remains the same: deforestation-free, legally compliant supply chains. However, a lot has changed in three areas:

New deadlines: The application of the EUDR has been postponed further:

- Medium & large companies: from December 30, 2026

- Micro & small enterprises: from June 30, 2027

- Special case: Micro & small enterprises that were already covered by the EUTR will start from December 30, 2026

Relief for downstream players

In future, only the first distributor will submit the due diligence statement (DDS) in the EU system. Downstream market participants and traders will instead work with reference and identification numbers, which they must record, store and submit on request. This saves time and reduces sources of error due to duplicate data entry. But be careful: reducing the workload does not mean that downstream companies can tick the box. Clean traceability, complete data and functioning internal controls remain mandatory, otherwise it will quickly become problematic in the event of an audit.

Country benchmarking

Countries are officially divided into risk categories (low / standard / high). This has a direct impact on the depth of checks and effort required and should be taken into account in the procurement strategy and supplier management. The core remains unchanged: cut-off date 31.12.2020, legal production in the country of origin and the three-stage due diligence process (collect information, assess risk, mitigate risk).

On October 21, 2025, the EU Commission presented measures to make the introduction of the EU Deforestation Regulation (EUDR) more practicable for companies without weakening the core obligations. The regulation is still due to start on December 30, 2025. Only micro and small companies are to be given more time until December 2026 for full implementation, while medium-sized and large companies must fulfill their due diligence obligations by the end of 2025. In addition, only the first distributor is to submit a central due diligence declaration, downstream actors will be relieved and less effort will be required thanks to data integration and the avoidance of duplicate data entry. The whole thing will only come into effect if the EU Council and Parliament approve the proposal.

On 02.10.2024, the EU Commission proposed postponing the launch of the EUDR by 12 months because member states and international partners need more preparation time. The EU Parliament agreed on 14.11.2024. Following the trilogue negotiations, the EU Parliament and EU Council finally decided on the one-year delay on 03.12.2024. This means that the EUDR Regulation will apply to medium-sized and large companies from 30.12.2025 and to micro and small enterprises from 30.06.2026. An additional risk category ("no risk") proposed by the Parliament was rejected in the final text. Related deadlines have also been postponed, including the country classification according to deforestation risk to June 2025.

The EU Deforestation Regulation(EUDR): Definition, objectives & importance

What is the EUDR and why was it introduced?

The EU Deforestation Regulation(EUDR/VO 2023/1115) is the EU's response to a problem that is no longer far away: Deforestation and forest degradation are directly linked to global supply chains and therefore also to products that are traded, processed and consumed in Europe every day. The regulation obliges companies to prove that certain raw materials and products are deforestation-free and have been produced in the country of origin in accordance with the law. This is the definition of forest according to the EU regulation.

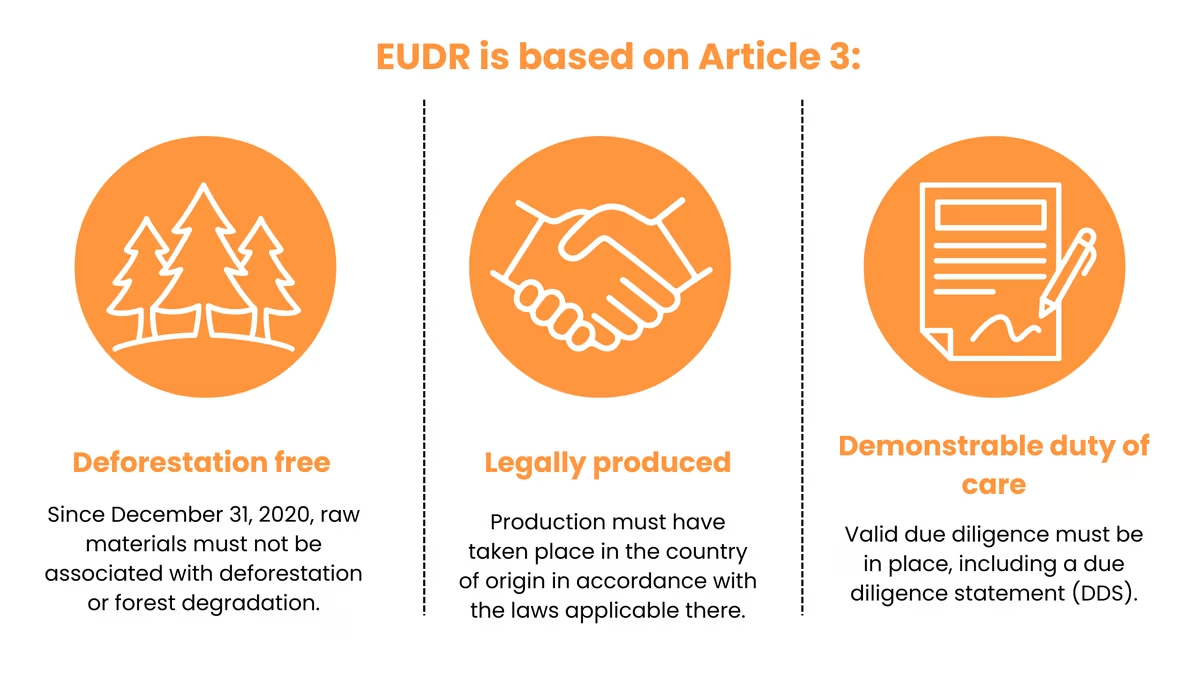

The Regulation is based on Article 3

A product may only be placed on the EU market or exported from the EU if three conditions are met simultaneously:

Deforestation-free: Since December 31, 2020, the raw materials must not be associated with deforestation or forest degradation.

Legally produced: Production must have taken place in the country of production in accordance with the laws applicable there (e.g. land use rights, relevant permits, labor and social regulations).

✅ Duty of care verifiable: A valid duty of care must be in place, including a declaration of due diligence (DDS) (depending on the role) and verifiable documentation.

The focus is on seven raw materials that are particularly relevant for deforestation risks according to EU logic: Cattle, cocoa, coffee, palm oil, soy, wood and rubber. This also includes products made from these raw materials (e.g. furniture, leather, chocolate, depending on the customs/product categories specified in the regulation).

The Deforestation Ordinance is based on a clear triad of due diligence obligations:

- Collect information (including supply chain, suppliers, product data and, above all, geolocation data on the cultivation/production area),

- Assess risk (incl. country and context factors),

- Reduce risk (if the risk is not negligible).

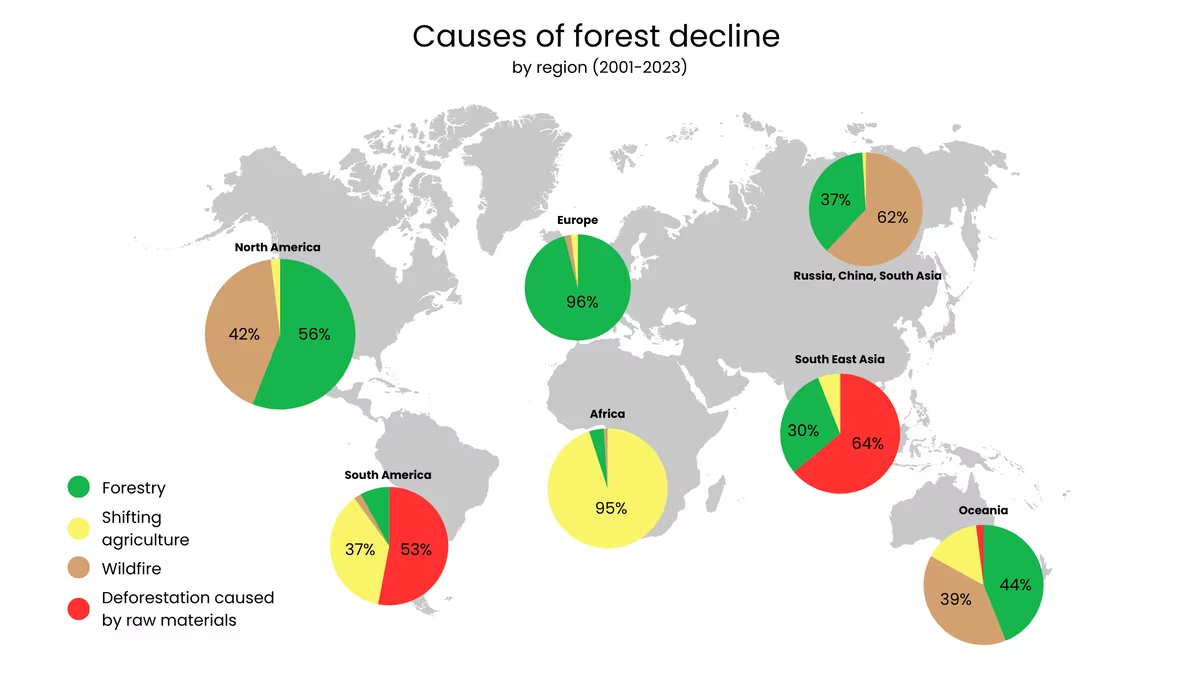

The realities on the corporate side show how great the need for action still is:

According to an iov42 study, around 18% of European timber importers are not even aware of the EU Deforestation Regulation. The Global Forests Report 2024 by CDP and the Accountability Framework Initiative also paints a sobering picture: of 881 companies surveyed, only 186 provided truly comprehensive information, and only 64 reported having achieved at least one completely deforestation-free supply chain.

Background and development of the regulation

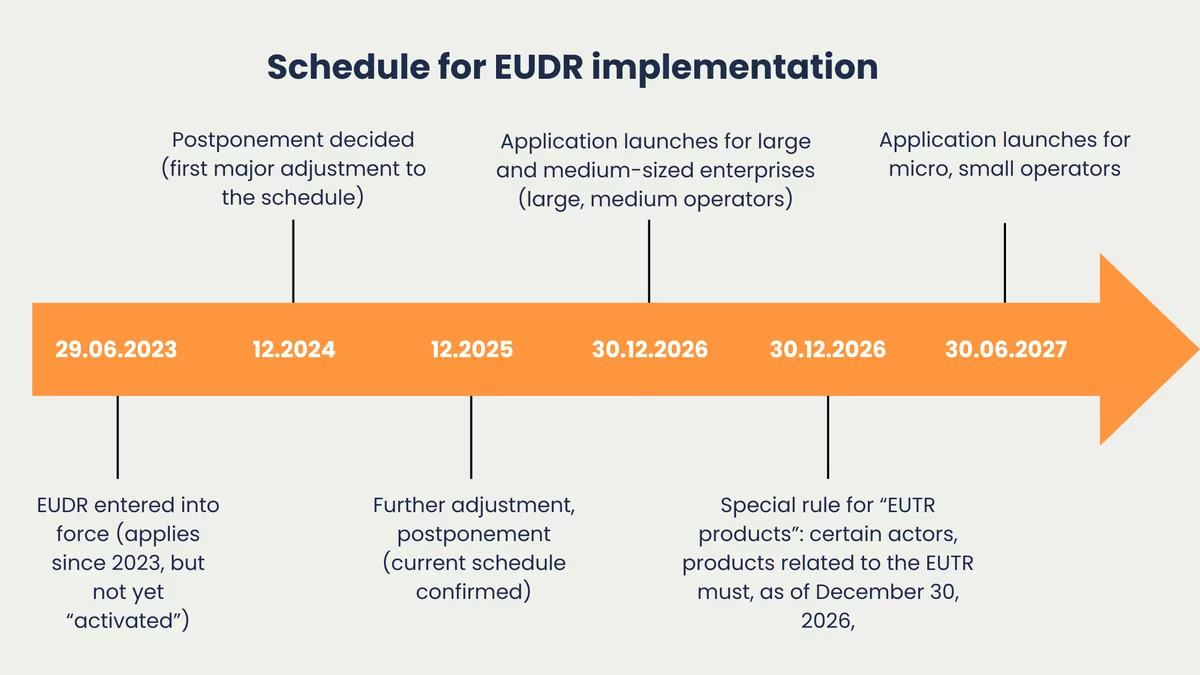

The Deforestation Regulation is not a quick fix, but the result of a political process lasting several years: Following the Commission's draft in November 2021 and the political agreement in December 2022, the Regulation formally came into force on June 29, 2023. The distinction between entry into force and application is crucial for companies. The latter was adjusted in December 2024 and again in December 2025 to make the introduction more feasible without abandoning the basic logic.

The current schedule (as of May 2026) is as follows:

- Large & medium-sized enterprises: Application from December 30, 2026

- Micro & small enterprises: Application from June 30, 2027

- Special case: micro/small enterprises that were already covered under the previous EU Timber Trade Logic (EUTR): December 30, 2026

At the same time, the EU has introduced targeted simplifications to avoid unnecessary duplication of work in the supply chain. One example is the due diligence statement: In principle, it should now only be submitted by the company that places the goods on the EU market for the first time. According to the amendment in the Delegated Act of May 2026, the timetable is no longer to be adjusted.

Importance of the EUDR for environmental and climate protection

The EU Deforestation Regulation is more than just another compliance project: it directly links environmental and climate protection with market rules. Forests are not only a source of raw materials, but also a carbon sink, a sanctuary for biodiversity and the livelihoods of many communities. Deforestation destroys ecosystems and exacerbates climate change in equal measure.

The Deforestation Regulation is intended to ensure that only products that have not been associated with deforestation since December 31, 2020 are traded in the EU. In addition, the products must have been legally produced in the country of origin, including the environmental and human rights requirements applicable there.

The bottom line is that the regulation creates a new minimum standard. Anyone who wants to take action in the EU must not only be aware of deforestation risks, but also prove, manage and document them.

Objectives of the EUDR

Reducing global deforestation through responsible sourcing

The EU Deforestation Regulation pursues a clear objective: deforestation and forest degradation should no longer be bought. To achieve this, the regulation is based on a principle that is particularly effective in practice: market access only for deforestation-free products. This turns responsible procurement from a best-practice issue into a concrete expectation for companies. Reliable evidence, good data and reliable suppliers are the basic prerequisites for this.

The objective behind this can be summarized in three points:

- Reduce deforestation pressure: Where the EU market sets clear requirements, incentives are provided to organize production without deforestation.

- Making risk supply chains visible: Lack of transparency is becoming a bottleneck - shifting priorities towards reliable data and clean origins.

- Strengthening responsibility along the supply chain: Risks should not be passed on, but actively managed, from procurement to market access.

Promotion of sustainable agricultural practices

In addition to forest protection, the EU Deforestation Regulation is also changing how agricultural supply chains will function in the future. The EU market is redefining what is considered deliverable and is therefore incentivizing more sustainable practices because they are more economically viable. Those who produce in a traceable manner, document cleanly and reduce risks will secure access to European supply chains.

In practice, this means that sustainability becomes more measurable, supplier development more important and short-term sourcing less attractive. Overall, the regulation shifts the understanding of sustainability away from pure voluntary commitments towards an implementation that works in purchasing, quality management and cooperation with suppliers in the long term.

Contribution to achieving the EU climate targets

Forests are climate stabilizers. If deforestation is reduced, carbon reservoirs are preserved, emissions are avoided and biodiversity is protected. For companies, the climate impact is particularly noticeable in two areas:

- Climate risks become supply chain risks: deforestation not only jeopardizes the environment, but also availability, prices and reputation.

- Evidence becomes crucial: The regulation makes politically set climate targets partially verifiable via supply chain logic.

The EUDR Regulation is therefore not just a forest protection rule, but a building block for making climate policy effective along global supply chains.

Sustainable development as a cross-cutting objective

The EU Deforestation Regulation makes it clear that sustainability is more than just green. It is not just about forest protection, but also about ensuring that supply chains are legally clean and social standards are adhered to, precisely because deforestation is often associated with land conflicts, unresolved rights and poor working conditions in practice. In practice, the regulation aims to achieve three things:

- Responsible procurement as standard, not as an add-on

- Better safeguarding of supply chains through clear requirements

- Greater credibility vis-à-vis the market, stakeholders and regulators

Obligations for companies

Introduction of due diligence obligations and risk assessments

In everyday life, this means above all that companies must set up their purchasing in such a way that deforestation and legal risks are identified early on and reduced where necessary. This requires a due diligence system that really works, not just as a document, but in the purchasing, quality, compliance and IT processes.

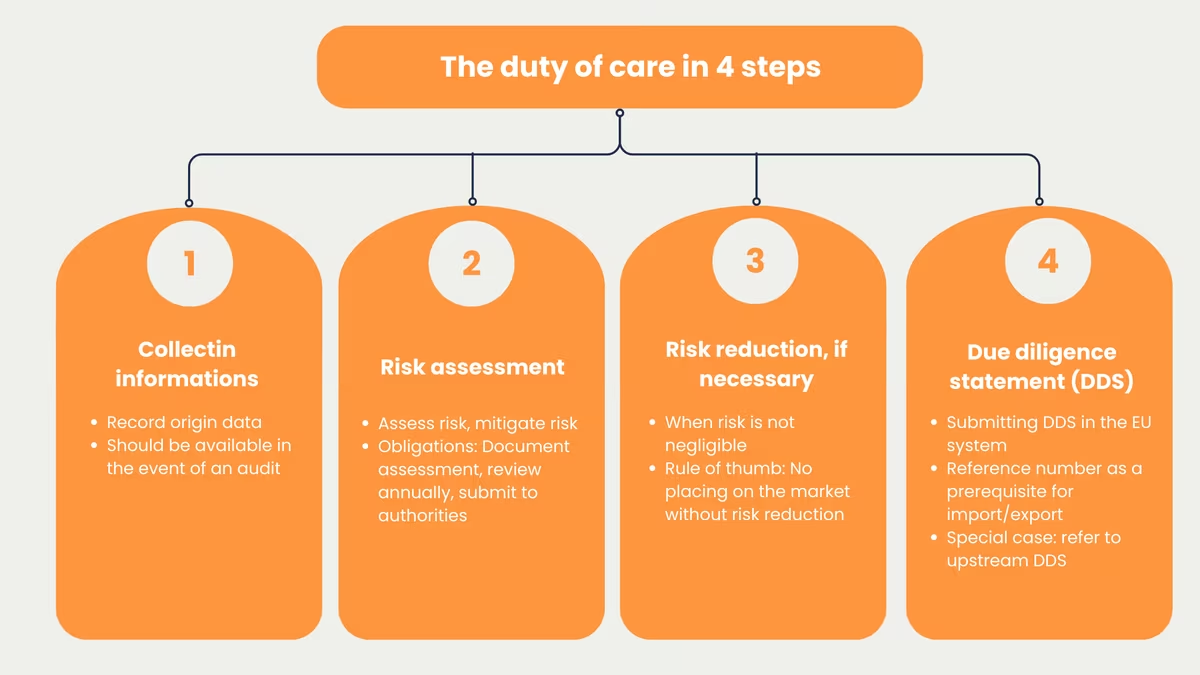

Essentially, the duty of care consists of four components:

- Collection of information

- Risk assessment

- Risk reduction if necessary

- Due diligence declaration (DDS)

What this means in practice

Due diligence starts with collecting all relevant information on the origin of the delivery. In practice, this often fails due to data quality, data formats and a lack of systematization. Geolocation data in particular must be available in a structured form and technically recorded in such a way that it can later be processed properly and used in the EU system.

At least the following information packages should be available for each flow of goods or batch and be retrievable for 5 years:

- Proof of deforestation-free status: Proof that the products are deforestation-free.

- Indication of origin: Country of production as well as geolocation of the cultivation or production areas and the production period.

- Quantity information: Quantity of goods (e.g. kg, volume, number of items).

- Supplier information: Name, address and e-mail address of all suppliers (depending on the chain: up to the relevant origin).

- Product description: Trade name, product type, raw materials contained and intended use.

- Legal conformity of production: Proof that raw materials have been produced in accordance with the relevant laws of the country of production.

- Customer information: Name, address and e-mail of the companies or retailers supplied.

Practical implementation: This information must be stored in such a way that it can be used quickly in the event of an audit.

Based on the information collected, market participants and non-SME traders check whether there is a risk of a breach. If a risk is identified, risk mitigation measures must be taken until only a negligible risk remains.

To-dos that are often underestimated in practice:

- Document risk assessments

- review or update regularly, at least annually

- Make results available to authorities on request

Criteria that belong in the risk assessment

- Producer country & regions: Risk status, presence of forests or indigenous groups, consultation or cooperation, legitimate land use or ownership claims.

- Environmental risks: Extent of deforestation or forest degradation in the country of production, reliability and validity of the information collected.

- Political & social factors: Corruption, falsification of documents, lack of prosecution, human rights violations, conflicts or existing sanctions.

- Supply chain & processing: Complexity of the chain and processing stages, risk of bypassing or mixing with products of unknown origin.

- Additional information: Conclusions of expert groups, information from certification systems or other verified systems.

Result of the risk assessment:

- No or only negligible risk: Products may be placed on the market or exported.

- Non-negligible risk: Risk mitigation measures are required prior to marketing or export.

This logic is important because it forces EUDR compliance into an operational rhythm: without clear criteria, approvals and escalation paths, the assessment becomes a case-by-case discussion and this is precisely what does not scale in real supply chains.

If the risk is not negligible, a guideline is not enough. Specific, documented measures are then required. Typical steps are

- Request for additional information, data or documents

- Independent investigations or audits

- Further measures as part of the information requirements

- Supporting suppliers with compliance

Important as a practical rule: No product may be placed on the market or exported without documented risk reduction in the event of a relevant risk. This is the point at which many programs collapse: If measures are not operationalized, the regulation quickly becomes a blocker for sales and supply.

The due diligence declaration (DDS) is the formal step that makes EUDR compliance effective: It is submitted digitally in the EU information system. After submission, the system generates a reference number. This number is not just internal proof, it is the prerequisite for importing or exporting relevant products and is passed on along the supply chain.

This is how it works in practice:

- Access & registration

First of all, registration or access to the EU information system is required. Without access, no declarations can be created or managed. - Create DDS (new or as a template)

A new due diligence declaration is created in the system. Depending on the case, you can use an existing declaration as a template or start from scratch. - Enter details and geodata

The required company and product data is then entered, including the geocoordinates of the original areas. Depending on the constellation, geodata can be entered manually or uploaded via GeoJSON. - Submit

Once all the information is complete, the DDS is submitted to the system. From this moment on, it is part of the officially verifiable documentation. - Receive, save and forward reference number

After submission, the system generates a reference number. This reference number must be saved internally and is passed on to downstream parties. For import or export, it is practically the key without which no further action can be taken.

Special case: Reference to an upstream due diligence declaration

In many supply chains, not all companies submit their own DDS. Instead, reference is made to an upstream due diligence declaration. In this case, the reference number of the upstream DDS is entered in the system, as well as the verification number. Both numbers can be called up in the system and serve as a unique link.

Practical rule: Even if you are only referencing, you are still obliged to keep the information in such a way that it is traceable during audits. It is crucial that reference numbers, batches and internal approvals fit together neatly.

Since the adjustment at the end of 2025, the clarity of roles in the supply chain is crucial. As a rule, the company that places the goods on the market in the EU for the first time submits the due diligence declaration (DDS). Downstream actors (downstream operators and traders) receive and use this declaration via DDS reference numbers or simplified declaration (SD) identifiers. Despite this simplification, the responsibility remains to ensure that your own processes run smoothly. Downstream operators cannot 'sit back completely', as they still have information obligations (especially in the case of 'substantiated concerns') and non-SMEs must also fulfill verification obligations to ensure the conformity of the products.

It is fundamentally important that all steps in the supply chain are traceable. This is the EUDR basic requirement - complete traceability.

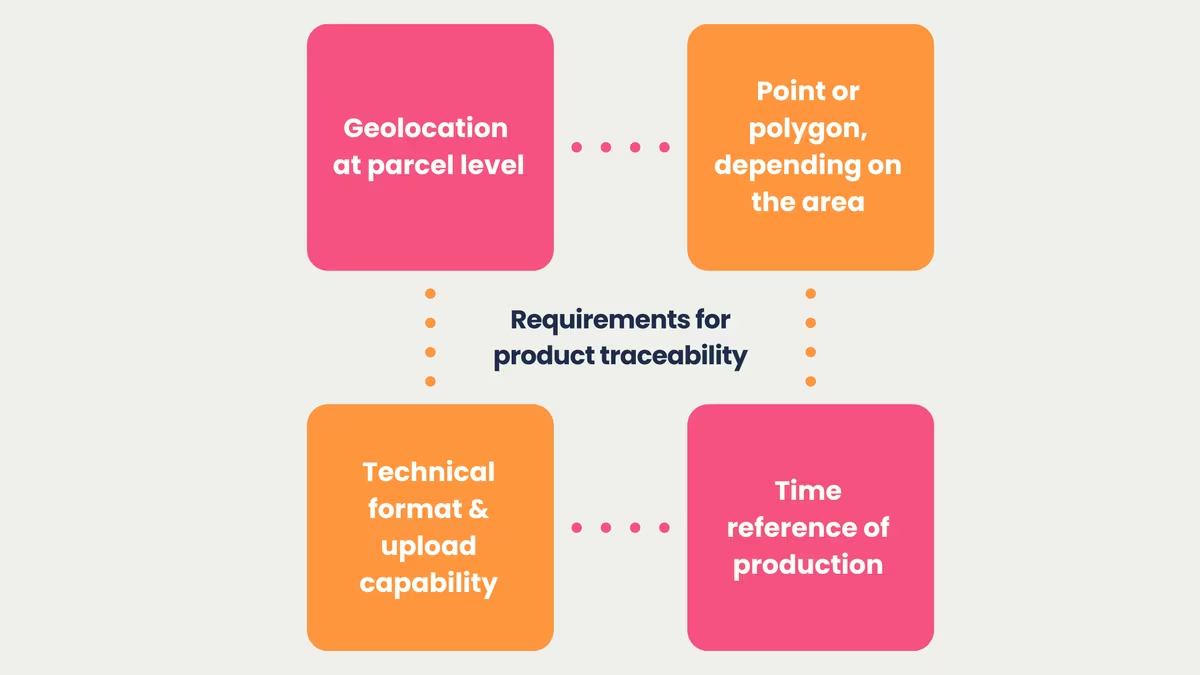

Requirements for the traceability of products

Traceability is the backbone of the Deforestation Ordinance. It is understood in much more concrete terms than traditional batch or supplier verification. It is crucial that a product can be traced back to the area on which the raw material was produced. To achieve this, companies must record the relevant information in such a way that it can be processed in the European Union's information system as part of the due diligence declaration.

What is particularly important in practice:

- Geolocation at plot level: The due diligence declaration shall indicate the geographical coordinates of the plots of land on which the raw materials were produced, with at least six decimal places for longitude and latitude. Responsibility for the accuracy of the data lies with the operator, even if it was provided by the supplier.

- Point or polygon, depending on the area: Polygons are mandatory for areas over 4 hectares, one point is sufficient for smaller areas. For cattle, one geo-point per holding is sufficient, but all holding locations must be recorded over the entire lifespan. Micro and small producers (MSPOs) from low-risk countries may be allowed to enter the postal address instead of the geo-coordinates.

- Technical format & upload capability: Geodata must be provided exclusively in GeoJSON format (WGS-84 / EPSG-4326). Manual input is hardly realistic for many areas, which is why the system supports file uploads.

- Temporal reference of production: In addition to the "where", the "when" is also relevant. For most raw materials, the harvest date or production period applies; for cattle, the entire lifespan from birth to slaughter. Animals born before June 29, 2023 are generally not covered by the EUDR.

In short: traceability is not just about knowing our suppliers, but a combination of area reference, data structure (geo-data) and system-compatible documentation. Geodata in the EUDR - that is what is required.

Checking supply chains for deforestation risks

The regulation does not require a guarantee of "zero risk". However, it does require companies to assess and manage risks in such a way that ultimately only goods are traded where the risk is negligible or has been reduced accordingly through measures. Negligible means that after a complete assessment of all information, there is no cause for concern with regard to freedom from deforestation or legality. EU instruments such as country benchmarking help, but are no substitute for a country's own risk assessment. Important: Countries that are not explicitly listed as low or high risk are automatically considered standard risk. Even when sourcing from low-risk countries, the collection of information remains mandatory; only the comprehensive risk assessment and mitigation can be omitted if there are no indications of a risk.

What the risk assessment typically boils down to:

- Structured assessment of risk drivers: country/regional risk (benchmarking), complexity of the supply chain, known hotspots, governance/legal enforcement, and plausibility of supplier data and area data.

- Think deforestation assessment in terms of area: In practice, much boils down to an area check, i.e. the question of whether and when forest loss/deforestation has taken place on the specified area. This is often supported by satellite/monitoring data and plausibility checks.

- Risk mitigation as "tangible" measures: If risks are not negligible, concrete steps such as additional evidence, tighter supplier requirements, independent audits, monitoring, segmentation of goods flows or, if necessary, the realignment of sourcing decisions are required.

Since the adjustment at the end of 2025, the following has applied in practice: the declaration of due diligence (DDS) is usually submitted by the first distributor, with downstream actors then working primarily with reference numbers. This saves duplication of work, but the checks beforehand still have to be carried out properly. If the risk assessment is sloppy, the DDS quickly becomes a problem instead of a safeguard. In the event of substantiated concerns, non-SMEs must also actively check whether due diligence has been properly exercised - until then, the goods concerned are subject to a distribution ban. Here we have put together a guide for you on how to implement the EU deforestation regulation step by step.

EUDR in the customs process: What must be included in the declaration?

In practice, compliance is not only decided in the audit folder, but often very specifically at customs: certain information must be provided in the customs declaration for the import or export of EUDR-relevant goods, otherwise the goods will not be released. Important: The DDS (or, if applicable, the SD) must be submitted in the EU information system before the customs declaration is submitted and the reference number must have been received.

Mandatory information for import & export

The following information is always required in the customs declaration for relevant goods:

- Customs tariff number (incl. TARIC): the 10-digit EU customs tariff number based on the HS/KN system and supplemented by TARIC.

- Quantity: in kilograms net weight (the weight of the product without packaging), plus additional unit if applicable.

- Document coding (TARIC document code): a code that signals to customs that the EUDR requirement has been met. Typical example: C716 ("Due diligence declaration available, goods may be placed on the market, imported or exported").

- Document number = due diligence declaration (DDS) reference number: The reference number from the EU information system must be entered as the document number. Several DDS reference numbers can also be combined in one customs declaration.

- Y-codes (exemptions), if applicable: In certain cases, additional Y-codes are used to correctly reflect exemptions/reliefs in the notification (e.g. SME constellations, transitional periods, "ex" HS codes from Annex I or products made from recycled material).

Important: The goods will only be released if the coding is complete (incl. reference number). If something is missing, the import/export cannot be processed in case of doubt.

Special cases that are often overlooked in practice

- Re-import: A conventional reference number (99EU999999999999) can be used instead of a separate DDS for products that were demonstrably previously placed on the EU market and exported.

- Export by downstream operator: When exporting, it is generally not necessary to specify a separate DDS reference number; instead, a dedicated TARIC certificate code is sufficient.

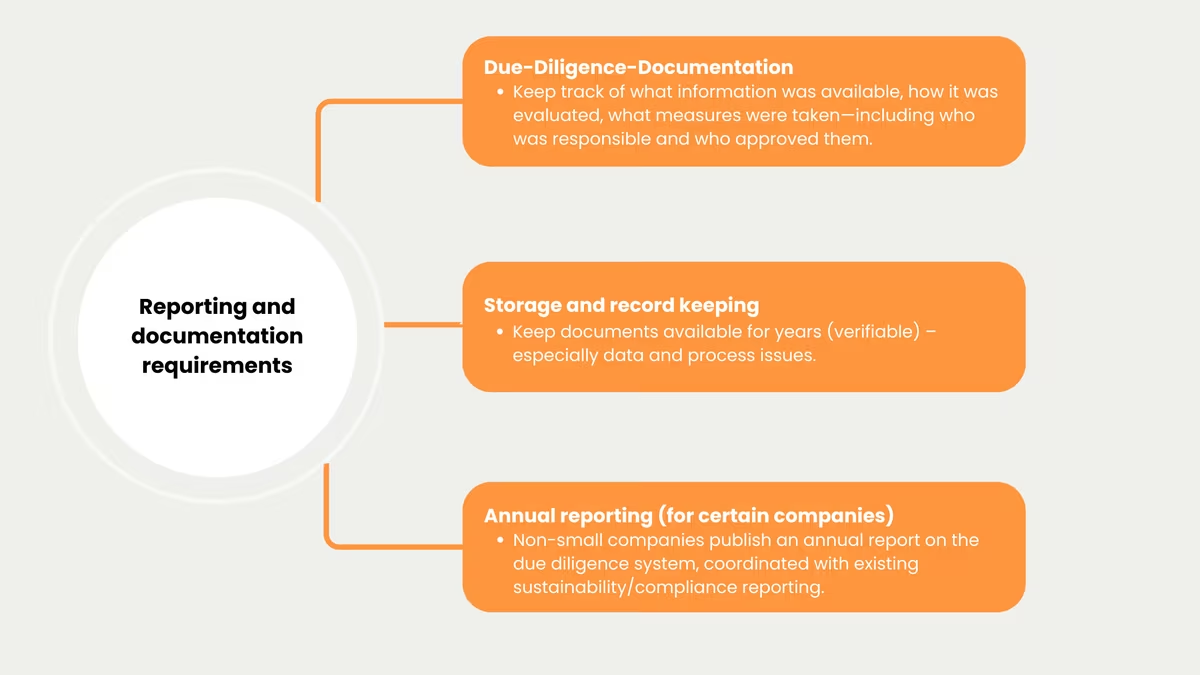

Reporting and documentation obligations

EUDR compliance does not work without proper documentation. Companies must be able to show how they arrived at their decisions. This requires two things: firstly, evidence that really stands up to scrutiny, and secondly, a reliable process that creates and updates these documents on an ongoing basis and makes them easy to find.

Three levels are central to this:

- Documentation of due diligence: Companies must be able to prove what information was available, how risks were assessed and what measures, if any, were implemented, including the respective responsible parties and approvals. The due diligence system must also be reviewed at least once a year and updated if necessary.

- Retention and verification: All documents, due diligence declarations, risk assessments, supplier data and reference numbers, if applicable, must be available for at least five years from the time the products are placed on the market or exported. Downstream operators and traders are also obliged to do so, but without specifying a particular storage system: it is sufficient if the data can be compiled within a reasonable period of time at the request of the authorities.

- Annual public reporting (for non-SMEs): Non-SME operators must publicly report on their due diligence system annually. The first report is due after December 30, 2027 and covers the year 2027. Those already reporting under CSRD or CSDDD can integrate the EUDR-relevant information there to avoid duplication, which should be planned into governance and reporting structures at an early stage.

In practice, it is helpful to treat documentation obligations not as a filing problem, but as a design issue:

- What minimum proof must be provided for each product flow?

- Where are they stored in the system?

- How do you prevent different teams from working with different versions?

- And how can it be shown at the touch of a button that a process has been released in compliance with EUDR?

For many companies, the EU information system becomes the linchpin here, because due diligence statements are created and managed there, including references that are used further down the chain.

Cooperation with suppliers to comply with the EUDR

No company fulfills the deforestation ordinance on its own. The crucial information almost always originates within the company's own organization. This is precisely why cooperation with suppliers is becoming an important success factor: not as a communication measure, but as a structured, contractually and procedurally secured data exchange. And yes: in many supply chains, these are de facto dependencies, without data there is no trade.

Three-stage approach to cooperation with suppliers

- Which data is mandatory (incl. geodata format, references, proofs)?

- Which quality criteria apply (completeness, plausibility, up-to-dateness)?

- What deadlines and escalation logic apply if data is missing?

Smaller suppliers in particular often fail not because of a lack of will, but because of technology and processes. If you support them with training, simple templates, suitable tools and clear contact persons, things will run much more smoothly and the purchasing department will not suddenly find itself without data shortly before the end.

- EUDR clauses (data obligations, audit/inspection rights, obligations to cooperate)

- Mechanisms for correction/remedy when risks occur

- Consequences of repeated inability to deliver (up to and including sourcing decisions)

Since the simplifications, it is even more important that cooperation in the supply chain is properly organized. If the DDS lies with the first distributor and others work primarily with references, the supplier data really must be correct. This is the only way to ensure that reference numbers, batches and internal approvals match and nothing gets lost along the way. Attention should be paid to this with batches, deliveries and the DDS.

Many underestimate that the deforestation regulation not only affects legal and purchasing, but also data and systems. The EU information system is the central working platform for due diligence declarations and references. If you define clear responsibilities early on and structure the data properly (for uploads such as GeoJSON, for example), you will save a lot of effort later on and make far fewer mistakes.

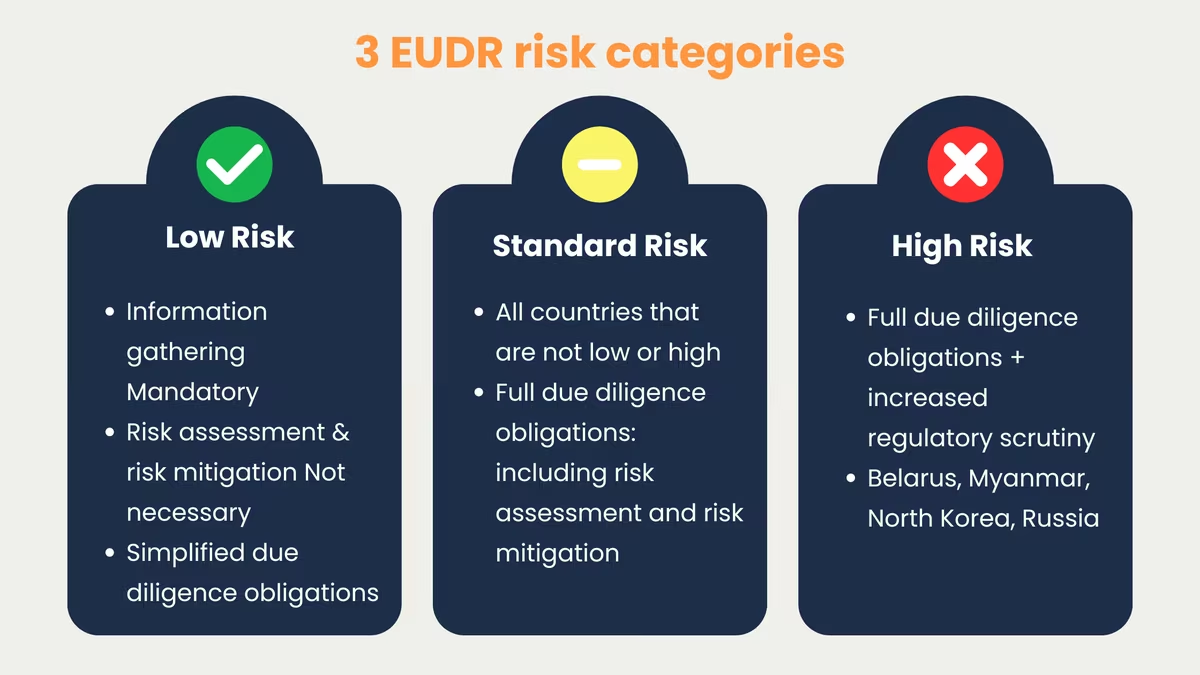

Country benchmarking

With country benchmarking, the EU has created a central instrument to systematically classify the deforestation risk per country of origin. Since May 22, 2025, an official classification has been available for the first time, which divides countries into three categories: low risk, standard risk and high risk. Benchmarking is therefore a decisive lever for the question of how deep due diligence must go - and where companies can work with simplified requirements.

The logic of the classification is important here: the EU publishes explicit lists for low risk and high risk. All countries that are not explicitly on these lists are automatically classified as standard risk. This makes "standard" the basic category - and the risk classification determines how extensive risk analysis and risk mitigation must be in practice. This applies to country benchmarking in detail.

Risk categories at a glance

Low risk: Countries in this category are considered to be at comparatively low risk of deforestation-related violations. Companies in this category benefit from simplified due diligence obligations: Information collection remains mandatory, a comprehensive risk assessment and risk mitigation is generally not required. Typical examples (excerpt) include

- Many EU member states (classified as low risk) and the USA

- as well as individual countries that often seem surprising but are explicitly listed as low risk (e.g. Laos or the Dominican Republic)

Standard risk: This category is the "default" classification: It applies to all countries that are not explicitly listed as low or high. For imports from standard risk countries, the full due diligence obligations of the EUDR Regulation continue to apply, including risk assessment and, if necessary, risk mitigation measures.

High risk: Countries in this category are subject to particularly strict expectations, not only because of the full due diligence requirements, but also because they are accompanied by a higher level of regulatory scrutiny. In the first official classification, only four countries were listed as high risk:

- Belarus

- Myanmar

- North Korea

- Russia

EUDR-relevant products and raw materials

List of raw materials concerned (e.g. wood, soy, palm oil)

For the EUDR (Regulation EU 2023/1115), the most important thing is how the raw material is legally classified. The decisive factor is whether it belongs to the relevant raw materials and whether the specific product is listed in Annex I. The goods concerned are defined there via CN/customs tariff codes, in some cases only for certain subgroups ("ex" codes). This applies to HS codes and TARIC codes under the Deforestation Regulation.

The Deforestation Ordinance is linked to seven raw materials:

- Wood

- Soy

- Palm oil

- Beef

- Cocoa

- Coffee

- Rubber (natural rubber)

Important in practice: As soon as a product contains one of these raw materials, was fed with it or was manufactured from it, it is worth taking a look at Annex I. Only if the product category is explicitly listed there does it fall within the scope. Composite products are also affected - this applies to composite products.

Product groups and their specific requirements

The regulation does not work with sectors, but with product groups via customs tariff codes. This may seem cumbersome at first glance, but it provides clarity: one and the same material can be in scope or out of scope depending on its classification, which is precisely why correct tariff classification (CN code) is a key step in any EUDR analysis. Two points are particularly important here:

- "ex" codes: If "ex" appears before a code in Annex I, only an excerpt of the product group is covered. For example, "ex 9401" only covers wooden seats, but not seats made of other materials.

- No quantity or value threshold: Even the smallest quantities of relevant products are subject to the obligations.

Typical product groups that fall under Annex I (depending on the CN code) are e.g:

→ Wood & wood products: Logs, sawn timber, panel materials, furniture, certain paper/cardboard products

→ Soy: beans, soybean meal/flour, soybean oil (depending on classification)

→ Palm oil: palm oil and certain palm oil-based products

→ Cattle: cattle farming/products incl. certain leather/skin product groups (hides, skins and leather are to be excluded from the scope according to the May 2026 draft)

→ Cocoa & coffee: Raw materials and selected processed product forms (e.g. certain cocoa products, coffee products). According to the May 2026 draft, soluble coffee is also to be included.

→ Rubber: Natural rubber and selected products made from it (e.g. certain tire/rubber products). This applies to natural and synthetic rubber.

What has changed recently: In the course of the targeted revision, Annex I was technically adapted, among other things by removing certain printed products from the scope (Annex I adjustment "ex 49").

Exceptions and special regulations

In addition to the principle of Annex I decisions, there are a number of special cases in the EU Deforestation Regulation and the accompanying Guidance/FAQ that are regularly overlooked in projects.

Important exceptions and delimitations include:

- Purely recycled products (100% recycled): Products that consist entirely of recycled material are generally not subject to EUDR. However, as soon as virgin material is mixed in (e.g. new wood to repair a pallet or virgin pulp in paper), the regulation applies to these proportions.

- Waste, used or second-hand products: Products that have completed their life cycle and would otherwise be disposed of as waste are exempt, as are their components. This also applies, for example, to the used tire carcass of retreaded tires; only the new rubber tread remains subject to EUDR.

- Packaging if it only "runs along": Packaging materials or containers that only serve a transportation or protective function are out of scope, including reusable packaging such as pallet pools or reusable containers. The situation is different when packaging is traded as an independent product.

- Printed products (HS 49): Since the revision at the end of 2025, many printed products have been excluded from the scope of application. This also includes marketing and information material (e.g. operating instructions, flyers, catalogs) that is attached to another product or provided free of charge. However, if such material is sold independently, the regulation still applies.

- Samples or specimens for testing or analysis purposes: Product samples of negligible value and in negligible quantity that are used solely to initiate new supplier relationships or for testing/analysis purposes are excluded, especially if they are consumed or destroyed during the test.

In practice, these special cases often lead to misclassifications. Here are the most important distinctions.

Some special features apply to wood and wood products under the EU Deforestation Regulation.

Special features of wood & wood products

When it comes to implementing wood, companies frequently encounter three recurring bottlenecks:

- Traceability: The more trading and processing steps, the more often there is a lack of consistent data back to the area of origin - especially in the case of geodata.

- Mixing / mass balancing: Raw materials from different sources are mixed in sawmills, pellet mills or paper mills. It is then often no longer possible to clearly assign them to individual areas. For mixed products, however, all components must be EUDR-compliant.

- Area origin: Forest areas often consist of many parcels, small owners or communal management. Determining the exact origin of individual wood lots is therefore challenging, especially outside the EU.

A frequent stumbling block: The transitional regulation between the EUTR and EUDR plays a major role for wood. For timber and timber products that were produced before June 29, 2023 and are placed on the market from December 30, 2025, the EUTR continues to apply up to and including December 31, 2028. Only after this date does the Deforestation Regulation apply exclusively. The date of production and time of placing on the market are therefore decisive.

It is important to note that these wood transitional rules run independently of the general EUDR deadlines according to company size; wood is a special case here.

FLEGT also causes misunderstandings in practice. The FLEGT regulations remain in force and are intended to ensure that only legally harvested timber from partner countries enters the EU. A FLEGT license therefore confirms legality - but it does not replace the EUDR requirements for freedom from deforestation and due diligence (incl. DDS).

Note: FLEGT can help with "legal", the Deforestation Ordinance also requires "deforestation-free" and "DDS/verifiable due diligence".

Affected companies & timetable

Scope of application according to company size and activity

Whether a company is subject to the EU Deforestation Regulation depends less on the industry and more on its role in the flow of goods. The regulation makes a rough distinction between "operators" and "traders". Since the amendment at the end of 2025, an additional distinction has been made between initial distributors, traders and downstream market participants:

- First distributor / exporter (Operatro): Anyone who makes a relevant product available on the EU market for the first time or exports it from the EU typically falls into the operator role. Examples: an importer of cocoa beans, a cattle farmer in the EU. Operators have a full due diligence obligation and must submit a DDS.

- Trader: Anyone who resells a relevant product after it has already been placed in the EU is considered a trader. No own DDS obligation, but information and retention obligations to suppliers and customers.

- Downstream operator (new): Companies placing on the market or exporting relevant products already covered by a DDS or simplified declaration, typically after processing with HS code change. Example: a chocolate manufacturer that produces chocolate from imported cocoa beans. Obligations essentially the same as for traders: no DDS levy, but information and retention obligations (obligation to register in the EU information system for non-SMEs).

Whether own import, own consumption or intermediate trader - our article Own consumption, own import, intermediate solution - When does the EUDR apply and when does it not?

These are the due diligence obligations for market participants and traders in detail.

Two special cases that often occur in practice:

- Non-EU operator (Art. 7 EUDR): If a company based outside the EU places relevant products on the EU market, the first company based in the EU that passes on the goods is also deemed to be an operator. There are therefore two operators with full obligations.

- Dual-role operator + downstream operator: A legal entity can have both roles at the same time, e.g. if it imports raw timber (operator) and processes it into sawn timber itself and sells it (downstream operator). In this case, DDS reference numbers do not have to be passed on within the same legal entity.

A separate sub-category of operators is the Micro or Small Primary Operator (MSPO), micro and small producers from low-risk countries with significantly simplified obligations. Details can be found in the update section above.

Transition periods and timetable for implementation

One point in particular is crucial for the timetable today: although the regulation has been in force since 2023, it will only become mandatory from the application deadlines. Following the amendments in December 2024 and December 2025 and the EUDR postponement, the current timetable (as of February 2026) is as follows

- Large and medium-sized companies (large/medium operators): from December 30, 2026

- Micro and small enterprises (micro/small operators): from June 30, 2027

- Special rule for "EUTR products": For market participants who were established as such on 31.12.2024, the later start date of 30.06.2027 generally applies - except for products that fall under the Annex to Regulation (EU) No. 995/2010 (EUTR). Here the application already applies from 30.12.2026.

EUDR and the cut-off date: Find out how to deal with goods in stock and later placing on the market here.

What the deadlines mean in practical terms: The additional time is not a break. It is an opportunity to set up the issue properly, as role clarification (operator/trader/downstream), data flows and internal approvals usually take longer in practice than the pure legal review. The amending regulation also regulates EUTR continued application until 31.12.2029 for certain "old goods" wood or wood products (produced before 29.06.2023, placed on the market from 30.12.2026).

Differences between large companies and SMEs

The regulation deliberately differentiates between company size and role. Large and medium-sized companies usually have to fulfill more formal obligations. SMEs are relieved in some cases. This applies in particular where the rules are intended to prevent the same work being done more than once in the supply chain. These thresholds apply in detail to corporations and SMEs.

This is typically more significant for large and medium-sized companies:

- More formal governance and more transparency: For non-SMEs, this includes annual public reporting on the due diligence system, with the first report due after December 30, 2027. In addition, the system must be reviewed at least once a year. Non-SME downstream operators and traders are also required to register in the EU information system.

- Greater expectation of systematics and scalability: Large organizations must set up due diligence in such a way that it functions consistently across product groups, countries and business units, including audit capability.

Where SMEs are typically relieved:

- Extended transition period: For micro and small enterprises, the EUDR will only apply from June 30, 2027, half a year later than for non-SMEs.

- Less reporting burden: SMEs do not always have the same public reporting obligations as non-SMEs.

- Simplifications along the chain: The obligation to submit the DDS lies in principle with the first distributor. The idea of the first downstream is particularly relevant: Only the first downstream entity has to record reference numbers in a structured way and it has to do so passively: it does not have to actively ask for the reference number, but only record it if it is passed on by the operator.

- Special category MSPO: Micro and small producers from low-risk countries who produce their own products and place them directly on the EU market benefit from particularly far-reaching facilitations, details in the update section above.

Where SMEs still come under pressure

Fewer formal obligations do not mean less effort. Small companies quickly reach their limits in practice: Geolocation data from suppliers from third countries is difficult to obtain, internal resources for risk analyses are often lacking and an in-house compliance structure is rarely in place. In addition, SMEs are also coming under increasing pressure from larger customers to provide EUDR-compliant evidence - regardless of what the regulation formally requires of them.

What SMEs can do now

- Check the supply chain: Which of the seven EUDR raw materials are included in your own product range, either directly or as a component of processed products?

- Approach suppliers: Clarify at an early stage which geodata and certificates of origin suppliers can provide.

- Clarify my role in the chain: Am I the first distributor or a downstream player? The specific obligations that apply depend on this.

A point that is often overlooked in practice: Despite simplifications, SMEs also need clean processes. If information is missing or not properly documented internally, things quickly become difficult, for example with customer requirements, inspections or in supply chains with many intermediate stages.

Monitoring compliance with the EUDR

Competent authorities and monitoring mechanisms

The EU relies on the member states to enforce the EUDR. Each state appoints its own authorities to monitor the rules and enforce them on a day-to-day basis. Control is therefore not carried out centrally from Brussels, but locally, ideally with uniform standards and closely interlinked with customs and market surveillance.

The checks are risk-based. Depending on the risk category of the country of origin, authorities must carry out a minimum number of checks: at least 1% for low risk, 3% for standard risk and 9% for high risk. For companies, this means that the chance of an inspection depends heavily on the origin of the raw materials or product. Therefore, data, evidence and internal decisions must be fully and comprehensibly documented at all times.

Carrying out inspections and audits

Controls are more than just paperwork. Authorities check whether the information is comprehensible and whether the internal assessments are really conclusive. They also check whether the processes in the company are set up in such a way that the rules are actually adhered to in the end. This can happen on an ad hoc basis, for example in the event of indications or anomalies, and there are also regular checks as part of the minimum quotas set.

In practice, an inspection usually consists of several parts. Authorities compare documents, carry out plausibility checks and look particularly closely at information on origin and geodata. There are often spot checks that are examined in greater depth. Depending on the case, on-site measures are also possible. If a risk is acute, authorities can also intervene immediately and temporarily stop the flow of goods, for example by securing goods or temporarily suspending the placing on the market or export.

Role of digital systems for monitoring

The EUDR can hardly be implemented without a digital infrastructure. This is why the EU information system plays a central role. Due diligence declarations are recorded and managed there and can be reused in the supply chain. Downstream companies can refer to existing entries by adopting the reference and verification numbers, either manually or via a CSV upload.

Technical scaling is also provided for large volumes of data: The system supports a machine connection via an API to manage declarations and data records in bulk. This makes the system a central access point for the authorities: it facilitates targeted screening, supports risk-based selection decisions and creates a uniform basis on which checks can be documented in a comprehensible and repeatable manner. There are also user guides that describe how to use the system in practice.

Sanctions and penalties for breaches of the EUDR

The regulation is deliberately harsh in its sanction logic because it uses market access as a lever. In addition to the financial dimension, the main focus is on measures that have an impact on the market: goods can be withdrawn from the market, distribution or supply bans can be imposed and, in certain constellations, confiscation or seizure is also relevant in order to stop risks immediately.

The framework for fines is also designed to be tangible. Many summaries point out that sanctions can reach up to 4% of (EU-wide) annual turnover. The decisive factor here is not so much the percentage as the message: infringements should not be calculable, but represent a real compliance risk, both financially and operationally.

Enforcement is the responsibility of the competent authorities in the Member States. They can not only impose penalties, but also order immediate measures to rectify problems. This may include recalling products or withdrawing them from the market. If a risk is acute, they can also initiate provisional steps to prevent damage.

In addition, there is an element that is often underestimated in practice: public visibility. Under the "naming and shaming" concept, the specialist literature on the EUDR emphasizes that legally binding decisions can be published, which adds a communicative and reputational level to sanctions.

The risk of reputational damage is not a marginal issue in the EU Deforestation Directive. When procedures or decisions become public, pressure quickly arises from many sides. Not only from authorities, but also from customers, investors, NGOs and the media. Violations are often immediately interpreted as a sign that controls are lacking, data is incorrect or suppliers are not being managed well enough. This can happen even if it is "only" an internal process or a system that has not worked properly at one point.

In addition to fines and sales bans, there may be other consequences. Business relationships can quickly become shaky because customers do not want to take risks. Contractual penalties or reversals become more likely, and internal questions arise about management and organizational responsibilities. EUDR violations are therefore rarely just a legal problem. They can very quickly develop into a real business risk that runs through the entire value chain.

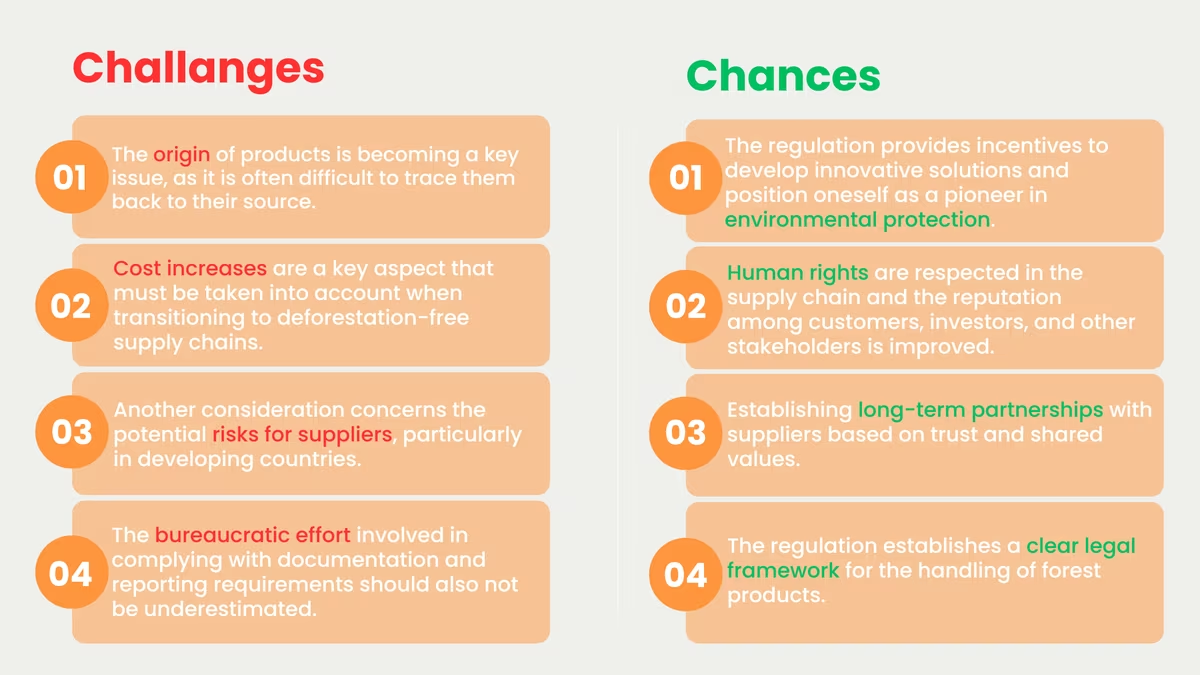

Challenges & opportunities

Effects on importers and exporters

For importers and exporters, the EUDR is primarily changing trade. Trade is increasingly becoming a question of data capability and process stability. Anyone moving flows of goods into or out of the EU must adjust to the fact that deliverability no longer just means price, quality and availability, but also reliable evidence along the flow of goods. This has a direct impact on contract design, supplier portfolios, procurement strategies and logistics, especially where supply chains have previously worked with intermediaries, mixed flows or incomplete documentation.

In practice, risk management is also shifting as a result. Goods from complex regions of origin are more frequently only procured if data, geo-information and proof of legality are available in sufficient quality. At the same time, there is increasing pressure to standardize information flows in such a way that they also work with large volumes (keyword: digital interfaces, structured data uploads and consistent references).

The trade policy dimension should also not be underestimated. Several trading partners have criticized the Deforestation Directive in international forums as a potential barrier to trade. Although this debate does not automatically lead to a weakening of the requirements, it is an indication that EUDR compliance will be a permanent factor in trade relations, negotiations and market access discussions in the future.

Challenges for developing countries

For many supplier countries, it is not so much the aim of the EUDR regulation that is the problem, but its implementation in everyday life. Especially where millions of small farmers produce in small-scale structures, there is often a lack of resources and infrastructure. Collecting geodata, documenting digitally, registering farms and maintaining data on an ongoing basis costs time and money. Small cooperatives, local exporters and individual producers are often unable to do this without support. This concern is particularly evident in countries such as Côte d'Ivoire. Smaller cocoa companies there say that the costs and organizational effort can quickly threaten their existence, while large corporations usually find it easier to cope with such requirements.

Indonesia also repeatedly points out that small farmers in particular can quickly fall out of EU supply chains without digital infrastructure or reliable internet. Not because they automatically produce less, but because they are often unable to provide the required proof in the short term.

This creates a risk that comes up again and again in the discussion. If implementation is not designed to be inclusive, large, data-rich companies in particular could end up benefiting, while smaller providers are forced out of the market. This is why support for producer countries is so important. Technical assistance, funding and practical support are needed to ensure that the EUDR really works in international trade.

Opportunities for sustainable trade practices

As demanding as the requirements are: The EUDR also opens up a new opportunity for international trade, namely competition based on verifiable sustainability. Where intransparency can still create a price advantage today, in the long term this will shift towards supply chains that can demonstrate data quality, legality and stable partnerships. This is exactly the kind of level playing field that makes sustainable practices more economically attractive, especially in industries where deforestation risks have been difficult to quantify.

In addition, the EU is increasingly supporting implementation through cooperation and support formats. One example is the "Team Europe Initiative" on deforestation-free value chains, which is supported by the European Commission and aims to strengthen partnerships with producer countries and facilitate the transition to deforestation-free supply chains. Such programs are a signal that the EUDR is not only understood as a control instrument, but also as an impetus for investment, capacity building and more resilient supply relationships.

And finally, the directive has an impact beyond the EU. It sets a standard to which other markets, buyers and financing logics can orient themselves. In the medium term, this could mean that deforestation-free and legal supply chains are not just "EU compliance", but a global reference point - with positive effects for companies that make structured investments early on and for producer regions that can demonstrably scale sustainable production.

Conclusion

The EUDR marks a significant step towards greater sustainability and environmental protection and at the same time presents companies with specific requirements. Anyone placing relevant products on the EU market must check and adapt supply chains, ensure transparency and fully document the origin of raw materials. The regulation thus makes it clear that deforestation-free production is not an add-on, but an integral part of day-to-day business.

The targeted use of modern technologies plays a decisive role in this. Digital tools and a reliable database enable companies to make processes more efficient, identify risks at an early stage and systematically meet compliance requirements.

Even if the EUDR postponement gives companies more time to prepare, it should not be seen as a delay, but as an opportunity. Those who consistently implement the regulation not only fulfill their legal obligations, but also position themselves as a reliable partner in sustainable supply chains in the long term. This is not only a contribution to the protection of forests, but also a real competitive advantage.

Frequently asked questions

The EU Deforestation Regulation(EUDR) is a European Union regulation designed to prevent products related to deforestation or forest degradation from entering the EU market. Seven raw materials are affected - cattle, cocoa, coffee, palm oil, soy, wood and rubber - as well as products made from them, such as leather, chocolate, furniture and paper.

The EUDR marks a significant step towards greater sustainability and environmental protection, while at the same time imposing specific requirements on companies. Anyone placing relevant products on the market in the EU must check and adapt supply chains, ensure transparency and fully document the origin of raw materials. The regulation thus makes it clear: freedom from deforestation is not an add-on, but an integral part of day-to-day business.

The Deforestation Regulation replaces the EU Timber Regulation(EUTR EU 995/2010). The EUTR banned the import of illegally produced timber into the EU for the first time in 2010 and obliged importers to provide evidence of legally harvested timber. An important step towards reducing the risk of illegal timber imports.

However, it remains valid for three years for timber products that originate from trees felled before the deforestation regulation came into force and enter the EU market during the transition period between EUDR and EUTR (Article 37(2)).

The transitional period extends from the adoption of the regulation on June 30, 2023 until the date of application on December 30, 2026 (for micro and small enterprises until June 30, 2027). This will be relevant for raw materials and products in accordance with EUDR Annex 1 that were imported during this phase but are only placed on the market in processed form after the date of application.

Example: Cocoa - listed as a relevant raw material in EUDR Annex 1 via its HS code - was imported during the transition phase without geolocation data. The chocolate made from it, which is also listed in Annex 1 of the EUDR, is to be sold from December 30, 2026. In this case, the market participant must be able to prove that the raw material was on the market before the regulation came into force, for example by providing appropriate evidence. If, on the other hand, the raw material is only placed on the market or exported after December 30, 2026, the standard obligations of the EUDR apply.

All "market participants" are affected, i.e. natural or legal persons who place relevant products on the EU market or export them as part of a commercial activity. This includes processing, distribution and use. The following applies: as soon as a company introduces relevant products into the supply chain, whether as an importer, processor or trader, it falls under the regulation. An example: Company A imports cocoa butter, company B processes it into chocolate, both are considered market participants.

The scope of the obligations depends on the size of the company. Large and medium-sized companies must fulfill the full due diligence obligation, including risk analysis and mitigation measures. SMEs are partially exempt, but they must ensure that their goods have been produced in a deforestation-free and legally compliant manner and keep reference numbers of the due diligence declaration for five years.

Small companies are those with total assets of up to EUR 4 million, net sales of up to EUR 8 million and a maximum of 50 employees. Medium-sized companies have a balance sheet total of up to EUR 20 million, a net turnover of up to EUR 40 million and a maximum of 250 employees. Regardless of size, however, it is the responsibility of each company to comply with the due diligence obligations.

Article 7 EUDR describes this case in more detail. In this respect, it should be noted that the first natural or legal person established in the Union to make these relevant products available on the market is considered to be an operator within the meaning of this Regulation. This means that the first company established in the EU that places the products on the market must comply with the due diligence obligations.

The EU Deforestation Regulation covers seven raw materials: Wood, coffee, soy, palm oil, cocoa, cattle and rubber as well as all products made from them as listed in Annex I. The list is exhaustive, no thresholds apply and the requirements apply regardless of whether the products were produced in the EU or outside. However, the Commission may amend the list by delegated act. An initial review is planned within two years of the regulation coming into force. The full text of the Regulation is available for download as an EUDR Regulation PDF from EUR-Lex and, in addition to the due diligence obligations, also contains Annex I with the binding list of all raw materials and products concerned, including HS codes. For companies, we recommend the consolidated version as an EUDR Regulation PDF, as this already contains all the amendments - including the postponement of the deadline by Regulation (EU) 2025/2650.

According to Article 3 EUDR, the raw materials and products must fulfill the following conditions cumulatively:

- They must not be deforested and must comply with the deadline of December 31, 2020.

- In addition, the products must be produced in accordance with the applicable laws of the country of manufacture.

- Finally, a declaration of due diligence is required for the corresponding products.

Deforestation refers to the conversion of forests into agricultural land, regardless of whether it is caused by humans or not. Important: The EUDR excludes not only illegal deforestation, but all forms of deforestation. Products are considered deforestation-free if the cultivated areas have not been deforested or degraded since December 31, 2020.

According to the FAO definition, an area of more than 0.5 hectares with trees over 5 m high and a canopy cover of more than 10 % is considered a forest, with the exception of areas used primarily for agricultural or urban purposes. Forest degradation occurs when structural changes are made to the forest cover, such as the conversion of primary forests into plantations.

Other wooded areas" are areas of more than 0.5 hectares that are not classified as forest but have a canopy cover of 5 to 10 % or are overgrown with shrubs, bushes and trees by more than 10 %. The EU Commission regularly examines whether the scope of protection of the regulation should be extended to such areas.

After one year, it will be examined whether "other wooded land" should be included in the scope. After two years, a review follows to determine whether other ecosystems such as peatlands and wetlands as well as additional raw materials such as maize and biofuels should be included. Five years after entry into force, the first general review will take place, focusing on the impact on producer countries, small-scale producers and indigenous peoples.

Operators must comply with the due diligence obligations set out in Article 8 before placing relevant products on the market or exporting them. Non-SME traders are subject to the same obligations as operators. Placing on the market is not permitted without prior fulfillment of this obligation.

SME market participants are exempt from carrying out their own due diligence if a due diligence declaration already exists for the products concerned. In this case, it is sufficient to submit the corresponding reference number. Important: For components that are not yet subject to due diligence, SMEs must also comply with the full due diligence obligation.

The current EUDR was fundamentally adapted at the end of 2025: On December 23, 2025, the revised version was published in the Official Journal of the EU. Mandatory application now applies to large and medium-sized companies from December 30, 2026 and to small and micro-enterprises from June 30, 2027. In terms of content, the revision introduces the so-called once-only approach: only the first distributor must submit a full due diligence declaration, while downstream market participants and distributors are significantly relieved. Printed products have also been removed from the scope. The EU Commission is examining further simplifications until April 2026. Companies should actively use the additional time to set up due diligence obligations and geodata collection in a practicable manner.

The due diligence procedure is divided into three steps that must be completed before placing on the market or exporting:

Step 1 - Information collection: Market participants and non-SME traders must record precise information on the product, quantity, supplier, country of origin and legality of production, including geo-coordinates of the cultivation areas. If the required information is missing, the product may not be placed on the market.

Step 2 - Risk assessment: A comprehensive risk assessment is mandatory for goods from standard and high-risk countries. A simplified due diligence obligation applies to low-risk countries. However, the collection of information remains mandatory. The result must show that there is no or only a negligible risk of deforestation.

Step 3 - Risk mitigation: If a non-negligible risk is identified, measures such as additional evidence, independent audits or closer supplier monitoring are required. Only then may the due diligence declaration be submitted and the product distributed.

All receipts must be kept for five years and the procedure must be reviewed at least once a year.

The country benchmarking (Article 29) categorizes countries of origin according to their deforestation risk in three levels: low, standard and high. This is based on objective and transparent criteria, including the extent of deforestation, the expansion of agricultural land and production trends for relevant raw materials. Other factors such as national laws, protection regulations for indigenous peoples and international sanctions can also be taken into account.

The risk classification has a direct impact on the scope of official controls and the requirements for risk analysis: In the case of low-risk countries, a simplified due diligence obligation applies. However, precise knowledge of the origin of the goods and the exclusion of deforestation and illegal practices remain mandatory in all cases.

The authorities of the respective member states are responsible for checking the due diligence declarations. The frequency depends on the risk of non-compliance. Different inspection rates apply depending on the risk classification of the country of origin: 9% for high-risk countries, 3% for standard-risk countries and 1% for low-risk countries.

The audits include both the submitted due diligence declarations, including risk assessment and risk mitigation, as well as spot checks and on-site inspections. Market participants and non-SME traders are obliged to support the authorities in this process, including by providing access to company premises and all relevant documentation.

In terms of the EUDR, traceability means being able to trace the entire path of a product from origin to marketing without any gaps. The core component is the geolocalization of all relevant cultivation areas: Plots of land must be recorded with latitude and longitude coordinates, and in the form of polygons for areas over four hectares.

There are no exemptions, neither for long supply chains nor for bulk goods such as soy or composite products such as wooden furniture. All properties involved must be identified and mixing with raw materials of unknown origin is not permitted. If a part of a product does not meet the requirements and cannot be separated, the entire product is considered non-compliant.

Geocoordinates can be recorded using cell phones, GNSS devices or digital GIS applications.

It should be emphasized that there are no exceptions. If a part of a relevant product does not comply with the regulations, it must be separated before being placed on the market or exported. If this cannot be done, the entire product is considered non-compliant. Proof of compliance with Article 3 is always crucial. The operator must record the geolocation of all properties involved, otherwise the product may not be placed on the market.

Article 9(1)(d) explains the requirements for geolocation. It is also important to record the time or period of production or the harvest date and the production period. This is necessary in order to verify that the product is actually deforestation-free in accordance with Article 3(a). The cut-off date of 31.12.2020 is therefore relevant.

There are special features with regard to cattle: The geolocation must include all farms where the cattle were kept, i.e. including grazing areas and slaughterhouses.

Article 31 grants natural and legal persons the right to report substantiated concerns to the competent authorities if they suspect a breach of the EUDR. The authorities are obliged to investigate such reports, listen to the market participants concerned and, if necessary, take action, including suspending trade in the products concerned. The whistleblowers will be informed of the measures taken within 30 days.

In the event of possible infringements, authorities can take interim measures, such as the seizure of products or the suspension of their placing on the market. If violations are detected, market participants are requested to take corrective action, including the recall or disposal of affected products and preventive measures to avoid future violations.

The sanctions must be effective, proportionate and dissuasive. They include fines, confiscation of products and revenue as well as trade bans. The amount of the fines depends on the economic benefit of the infringement and can reach up to 4% of annual turnover in the event of repeated infringements. Sanctioned companies are also publicly listed by the EU Commission.

Larissa Ragg

LinkedInMarketing Managerin · lawcode GmbH

Larissa Ragg verantwortet die Content-Strategie bei lawcode und erstellt Fachbeiträge zu den Themen EUDR, ESG-Compliance, HinSchG, Supply Chain und CSRD. Ihre Beiträge auf dem lawcode Blog machen komplexe regulatorische Anforderungen verständlich und liefern Unternehmen praxisnahe Orientierung.