Important facts

- What is the VSME standard?

- A voluntary EU standard for SMEs for simple and resource-saving sustainability reporting.

- Who does it apply to?

- Non-listed SMEs that wish to provide ESG data to banks, investors or customers.

- What modules are available?

- The Basic module provides 11 core ESG disclosures and the Comprehensive module, which is an extension for more ambitious companies.

- Why is it important?

- Following the increase in the CSRD thresholds, many SMEs are no longer required to report, but must continue to provide ESG data.

- Advantages for SMEs

- Simple application, access to financing, strengthening competitiveness.

- When can it be used?

- Voluntarily applicable since publication of the final draft in December 2024

Abstract

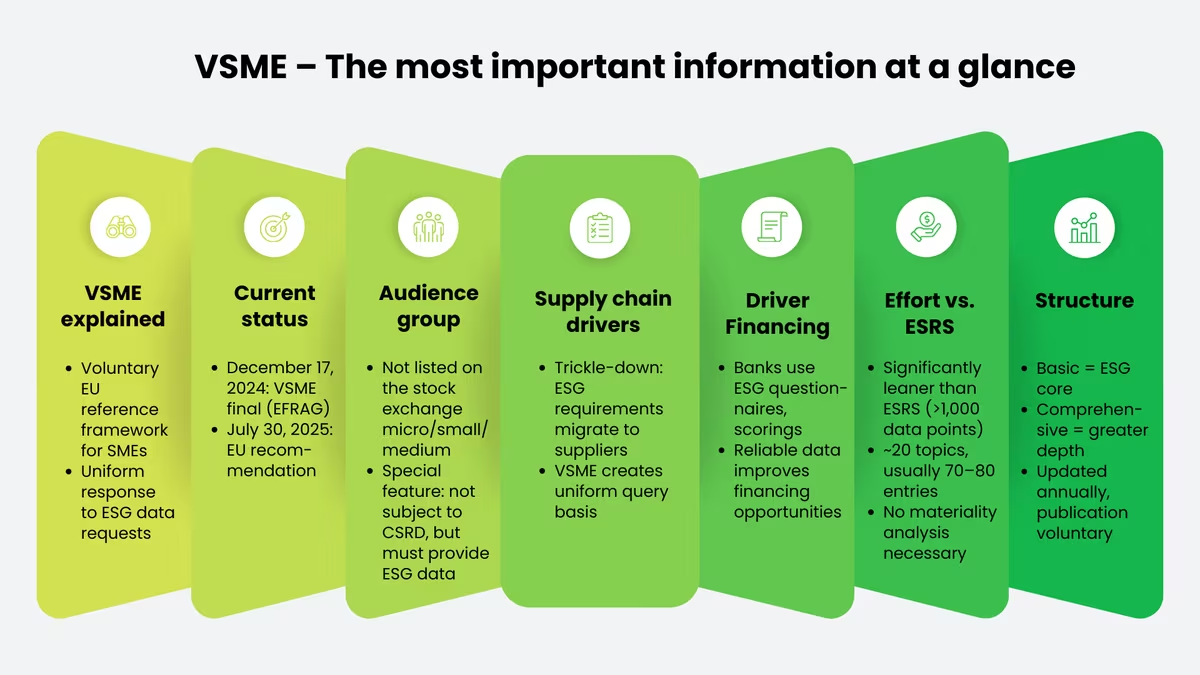

The VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs) is a voluntary EU reference framework for sustainability reporting by non-listed SMEs. EFRAG published the final standard in December 2024 and the EU Commission officially positioned it as a voluntary standard for SMEs on July 30, 2025 in Recommendation (EU) 2025/1710. The omnibus initiative to simplify EU sustainability regulation is running in parallel, and a political agreement to streamline the CSRD and CSDDD was reached at the end of 2025. However, formal implementation is still pending.

Even without a statutory reporting obligation, the VSME is relevant for many SMEs: Large companies are increasingly passing on ESG requirements to their suppliers, banks are requesting ESG data for lending decisions and a structured report protects against contradictory individual requests. The standard thus creates a uniform basis and strengthens transparency and competitive position.

The VSME is significantly leaner than the ESRS because instead of over 1,000 data points, it comprises two modules (Basic and Comprehensive) with typically 70-80 specific details. The double materiality analysis is no longer required. An annual update in line with the annual financial statements is recommended. Sensitive information may be omitted, but must be marked transparently.

Update (status: February 2026)

The VSME standard has taken a clear legal position: EFRAG submitted the final standard to the European Commission on December 17, 2024, which subsequently adopted an official recommendation (Recommendation (EU) 2025/1710) on July 30, 2025. This explicitly recognizes the VSME as a voluntary standard for SMEs, in particular as a uniform response to ESG data requests from supply chains and financial institutions.

In addition, the Omnibus Initiative (since February 2025) to simplify EU sustainability regulation is underway, a reform package that does not yet constitute applicable law. A political agreement to simplify the CSRD and CSDDD was reached at the end of 2025. Formal implementation remains the crucial next step.

VSME: Definition, background & current status

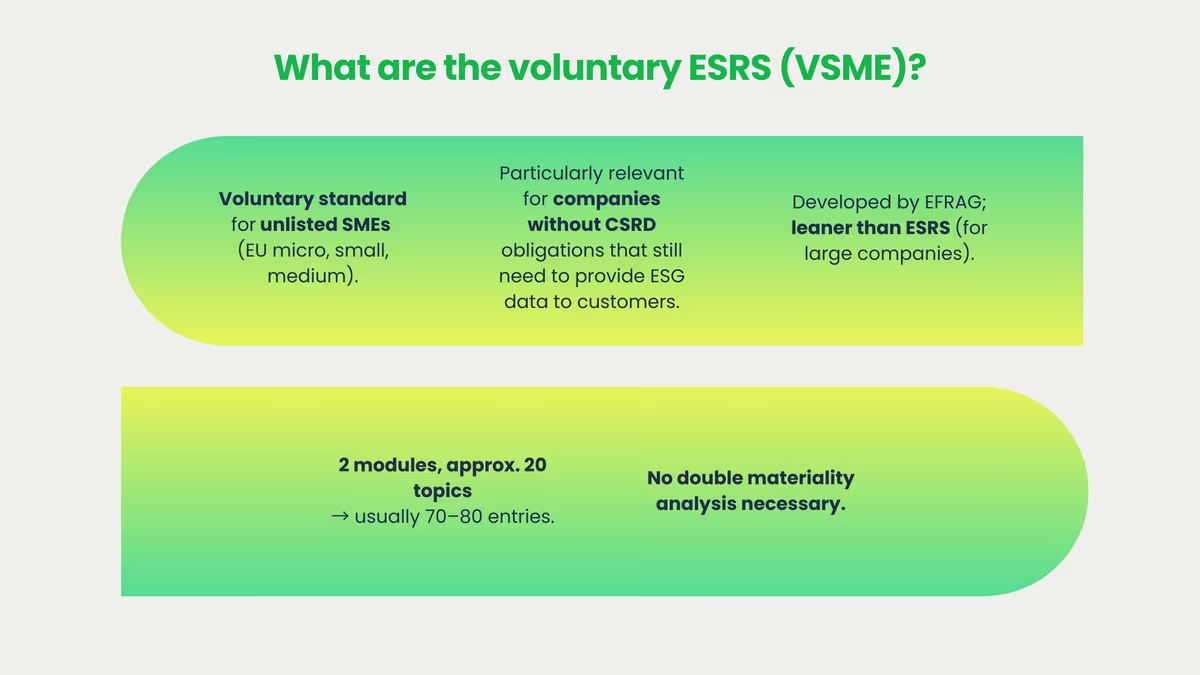

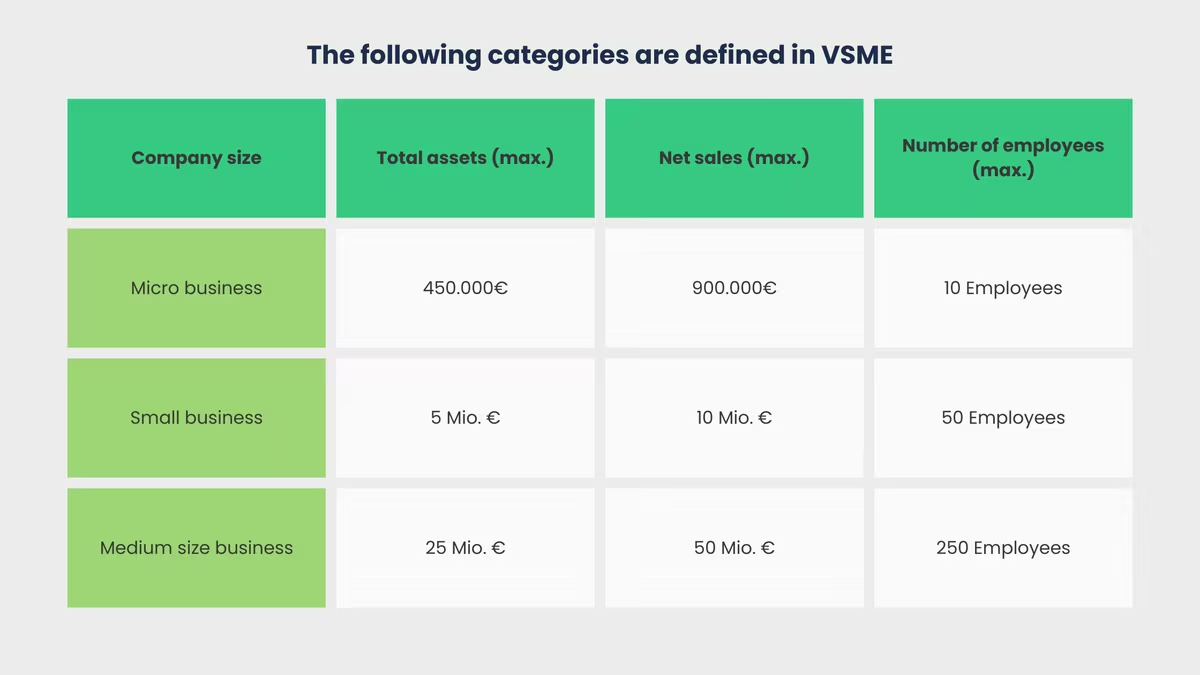

The VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs) is aimed at non-listed micro, small and medium-sized enterprises (SMEs) as defined by the EU (micro/small/medium). The threshold values of the EU Accounting Directive (including up to 250 employees and turnover and/or balance sheet total thresholds) are decisive.

In practice, the standard is particularly relevant for companies that do not fall within the scope of the CSRD but still have to regularly provide ESG data to customers or financial institutions. In the political debate, these companies are often described in simplified terms as "under 1,000 employees". ).

The VSME standards were developed by the EFRAG (European Financial Reporting Advisory Group) to support SMEs in sustainability reporting. Compared to the comprehensive ESRS, which are primarily tailored to larger companies, the VSME are much leaner and more practical. If you would like to get an overview of the "classic" reporting standards, you can find more information on this in our blog post.

By implementing these standards, SMEs can present their sustainability practices transparently. It also helps to efficiently handle ESG data requests from banks and customers, which helps to strengthen their market position and trustworthiness. It takes into account the limited resources of SMEs compared to larger corporations and thus facilitates access to financing and customers by standardizing various ESG data requests.

In contrast to the ESRS, which comprises over 1,000 data points, the VSME standard significantly reduces the administrative workload. The VSME comprises two modules with around 20 overarching reporting topics. Depending on the relevance and level of detail in practice, this results in around 70-80 specific disclosures and data points.

A double materiality analysis is not required. If you would like to find out more about the materiality analysis, you can access our article here. This simplification enables SMEs to respond more efficiently to sustainability requests from business partners such as banks or larger companies.

Current status of the VSME standards

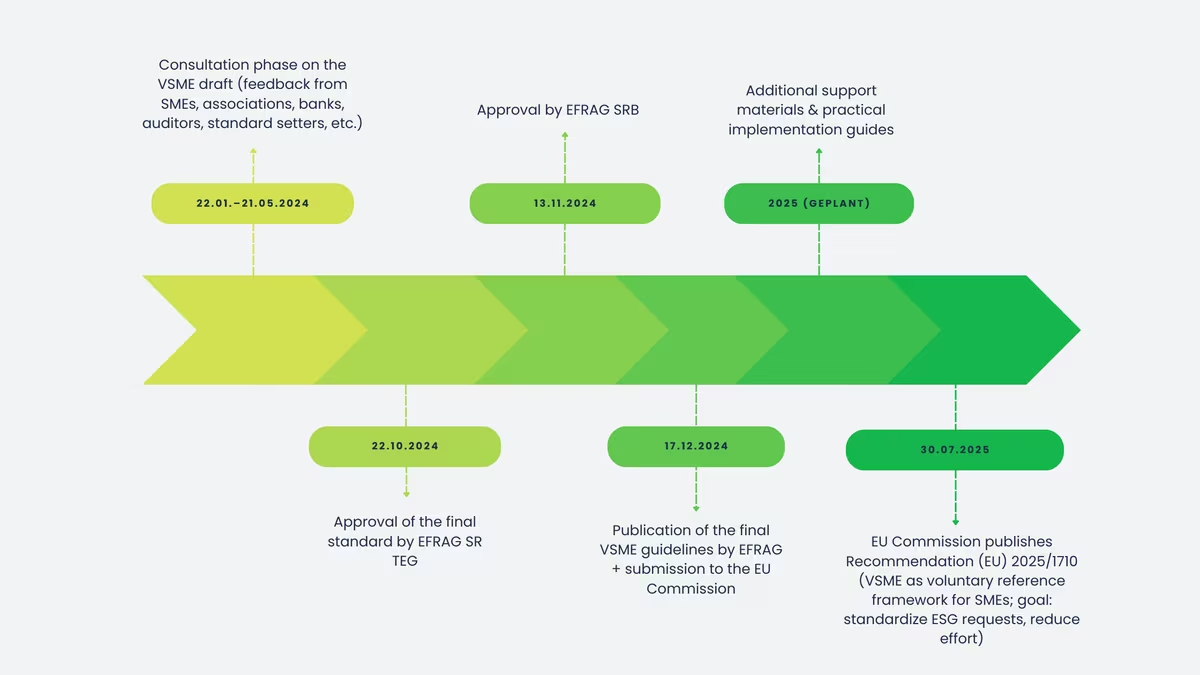

On December 17, 2024, EFRAG published the voluntary VSME guidelines for sustainability reporting by non-listed SMEs. For the first time, this provides a much clearer and practicable framework for SMEs to prepare their ESG information in a standardized manner and with less effort. This ensures greater transparency and facilitates communication with stakeholders such as customers, banks or business partners, especially if ESG data is regularly requested.

The consultation on the VSME draft ran from January 22 to May 21, 2024, during which time EFRAG collected feedback from various sources, including SMEs and their associations, banks, auditors and national standard setters. Based on this feedback, the standard was further simplified in several places in order to better adapt it to the practice and resource situation of SMEs.

The final standard was subsequently approved by the EFRAG SR TEG on October 22, 2024 and received the approval of the EFRAG SRB on November 13, 2024. Further support services are also planned for 2025, such as additional materials and practical guidelines to facilitate implementation within the company.

On this basis, the European Commission published Recommendation (EU) 2025/1710 on July 30, 2025, which explicitly supports the standard as a voluntary, practical reference framework for SMEs. The main aim is to standardize ESG information requests from supply chains and financial institutions and to significantly reduce the workload for SMEs.

Omnibus initiative: What will change for SMEs?

The EU Omnibus Initiative aims to significantly streamline the reporting obligations of the CSRD. The legislative process has been underway since February 2025. A political agreement was reached between the Commission and Parliament in December 2025. Formal implementation is still pending. In Germany, the CSRD has not yet been fully transposed into national law.

The most important planned changes at a glance:

- Narrower scope of application: In future, only companies with more than 1,000 employees and a net turnover of over € 450 million will be required to report, a reduction of around 80% of the companies affected.

- Later deadlines: reporting obligation only from 2028 (for the 2027 financial year); the stop-the-clock directive has already postponed deadlines.

- Fewer data points: Around 25% reduction, no sector-specific ESRS, more limited supply chain requirements.

- Audit: No "Reasonable Assurance". The "limited assurance" remains.

- EU taxonomy & CSDDD: Simplifications and higher thresholds, risk-based approach instead of full mapping.

This could mean that many companies will no longer be required to report in future. However, the need for clear ESG data on the part of investors, customers and banks remains. This is precisely where the VSME gains importance: it enables structured, reliable ESG reporting with manageable effort, without the full complexity of the ESRS. This makes it not only a response to current requests, but also a strategic lever for competitiveness and trust.

Never miss an update on VSME again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Companies affected

The VSME standards are aimed at unlisted micro, small and medium-sized enterprises. They are based on the size categories of the EU Accounting Directive: micro (up to 10 employees), small (up to 50) and medium (up to 250) - each combined with threshold values for turnover and total assets. The aim is to create a practical standard that SMEs can use to answer typical ESG queries from banks, customers and large companies in a uniform manner.

The standards help non-reporting companies to address the most important ESG issues, i.e. environmental, social and governance, in a structured manner without becoming unnecessarily complex. And if the EU Commission's omnibus proposal is implemented as planned, the VSME is likely to become even more relevant for many companies: as a voluntary but uniform framework for responding to ESG inquiries from customers, banks and business partners more easily.

Even if SMEs are not obliged to report, the relevance is increasing.

Relevance for small & medium-sized enterprises without a reporting obligation

An important point in ESG compliance is the so-called trickle-down effect: requirements from large companies "migrate" down the supply chain. If a company itself is subject to ESG reporting requirements, it often requests the necessary information from its suppliers. In practice, these are often small and medium-sized companies.

In many cases, these small and medium-sized enterprises do not yet have systematic procedures for collecting such data. However, the VSME standards offer these companies an effective way to organize their sustainability data and thus ensure recognized and consistent sustainability reporting. This not only promotes compliance, but also strengthens trust in the entire supply chain and contributes to the creation of sustainable business practices.

With the VSME, SMEs can better arm themselves against excessive or contradictory ESG requests from large customers. Without a clear framework, many large companies today demand very individual and often unnecessarily detailed data sets. The Voluntary Standard creates a uniform, comprehensible basis here: SMEs can refer to a recognized standard, report more quickly and do not have to start from scratch with every request. Voluntary reporting saves effort and at the same time ensures greater security and consistency in communication.

Banks and financial institutions are now asking about ESG issues much more frequently. This is usually done via questionnaires or scorings. Those who can provide reliable data often have a better chance of obtaining financing, for example through more favorable conditions. If this information is missing, on the other hand, it can become more difficult to obtain loans or maintain existing credit lines.

VSME reporting helps SMEs to respond to precisely these requirements in a structured manner: environmental, social and governance issues are presented in a comprehensible manner. At the same time, the company shows that it takes the issue seriously and acts proactively, which can noticeably strengthen the trust of lenders.

The EU guidelines on sustainability are constantly changing. What is currently still voluntary could become mandatory in the near future. Small and medium-sized companies that get to grips with the VSME standards at an early stage are better prepared for future regulations and can thus gain a competitive advantage.

A transparent sustainability report in accordance with VSME shows that the company takes responsibility and is seriously concerned with sustainability. Especially as public, political and market expectations are rising, this can improve the company's public image and build trust.

Many customers, investors and business partners are increasingly paying attention to whether ESG issues are disclosed in a comprehensible manner. Those who create clarity here at an early stage can stand out positively and derive new opportunities in competition from this.

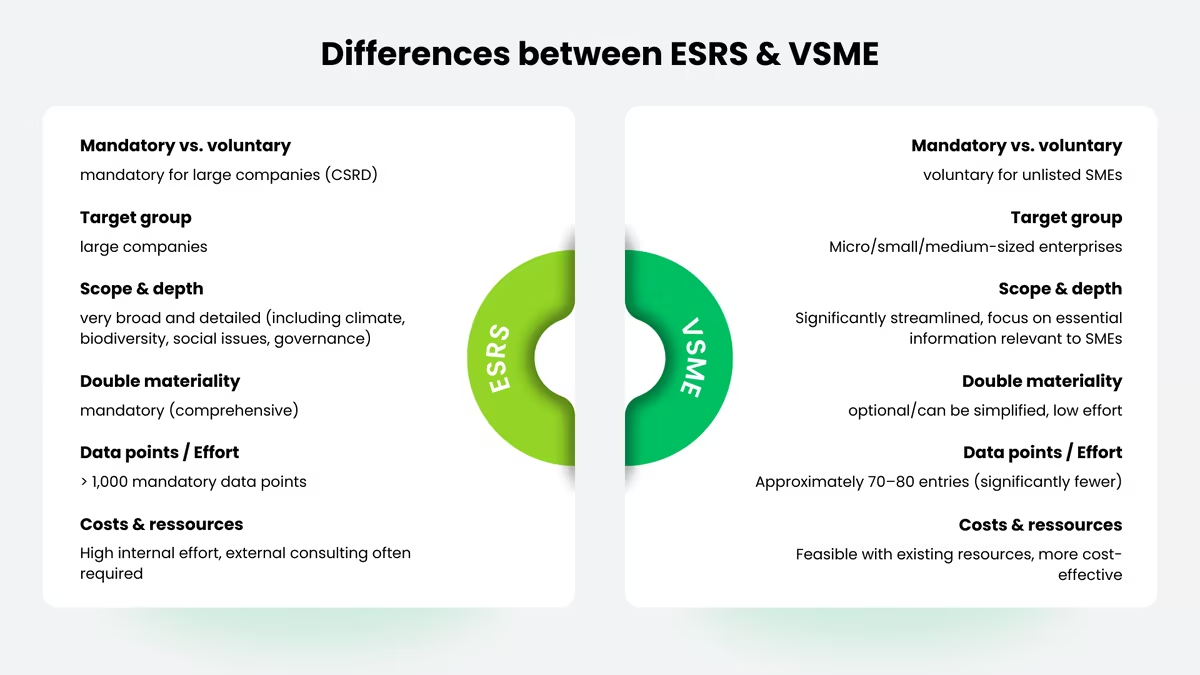

Differences between ESRS and VSME

The ESRS are mandatory for large companies and require very extensive reporting, for example on climate change, biodiversity and social issues. The VSME, on the other hand, is intended for unlisted SMEs and is voluntary. It is much leaner and focuses on the issues that are really relevant for this size of company in practice.

A materiality analysis is mandatory under the ESRS, whereas it is only optional under the VSME standards. In addition, the ESRS (European Sustainability Reporting Standards) include more than 1,000 mandatory data points, which can lead to a considerable amount of additional work compared to the approximately 75 data points of the standards. This reduced data collection makes the VSME standards more cost-efficient and practicable for SMEs striving for sustainable corporate management despite limited resources.

VSME differs from ESRS in the following points:

- Voluntary vs. mandatory: The ESRS are mandatory for large companies in the EU that are subject to the CSRD. In contrast, the VSME are optional standards for small and medium-sized enterprises, which can decide for themselves whether and to what extent they wish to provide information.

- Scope and depth of reporting: The ESRS cover a wide range of topics, from climate change and biodiversity to social issues and governance. They require correspondingly detailed information. The VSME is much leaner: it deliberately reduces the depth and scope so that even companies with limited resources can provide the most important ESG information in a structured manner.

- Materiality analysis to determine the scope: The ESRS requires a comprehensive materiality analysis to determine all relevant topics and to meet the legal requirements. In contrast, a simplified materiality analysis can be carried out for sustainability in accordance with VSME, which requires fewer resources and less effort. This focuses specifically on the aspects that are directly material to the company, which enables efficient and practical implementation of compliance objectives.

- Costs and resources: The introduction of ESRS requires considerable effort, often involving the use of external consultants and additional internal resources. In contrast, the VSME was designed for small and medium-sized companies in such a way that it can be implemented with existing resources. This leads to a significant reduction in the use of costs and resources and enables companies to adapt to legal requirements in the long term.

Basic and Comprehensive Modules

The VSME standard comprises two modules: the Basic Module and the Comprehensive Module. Both modules can be used both at individual company level and on a consolidated basis. The following applies: the Basic Module forms the basis and is a prerequisite, while the Comprehensive Module can be used as a supplement ("on top") if more in-depth reporting is required or desired.

In practice, it is recommended that the VSME report is updated annually, especially if it is prepared at the request of larger companies or financial institutions. This allows the report to be synchronized with the annual financial statements or financial reporting. The SME itself decides whether to publish the VSME report. Certain sensitive information may be omitted; in this case, however, it must be stated transparently that this content could not be disclosed. From the second reporting year onwards, comparative figures from the previous year should also be included in order to present developments in a comprehensible manner.

The modules also follow the "if applicable" approach. This means that an SME using the VSME is only obliged to provide the information that is actually relevant to its own business model and situation.

Note: Basic provides the resilient ESG core for typical requests, Comprehensive adds context and depth when stakeholders expect more detail.

Basic module

The Basic module includes the minimum disclosures (B1-B11) and is designed so that even SMEs with limited resources can produce a consistent report.

1) General company information (B1/B2)

- Module used (Basic or additionally Comprehensive) and reporting boundary (single entity/consolidated)

- Company profile: legal form, sector (e.g. NACE), size (turnover/total assets), employees (headcount & FTE), country of main activity

- Group information: subsidiaries and addresses, if applicable

- Locations of significant assets (land/real estate, if applicable)

- Certificates/awards (if available): Issuer, date, result if applicable

- Reference to undisclosed sensitive information (if applicable)

- Brief description of existing practices, policies, objectives and measures (if any)

2) Environment (E) - Basic key figures (B3-B7)

- Energy consumption (broken down into renewable/non-renewable)

- Greenhouse gas emissions Scope 1 and Scope 2 (estimate permissible depending on data available)

- Pollutant emissions (only if internally/legally relevant)

- Water withdrawal and water consumption (if relevant)

- Waste & recycling / circular economy practices

3) Social (S) - Employee-related information (B8-B10)

- Employee structure (e.g. contract types)

- Breakdowns (e.g. gender, countries of origin if applicable - only if collected/permitted)

- Remuneration-related disclosures (aggregated, depending on requirements)

4) Governance (G) - Integrity/compliance (B11)

- Convictions and fines in connection with corruption and bribery (if any)

Comprehensive module

The Comprehensive module adds more in-depth information to the Basic report. This is particularly helpful if banks or customers require more context or if an SME wants to present its ESG positioning more clearly.

Typical additional content:

- Business model & strategy (C1) - central value creation, strategic orientation

- Policies, measures & transformation plan (C2) - existing practices, goals, planned steps

- In-depth environmental disclosures (C3-C4) - additional key figures/explanations depending on relevance

- In-depth social disclosures (C5-C7) - e.g. other HR/labor practices

- Revenue from certain sectors (C8) - if relevant

- Diversity in management and supervisory bodies (C9) - in particular gender diversity

To ensure that the VSME report does not become unnecessarily time-consuming, it is worth having a clear procedure.

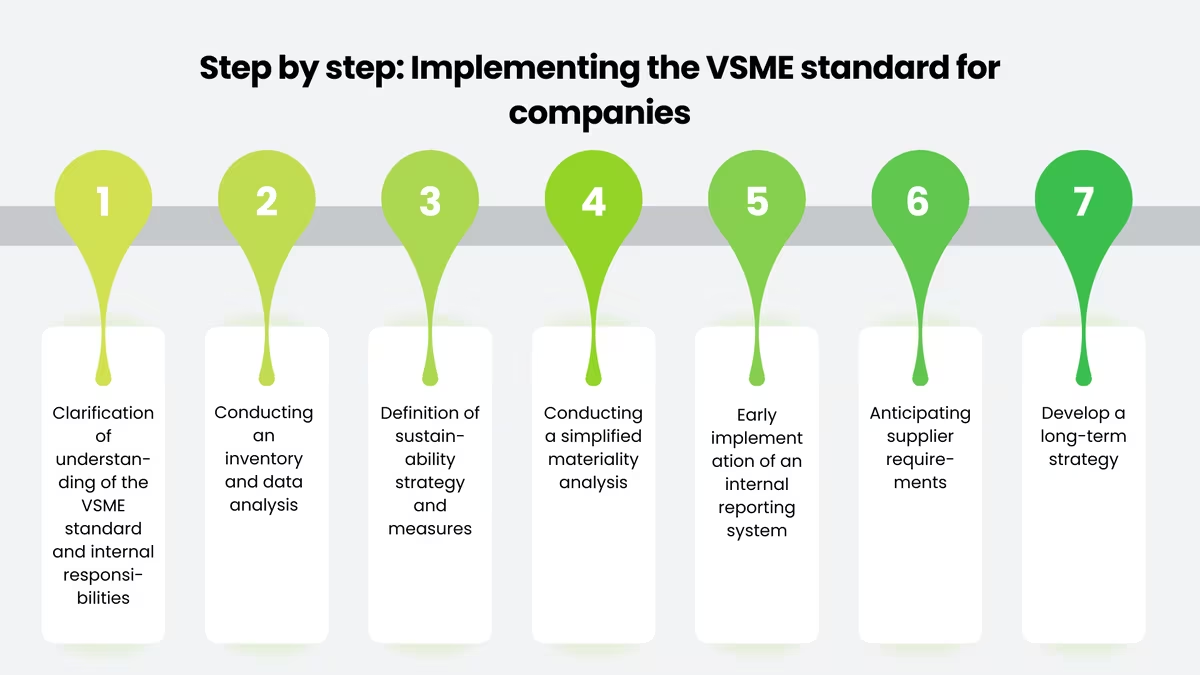

Implementation of the VSME standard

Before you start, you should briefly familiarize yourself with the requirements of the draft VSME. It is also important that clear responsibilities are defined internally, for example at management level, in controlling or with a person responsible for sustainability. This is the only way to ensure that the process is properly managed.

- Which topics and key figures need to be recorded?

- Which internal departments are responsible for data collection?

- Do ESG data already exist that can be used?

In order to determine what information is required for the report, it is necessary to carry out an inventory. This analysis helps to develop a realistic plan for data collection. The following points, for example, can be clarified:

- What ESG data is already available (e.g. energy consumption, CO₂ emissions, social responsibility)?

- What gaps still exist?

- Where can the missing data be obtained (e.g. from suppliers, external consultants)?

The standard goes beyond mere reporting and gives companies the opportunity to formulate a well thought-out ESG strategy. Companies should ask themselves the following questions:

- What long-term sustainability goals do we want to strive for?

- What steps can we take to improve our ESG performance?

- Are there existing initiatives that can be integrated into the report?

SMEs should carry out a simplified materiality analysis in order to prioritize the issues that really matter in their own business, for example energy consumption, CO₂ emissions or working conditions. It is helpful to talk to key stakeholders, especially major customers: This quickly makes it clear what information is actually expected in practice.

An internal system for collecting sustainability data should be used as early as possible. This is the only way to ensure effective data collection and regular reporting, even if it is initially only used internally.

Small and medium-sized enterprises should take active steps to clearly signal to large customers that they are reporting in accordance with VSME standards. In this way, excessive or arbitrary demands from suppliers can be avoided. It also promotes transparency and consistency in the SME supply chain.

Even if the VSME is voluntary, it is worthwhile for SMEs to set up the topic for the long term, with clear goals and a strategy that is regularly reviewed and adapted. This strengthens the company's position in the supply chain and makes it more resilient if sustainability reporting requirements evolve in the future.

A clear strategy not only supports reporting, but also helps to position the company advantageously in competition. Especially now that many companies will probably no longer be covered by the CSRD, resources can be used to focus on specific sustainability measures.

Conclusion

The VSME provides SMEs with a practical way to prepare ESG information in a structured manner without the effort of the full ESRS. This is particularly relevant for companies that regularly have to provide sustainability certificates for customers, business partners or banks. A double materiality analysis is not required and the scope remains manageable.

Even if the omnibus initiative could further reduce regulatory pressure, the demand for ESG data remains. Those who adapt to the VSME at an early stage not only create transparency, but also secure a real competitive advantage.

Frequently asked questions

The VSME standard (Voluntary Standard for SMEs / SMEs VSME) is a voluntary sustainability report for small and medium-sized enterprises that do not fall under the CSRD obligation but still have to provide ESG data, for example for business partners or banks. It offers a simplified alternative to the extensive ESRS standards and helps SMEs to document their sustainability practices in an efficient and standardized manner.

The standard is voluntary and is aimed at companies that are not subject to CSRD, usually SMEs. It enables structured ESG reporting in order to meet the sustainability requirements of business partners, banks or investors without the high bureaucratic hurdles of the ESRS.

The VSME standard is a simplified and voluntary alternative to the ESRS. While the ESRS requires over 1,000 data points and a comprehensive materiality analysis, the VSME standard only comprises around 75 data points and does not require a double materiality check. It is specifically tailored to the limited resources of SMEs and makes ESG reporting considerably easier.

The VSME standard records key ESG data on the environment, social issues and corporate governance. This includes energy consumption, CO₂ emissions (Scope 1 & 2), water consumption, waste management, employee numbers, diversity and governance practices. Depending on the module (Basic or Comprehensive), the requirements vary in scope, but are always designed to be practical and resource-efficient for SMEs.

The VSME standard consists of two modules:

- Basic module: Contains minimum requirements for micro-enterprises, e.g. company structure, energy consumption, CO₂ emissions, water and waste management as well as social aspects such as employee numbers and diversity.

- Comprehensive Module: Provides more detailed reporting, including business model, sustainability strategy, supply chain information and more comprehensive environmental and social data.

Companies can choose the right module depending on their needs and resources.

No, a materiality analysis is not mandatory under the VSME standard, but it is optional. In contrast to the ESRS, which require a comprehensive double materiality assessment, the VSME standard allows SMEs to decide for themselves which ESG topics are relevant to them and report on them. This saves time and reduces bureaucracy.

The standard enables SMEs to carry out simple, cost-efficient and standardized ESG reporting without the high requirements of the ESRS. It helps to document sustainability data transparently, facilitates access to financing and strengthens competitiveness. It also protects SMEs from excessive ESG requests from large companies and prepares them for future regulatory requirements.

The VSME standard enables SMEs to provide structured ESG reporting that meets the requirements of large business partners. As many corporations require ESG data from their suppliers, the standard helps to provide relevant sustainability information in a consistent manner, reduce bureaucracy and avoid unclear or excessive requests. This enables SMEs to improve their supply chain compliance and strengthen long-term business relationships.

Yes, the VSME standard can help SMEs with financing from banks, as many credit institutions include ESG criteria in their assessment. A standardized sustainability report according to VSME shows that a company operates sustainably, improves the ESG score and can lead to better credit conditions. It also increases transparency and strengthens the trust of investors and financial partners.

Companies should first understand the VSME standard and define an internal responsibility for ESG reporting. This is followed by an inventory of existing sustainability data (e.g. energy consumption, CO₂ emissions, employee numbers). They should then define a sustainability strategy, introduce a simple internal reporting system and, if necessary, take supplier and stakeholder requirements into account. Gradual implementation facilitates integration into existing processes.

Alexander Hilmar

LinkedInESG compliance expert - lawcode GmbH

Alexander Hilmar advises companies on the implementation of ESG compliance, sustainable reporting and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.