Important facts

- What role does company size play in EUDR obligations?

- The EUDR makes a clear distinction between large companies and SMEs. This determines whether full or simplified due diligence obligations apply.

- How are SMEs defined under EU law?

- Less than 250 employees and no more than € 50 million turnover or € 43 million balance sheet total, based on EU Recommendation 2003/361/EC.

- Why is the group structure decisive for the threshold test?

- Because the relevant values (employees, turnover, balance sheet) of affiliated companies must be calculated on a consolidated basis, even across national borders.

- Is a subsidiary automatically considered an SME if it is small?

- No. If the parent company or other affiliated companies are large, the subsidiary may lose its SME status.

- What exactly do SME retailers need to do to be EUDR-compliant?

- They must ensure that they can produce, pass on and archive a valid reference number of the due diligence declaration for each product.

- What does the reference number mean in practice?

- It is proof that a product has undergone EUDR-compliant due diligence and must be carried with every transaction.

- How can EUDR implementation be organized efficiently within the Group?

- Through a clear allocation of roles (market participant vs. trader), central threshold checks, compliance processes and digital systems for managing reference numbers.

Executive Summary

The EU Deforestation Regulation (EUDR) imposes different due diligence obligations on companies depending on their role in the supply chain and company size. While market participants must implement a complete due diligence system including risk analysis and due diligence declaration, simplified requirements apply to traders, especially SMEs. Whether a company is considered an SME is based on the EU definition in accordance with Recommendation 2003/361/EC. The decisive factors here are fewer than 250 employees and an annual turnover of no more than 50 million euros or a balance sheet total of no more than 43 million euros. In the case of affiliated companies, for example within group structures, these thresholds must be examined on a consolidated basis. This means that a subsidiary can no longer be considered an SME despite its own small structure if the group of companies as a whole exceeds the thresholds and the EUDR turnover limits.

Although SME traders do not need to carry out their own risk analyses, they must document the market participant's due diligence declaration, provide evidence of this via a reference number and archive the information for at least five years. Clear clarification of roles within company groups and documented, system-based handling of reference numbers are key requirements for legally compliant EUDR implementation. Companies should regularly review their classification and establish suitable measures for implementation by the start of application of the EUDR on December 30, 2026, as no transitional periods are planned.

EUDR: objectives, background and obligations

The EUDR (EU Deforestation Regulation) aims to curb deforestation and forest damage worldwide by ensuring that only deforestation-free products enter the EU. It applies to companies that import certain raw materials or products into the EU or sell them within the EU. The regulation distinguishes between different types of companies.

There are some exceptions or simplified rules for small and medium-sized enterprises (SMEs). The exact requirements that apply often depend on the size and structure of the company in question.

In day-to-day business, groups of companies in particular, such as parent companies, subsidiaries, holding companies or joint ventures, are often faced with the question of how to correctly determine and apply the thresholds and obligations of the EUDR. In addition, there is often uncertainty as to what role a company plays in the supply chain, whether as a market participant or as a trader, and how this affects implementation (e.g. due diligence obligations, documentation, risk assessment). Particularly in the case of complex corporate structures or small companies with a strong division of labor, it is important to identify the obligations precisely.

When do which EUDR obligations apply?

By December 31, 2026, companies in the EU must be able to demonstrate transparently that their products do not contribute to deforestation or forest degradation. The regulation particularly affects players that import relevant raw materials such as wood, coffee, cocoa, soy, palm oil, rubber and cattle products or are the first distributors in the EU. Products made from these raw materials are also important and must be taken into account. The EUDR makes a clear distinction as to whether a company acts as a market participant or trader and whether it is an SME as defined by the EU.

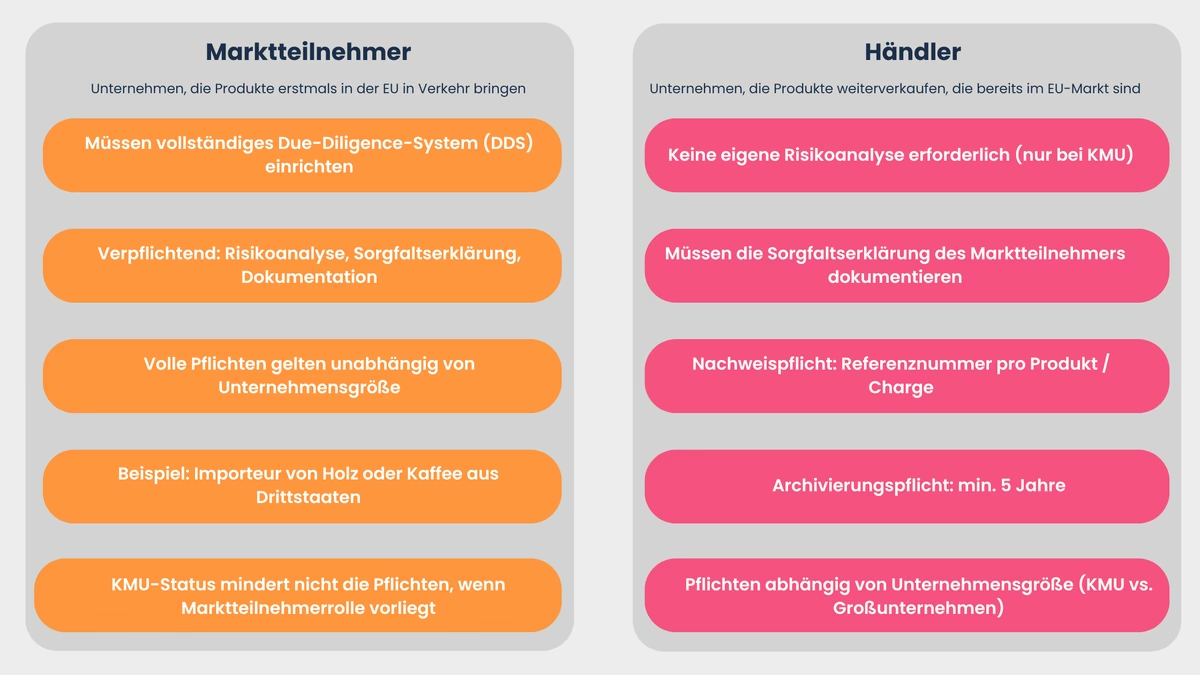

Market participants vs. traders - key distinction of the EUDR

The EUDR initially differentiates according to the "functional role" of the participants concerned. In simple terms, a market participant is a company that places products on the EU market for the first time or exports them from the EU. Typical market participants are importers and manufacturers. Distributors, on the other hand, trade in products that are already available on the internal market, such as wholesalers or retailers, provided they do not act as market participants themselves.

Market participants are subject to the full due diligence obligation under the EUDR: they must submit their own due diligence statement, trace the origin of the products, obtain geographical data and prove that the products do not contribute to deforestation. Furthermore, a due diligence statement must be submitted for each shipment prior to import/export.

This does not make traders who are not SMEs second market participants. Since the targeted adjustment at the end of 2025, the obligation to submit a due diligence declaration lies exclusively with operators who supply or export a product to the EU market for the first time. As a rule, downstream actors do not have to submit their own DDS, but work with references and traceable documentation, depending on their specific role in the flow of goods.

Small and medium-sized traders, on the other hand, benefit from simplifications in certain cases. Qualification as a market participant or trader and classification as an SME are therefore key factors in EUDR compliance.

Market participants vs. traders - the most important differences:

- Market participants bring products into the EU for the first time - full due diligence incl. DDS, traceability and geodata

- Non-SME dealers do not provide their own DDS - work with references and traceable documentation

- SME traders benefit from additional simplifications

Standard obligations and simplifications - the importance of company size

The standard obligations of the EUDR apply to all market participants, regardless of size. For traders, however, the decisive factor is whether or not the company qualifies as an SME as defined by the EU. The EUDR provides significant relief for traders who are classified as SMEs, as they do not have to submit a separate due diligence declaration for each delivery. Under certain conditions, they may refer to the due diligence declarations of their upstream suppliers. Nevertheless, a number of documentation and cooperation obligations remain, e.g. to retain the due diligence declarations and in the event of inquiries from authorities.

From a practical point of view, it is therefore crucial whether a company, and thus also affiliated or subsidiary companies in the group, exceeds or falls below one of the EUDR thresholds or turnover limits.

Special case: micro and small "primary operators"

In addition to the simplifications for SME traders, there has been a second simplification component since the targeted adjustment at the end of 2025 that is often overlooked. It is aimed at micro and small primary operators, i.e. actors who produce relevant raw materials or products themselves and place them on the market for the first time. This group is not required to submit a full due diligence declaration for each process. Instead, a one-off simplified declaration in the EU system is sufficient, from which a declaration identifier is then generated. This identifier then serves as a verification and traceability anchor for the products concerned. In certain cases, these primary operators may also provide a postal address if this clearly assigns the production to a location.

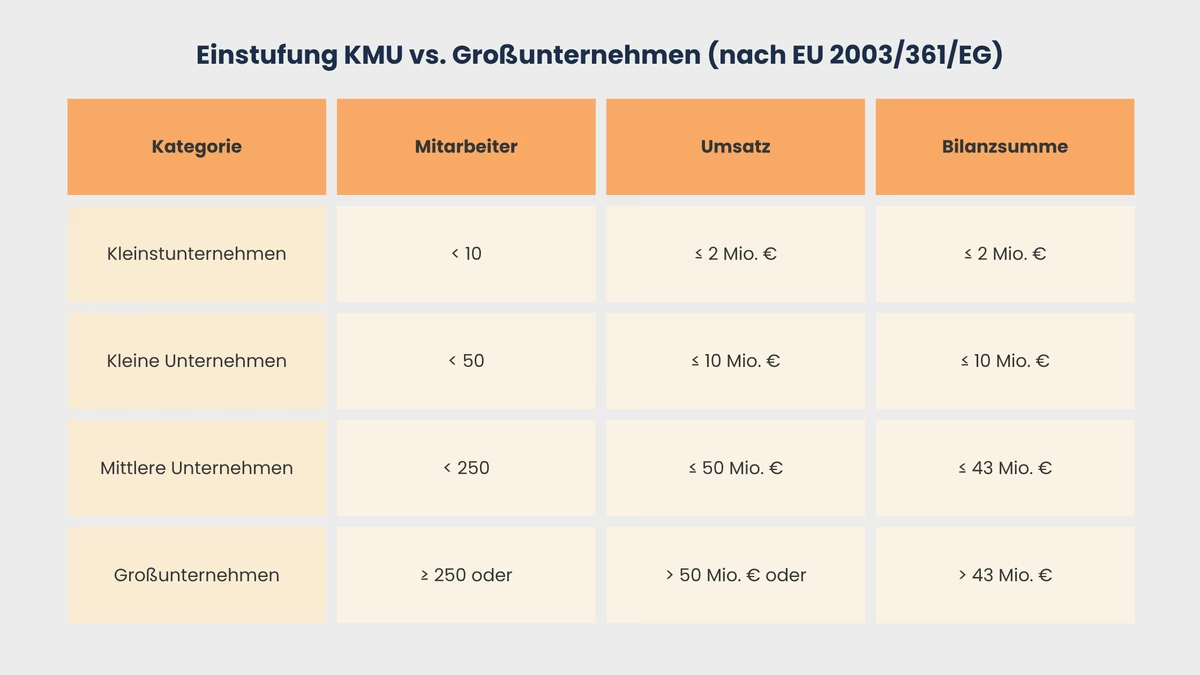

The EU SME definition: thresholds at a glance

In the context of the EUDR, the term SME is generally based on the European Commission's Recommendation 2003/361/EC. The definition based on this sets precise financial and personnel thresholds.

A company is considered an SME if it has fewer than 250 employees and either an annual turnover of no more than 50 million euros or an annual balance sheet total of no more than 43 million euros. The decisive factors here are all employees and the consolidated financial figures within a group of companies, provided the company is affiliated with others.

The SME classification according to this definition also makes a further distinction within SMEs between micro-enterprises (fewer than 10 employees and no more than EUR 2 million turnover or balance sheet total), small enterprises (fewer than 50 employees, no more than EUR 10 million turnover or balance sheet total) and medium-sized enterprises (fewer than 250 employees, no more than EUR 50 million turnover or EUR 43 million balance sheet total). The reference to Recommendation 2003/361/EC is expressly binding for the application of the EUDR and helps to ensure uniform thresholds throughout Europe.

SME thresholds:

- Microenterprise: < 10 employees, ≤ € 2 million turnover or balance sheet total

- Small companies: < 50 employees, ≤ € 10 million turnover or balance sheet total

- Medium-sized companies: < 250 employees, ≤ € 50 million turnover or ≤ € 43 million balance sheet total

The level of the respective thresholds determines whether a company can claim regulatory relief (e.g. as an SME trader) or has to fulfill the full EUDR due diligence obligations of a market participant. The correct classification of company size requires a detailed examination - particularly with regard to shareholdings and group structures.

Group structures and holding companies - how are they counted?

In practice, many companies are part of groups, operate as subsidiaries, holding companies or have indirect shareholdings through subsidiaries. When implementing the EUDR, it is important to check whether a company is assessed individually. In some cases, however, the entire group of companies must be considered together in order to determine whether the SME thresholds have been exceeded.

Basic principle: Individual consideration of the legal entities

In principle, individual legal entities are considered under European law. A company that has its own legal existence and entry in the commercial register is therefore treated as an independent entity. As a result, the EUDR obligations are triggered at the level of the respective legal entity. However, this does not mean that group membership and economic interdependence with other companies are disregarded. The EU provides explicit rules for dealing with affiliated companies and partner companies, particularly for the application of the SME definition.

Consolidated view of affiliated companies

The EU SME Recommendation(Annex, Article 3) explicitly states that in the case of affiliated companies - i.e. groups, joint ventures, holding structures or subsidiaries with binding control - the thresholds are to be calculated on a consolidated basis. In concrete terms, this means that all employee numbers, turnover and balance sheet totals of the affiliated companies are added together in order to check the EUDR thresholds. Affiliated companies within the meaning of the definition are those that are majority-owned, directly or indirectly under common control or - conversely - constitute a subsidiary in terms of decision-making power and economic interdependence.

The EUDR turnover limit and the EUDR balance sheet total therefore apply at the level of the entire group, particularly in the case of internationally operating groups of companies that have their own purchasing or sales subsidiaries in several EU countries, for example. It is therefore not just the isolated size of the company that matters, but the entire "group". The Commission and the EUDR guidelines emphasize that the due diligence obligations should not be circumvented through artificial splits ("carve-outs").

For example: If a German parent company has 100 employees and a turnover of 49 million euros, but has a subsidiary in France with 170 employees and a turnover of 6 million euros, the relevant turnover for the EUDR threshold is the total value of 55 million euros (49 + 6), even if both companies individually would be below the SME threshold.

Examples of classification

A German subsidiary of an international group imports coffee products independently and operates as an independent legal entity. The company has 40 employees, a turnover of 6 million euros and a balance sheet total of 4 million euros. Its parent company, based in France, has 180 employees and a turnover of 30 million euros. As both companies are deemed to be affiliated companies, the key figures of both companies are added together when calculating the thresholds. If the overall group exceeds 250 employees or 50 million euros in turnover, the German subsidiary is not considered an SME either.

A wholly owned subsidiary only provides internal services for the parent company and does not have its own market presence or customers, but effectively acts as a service company. However, it has its own entry in the commercial register and prepares its own accounts. Here too, the employee and financial values of the parent company are attributed. Operational independence is not decisive for the SME classification as long as a participation threshold is reached.

A holding company holds 100% of the shares in each of five companies, each of which has 30 employees and a turnover of EUR 6 million. Each subsidiary must be checked to see whether it is considered a separate SME. The decisive factor here is that, according to EU regulations, the number of employees and turnover of all affiliated companies are also taken into account. This means that the threshold of 250 employees and 50 million euros in turnover is exceeded, meaning that none of the subsidiaries are considered to be independent SMEs, even if they were individually small.

These examples show how important careful group-wide analysis and documentation is in order to be able to assess one's own EUDR obligations in a legally compliant manner.

Requirements for SME retailers in the supply chain

Many small companies are not market participants under the EUDR, but only act as traders. They sell products that other, usually larger, companies have already imported into the EU. According to Article 6 of the EUDR, special, simplified rules apply to such SME distributors.

Facilitations for SME traders according to EUDR

The EUDR regulations stipulate that SME traders are not obliged to carry out their own due diligence statement (DDS) for affected products. An independent risk analysis, as required for market participants, is also not required for this group of companies. The EU Commission justifies this simplification by reducing the administrative burden for smaller companies. This significantly reduces the workload for SME traders: they can focus on core obligations without being subject to the comprehensive documentation and analysis obligations of market participants.

The distinction is important: the simplifications for SME traders relate to traders who resell products that have already been covered by an operator. The simplification for micro and small primary operators, on the other hand, is a separate mechanism at the beginning of the chain and works with a one-off simplified declaration and a declaration identifier instead of a complete DDS per transaction.

Obligations that nevertheless exist

Even though SME traders are exempt from many administrative obligations, they are not completely exempt from the EUDR. Key obligations include, in particular, the fact that every trader must provide evidence of and archive the market participant's due diligence declaration. For each transaction, it must be ensured that a unique reference number for the respective due diligence declaration is available and can be clearly assigned to this product or its batch.

In addition, the EUDR requires SME traders to keep the evidence for the competent authorities or audits for at least five years. This documentation obligation extends to all transactions with affected products within the supply chain.

Reference number instead of full DDS - what does this mean in concrete terms?

The reference number is the central link in EUDR compliance for SME traders. It refers to the due diligence declaration issued by market participants and must be documented for each delivery. In practice, this means that the reference number for each delivery or batch must be clearly assignable internally, archived in an audit-proof manner and transferable if required. Many companies solve this by carrying the predominant reference in ERP and document processes without having to generate new proofs at each stage of the chain.

From a technical perspective, companies can adapt existing ERP, merchandise management or compliance systems so that the recording, archiving and reporting of the reference number is automated. Organizationally, clear processes must be established to ensure that the associated due diligence declaration is clearly linked to each relevant transaction and can be checked at any time. Safeguarding against sources of error, duplication or loss of reference numbers is crucial, as missing or incorrect information can lead to sanctions in the event of an audit.

Recommendations for action for corporate groups and SMEs

Clarification of the distribution of roles within corporate groups

Within companies or groups of companies, a clear distinction must first be made between market participants and traders. Who is actually importing into the EU for the first time? Who is reselling? These questions are also important for the practical division of tasks. In the case of related business activities, it is advisable to install a responsible function (e.g. compliance officer), which takes over the allocation and monitoring of EUDR obligations and ensures group-wide consistency. It must be documented for each individual company in the group whether it acts as a market participant or trader within the meaning of the EUDR. It makes sense to clearly define the due diligence obligations and, if necessary, have them handled centrally by the parent or holding company, provided this is possible in accordance with the law.

Uniform valuation within the Group

The review of SME status and the relevant thresholds should be documented annually in a comprehensible manner as part of the financial statements or reporting on the corporate structure. Close coordination with the internal legal and compliance department is recommended in order to ensure a uniform interpretation of the relevant EUDR thresholds within the group. Every change in the corporate structure - for example, due to new investments, divestments or newly founded companies - must be transparently included in the assessment. The documentation of the threshold test is also essential because it can be used as proof of the claimed simplifications or obligations in the event of an audit.

For SME dealers: Efficient system for managing reference numbers

SME traders are recommended to use existing software solutions such as ERP or compliance systems to manage the EUDR reference numbers. Are you already familiar with our EUDR module? With this module, all necessary EUDR-relevant checks can be carried out automatically in just one platform. It makes sense to integrate the entry of the reference number as a mandatory field in the workflow for goods receipt, invoicing and warehouse management. At the same time, companies benefit from clear processes for passing on the number within the supply chain, archiving and audit-proof storage. Every employee in retail, purchasing or sales should be made aware of the importance of the reference number so that there are no gaps in verification. A precisely documented and regularly reviewed process for managing reference numbers reduces the risk of official complaints and ensures legal certainty for all transactions.

To Do:

- Clarify for each company in the group whether it acts as a market participant or trader - and document this role assignment in a comprehensible manner.

- Designate a central compliance function that coordinates EUDR obligations across the Group and ensures uniform interpretation.

- Check the SME classification annually and include changes in the company structure - such as new investments - transparently in the assessment.

- Integrate EUDR reference numbers as a mandatory field in existing ERP or compliance systems and firmly anchor their management in goods receipt, invoicing and archiving.

Conclusion

Correct classification as a market participant or trader is the crucial first step; mistakes here can have serious legal consequences. SMEs benefit from simplifications, but remain under obligation: documentation and management of due diligence declarations and reference numbers must be designed in an audit-proof manner.

In group structures, the consolidated thresholds of the group always apply, so close coordination with the legal and compliance department is essential. Those who clearly assign roles, regularly check thresholds and introduce efficient systems for reference number management create the basis for legally compliant EUDR compliance.

Frequently asked questions

As soon as a company, together with its affiliated companies, exceeds the thresholds defined in Recommendation 2003/361/EC, it loses its status as an SME for the EUDR. This means that, as a trader, it must carry out the due diligence obligations and any risk analyses itself and can no longer benefit from the simplifications.

Yes, when assessing the SME thresholds, foreign companies are also to be considered together with the subsidiary based in the EU, provided that they are affiliated companies within the meaning of EU law. The consolidated values of the entire group are always used.

With a professional system for collecting, managing and archiving EUDR reference numbers, SME retailers ensure that they can prove at any time which due diligence declaration their products are based on in the event of official inspections. This prevents sanctions and considerably simplifies the obligation to provide evidence.

The EUDR itself does not provide for any transitional periods: The requirements will come into force from December 30, 2026 due to several postponements of the EUDR. Companies should therefore review their structures at an early stage and make the necessary adjustments in order to be legally compliant from this date.

The competent authorities of the EU Member States are responsible for compliance, monitoring and enforcement of the EUDR. They may carry out audits, spot checks and inspections and request complete information from companies - in particular due diligence declarations, associated reference numbers and other evidence. Violations may result in fines or other sanctions.

Karim Boukaouche

LinkedInESG-Compliance Experte · lawcode GmbH

Karim Boukaouche berät Unternehmen bei der Umsetzung der EU-Entwaldungsverordnung (EUDR) und begleitet die Implementierung digitaler Lösungen für rechtssichere Lieferketten. Seine Fachbeiträge auf dem lawcode Blog verbinden regulatorische Tiefe mit praxisnahen Handlungsempfehlungen.