Important facts

- What is the HS code?

- The six-digit HS code is a globally used system for classifying goods in international trade.

- How does the TARIC code differ?

- The TARIC code adds two more digits to the eight-digit CN code to create a ten-digit code number. It represents EU-specific measures such as customs duties, import restrictions and regulatory obligations - including the EUDR - in the customs declaration.

- What role do HS and TARIC codes play in EUDR?

- The EUDR uses HS and TARIC codes to identify the goods concerned and to ensure due diligence.

- Where can companies find the relevant HS and TARIC codes?

- The EZT-Online and TARIC platforms are central points of contact.

- What is the function of the Y-codes?

- Y-codes provide specific information on exceptions.

- Why is the correct classification of goods important for companies?

- The precise classification of goods using HS and TARIC codes is crucial to ensure smooth import and export.

Executive Summary

The HS Code is a six-digit, globally recognized system for classifying goods in international trade. The EUDR integrates it to identify affected goods and their due diligence requirements. The TARIC code is an EU-specific extension of the HS/CN code to ten digits, which maps additional EU measures such as customs duties, import restrictions and regulatory requirements for imports. The separation of functions is important: Which goods fall within the scope of the EUDR is determined by Annex I of the regulation - where the products concerned are listed using CN codes. TARIC serves as a vehicle in the customs declaration to indicate how the EUDR requirement is fulfilled in a specific case using specific document and exception codes (C and Y codes).

The connection between the two codes is central: their combination ensures that goods are correctly classified, subjected to a due diligence check and identified as deforestation-free.

Companies can find the relevant HS codes via EZT-Online (German customs platform) and TARIC codes in the European Commission's EU customs tariff database. In addition, the EUDR Regulation itself contains information on the codes concerned.

Recommendations for action

→ Regularly check the classification of goods: Systematically check that HS and TARIC numbers are up to date.

→ Establish due diligence processes: Clear internal processes for risk assessment and documentation ensure traceability along the supply chain.

→ Actively involve suppliers: Inform suppliers about EUDR requirements at an early stage and oblige them to provide proof of origin.

→ Use technical expertise: Customs and compliance experts or specialized software solutions help to avoid classification errors.

Never miss an update on the EUDR again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Difference between HS codes and TARIC codes

The HS code (Harmonized System) is the internationally recognized classification system of the World Customs Organization (WCO). With six digits, it forms the global basis and ensures that goods can be classified uniformly worldwide. Countries and economic areas build on this and add further digits for their regulatory purposes.

In the EU, the code structure works in three successive steps:

→ Digits 1-6 (HS code): worldwide goods nomenclature of the WCO.

→ Digits 7-8 (CN code, Combined Nomenclature): EU-specific subdivision. It is the basis for all import and export declarations and for intra-Community trade statistics. Annex I of the EUDR also works at this level.

→ Digits 9-10 (TARIC): EU measures such as customs duties, anti-dumping duties, import restrictions and regulatory obligations such as the EUDR. The TARIC is used for import declarations.

→ Digit 11: national code number for Member State-specific regulations (e.g. national bans or statistical purposes).

Practical consequence: When exporting, the eight-digit commodity code (CN code) is usually sufficient. For imports, the ten-digit code number (CN + TARIC) is given, supplemented in Germany by the eleventh national digit.

Note: Annex I of the EUDR defines at CN level which products are covered. TARIC supplements this information in the customs declaration with specific document codes (C codes) and exception codes (Y codes).

TARIC numbers: A comprehensive overview

The legal basis for the TARIC number is Regulation (EEC) No. 2658/87 of July 23, 1987, which regulates the tariff nomenclature and the Common Customs Tariff of the EU.

TARIC harmonizes EU-specific requirements in trade and comprises two main categories of measures:

- Tariff measures regulate tariff rates and preferences vis-à-vis third countries, tariff quotas and temporary tariff suspensions. In the agricultural sector, there are also specific regulations on additional duties and price fixing.

- Non-tariff measures include trade policy instruments such as anti-dumping and countervailing duties, import and export bans for certain countries or goods and the control of sensitive goods. These include CITES goods, dual-use goods and luxury goods. Veterinary and phytosanitary controls also ensure compliance with safety standards.

Overall, TARIC ensures that all import and export processes comply with EU directives and that integrity and sustainability in international trade are guaranteed.

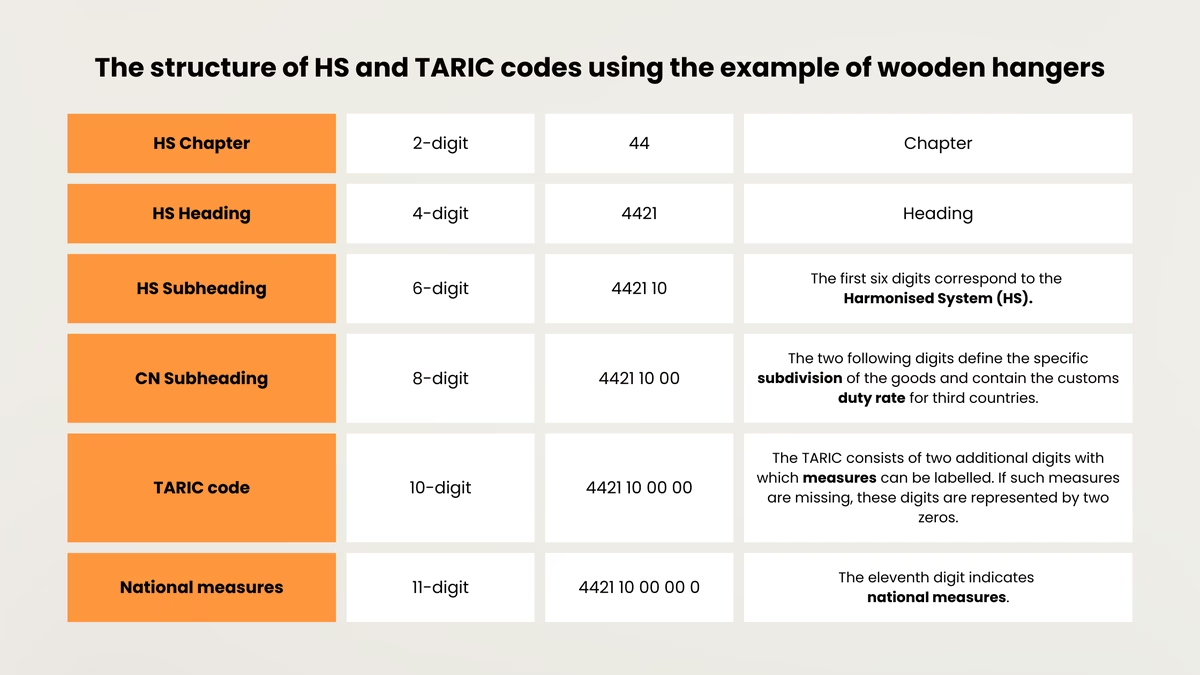

The structure of HS and TARIC codes using the example of hangers

A comparison using the example of wooden clothes hangers illustrates the practical use of these codes. The HS code for your product can provide general information about the product group, while the TARIC code provides specific customs duties or trade-related requirements for imports into the EU. Together, these codes act as a comprehensive system to increase efficiency and regulate international trade activities.

For an import declaration, the ten-digit code number (CN + TARIC) is given; in Germany, an eleventh digit is added for national code numbers. The eight-digit commodity code (CN code) is sufficient for export declarations.

Determination of HS and TARIC codes in the EUDR

The Harmonized System Codes (HS codes) and the TARIC (Integrated Tariff of the European Communities) play a decisive role in the implementation of the EU Regulation on the prevention of deforestation (EUDR). Everything you need to know about the EU Deforestation Regulation can be found here. These codes serve as a basis for the clear identification of product groups that could be affected by the regulation.

HS code change for processing: When do I become a downstream operator?

A question that is often overlooked in practice concerns companies that further process relevant products. The EU Commission has clarified this in the FAQ update (Version 5, FAQ 3.1.1): A change of commodity code (HS, CN or TARIC) only leads to classification as a downstream operator if the change affects the entities listed in Annex I.

An example from the Commission illustrates the principle: Company A in the EU imports unroasted, undecaffeinated coffee (HS 0901 11) and places it on the market. Company B buys it, roasts it and sells it on (HS 0901 21). A is the operator, B remains the trader, because both codes begin with the same four digits (0901) and only these four digits are listed in Annex I. For chapters HS 47 (wood pulp, paper) and HS 48 (paper, paperboard), only the first two digits match.

In practice, this means that for each processing operation, companies should check whether the new code retains the same Annex I-relevant positions or whether it changes to a different Annex I entry - only the latter justifies the role as downstream operator with the resulting information and retention obligations.

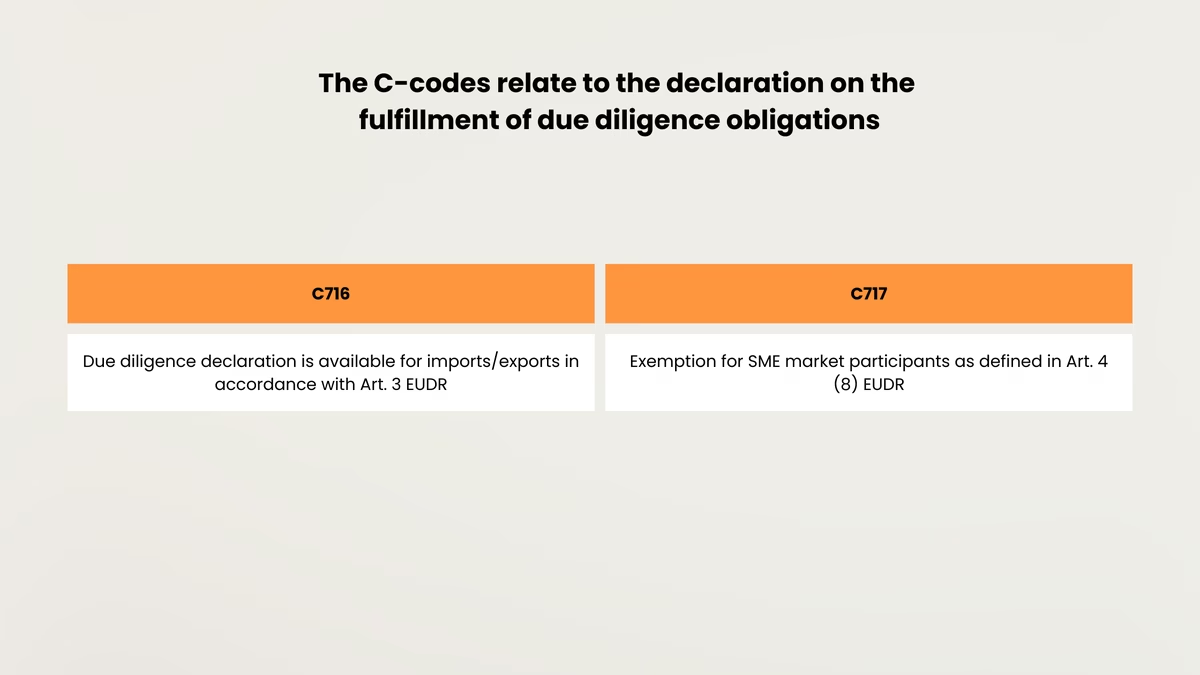

The C-codes relate to the declaration on the fulfillment of due diligence obligations

However, when products covered by the EUDR are imported or exported, it is not immediately possible to determine whether or not they are covered by a due diligence declaration using the existing TARIC alone. For this reason, the EU Commission has published new TARICs in connection with the EUDR, which enable customs to quickly identify whether a relevant product meets the requirements of the EUDR or not.

TARIC code C716

The TARIC document code C716 is important. This indicates that a due diligence declaration is available and that the product may be put into circulation. In practice, this means that if a due diligence declaration is available for the goods in question, the TARIC code C716 must also be indicated on the customs declaration in addition to the full customs tariff number from the date of application of the regulation. When creating the customs declaration, specific entry fields are provided for each of this information, including any additional information such as the description of the goods.

TARIC code C717

Furthermore, a new TARIC code C717 is introduced, which is relevant for SME market participants that are exempt from due diligence in accordance with Article 4(8) EUDR. In other words, affected SMEs do not have to assume due diligence obligations for already declared relevant products that already comply with the due diligence obligation and for which a due diligence declaration is available. This code must be provided to customs if companies are not required to carry out due diligence on products that are already subject to declaration and for which a due diligence declaration is available. C717 serves as a reference number for the previously submitted due diligence declaration.

The logic following the simplifications at the end of 2025 (once-only approach) is important here. Responsibility for the formal DDS lies in principle with the first operator. According to Art. 4(7) EUDR, the operator is obliged to actively pass on the DDS reference number to the first downstream operator or trader. Downstream operators, on the other hand, do not have to actively inquire about their own role: if they do not receive a reference number from their supplier, they may assume in good faith that the supplier is not an upstream operator (FAQ 3.4 and 3.5). In practice, the collection and storage of reference numbers is primarily the responsibility of the first downstream operator. Further verification obligations only apply if there are substantiated concerns and only for non-SMEs. The DDS verification number does not have to be passed on along the chain by law - it can only be requested on a voluntary basis or in the event of substantiated concerns (FAQ 3.6.1).

The timing of the scope changes is important:

The EUDR Regulation itself was revised at the end of 2025 with regard to application deadlines and once-only logic (published in the Official Journal on December 23, 2025). Content adjustments to the product scope - including the exclusion of certain printed products from Chapter 49 (CN) - will be made via a separate delegated act. The current draft (as of May 2026) is still subject to public consultation until June 1, 2026 and will only become binding upon publication in the Official Journal. Companies should therefore prepare their HS Code mappings now, but mark the changes as 'expected' until they are formally adopted.

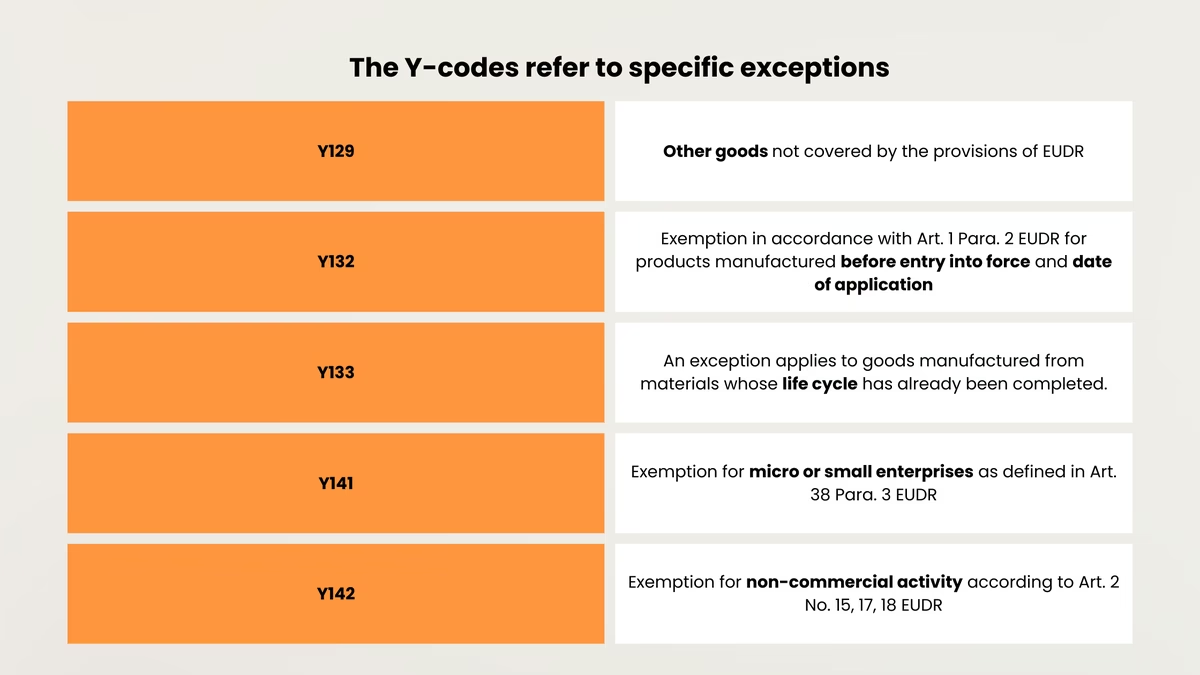

The Y-codes refer to specific exceptions

Y-codes provide specific information on exemptions that are particularly important for small and medium-sized enterprises (SMEs). They also include relevant regulations for goods manufactured from materials whose life cycle is already complete.

A new TARIC code Y129 has been introduced for the "ex" codes in Annex I of the EUDR. The code refers to the declaration of goods that do not fall within the scope of the Regulation, so-called "ex" products. Here it is necessary for the declarant to be able to indicate that the Regulation does not apply to the import, even if the declared product is assigned to a nomenclature code covered by the EUDR.

To clarify:

The "ex" before the goods tariff code identifies a product as an extract from a group of products with identical numbers. For example, the tariff code 9401 refers to seating furniture, including those made of different materials, but only furniture made of wood is subject to the specific requirements of the regulation.

The TARIC code Y132 refers specifically to Art. 1 para. 2 EUDR. It states that the provisions of the EUDR do not apply to the relevant products listed in Annex I if they were manufactured before the date specified in Art. 38 (1) EUDR, i.e. before the period of validity of the EUDR.

TARIC code Y133 defines an exemption in accordance with the second paragraph of Annex I of the EUDR, according to which the Regulation does not apply to goods made entirely of materials whose life cycle has been completed. These products are considered recycled.

The TARIC code Y141 is used to indicate the transitional arrangement in accordance with Article 38 EUDR in the customs declaration. After the adjustment at the end of 2025, the date of application will be December 30, 2026 for large and medium-sized companies, while market participants who were established as micro or small enterprises on December 31, 2024 (size classification according to the Accounting Directive 2013/34/EU) will only be subject to the central EUDR obligations from June 30, 2027. For this group, this also postpones the date from which EUDR-specific evidence and references are expected in the customs process. Important restriction: This simplification does not apply to products that were already covered by the Annex to the EU Timber Regulation (EUTR, Regulation 995/2010) - the EUDR obligations will continue to apply here from December 30, 2026. Y141 should therefore always be checked in connection with the specific product, your own role and the current TARIC status.

The TARIC code Y142 is used in customs declarations if the transaction does not take place as part of a commercial activity - for example, in the case of purely private imports by natural persons (consumer-to-consumer constellations). The EU Commission clarifies in FAQ 3.16 that products that are exclusively for private use or private consumption in the customs territory of the Union do not fall within the scope of the EUDR. Examples: a travel souvenir in normal household quantities or a parcel between private individuals from a third country.

The Combined Nomenclature (CN) and TARIC are seamlessly integrated into the EUDR to ensure a clear classification of products that may contribute to deforestation. This codification not only facilitates the administrative process, but is also an indispensable tool for companies engaged in international trade. With its help, companies can precisely determine whether their goods meet the requirements of the regulation and what regulatory steps are required to ensure compliance.

These codes play a central role in risk analysis and the preparation of due diligence declarations. By precisely categorizing products, companies are able to more effectively identify potential risks in their supply chains and implement appropriate risk mitigation measures. The ability to successfully identify and apply the relevant codes for their products is therefore an essential part of the strategic planning and implementation of EUDR compliance.

Note: The correct identification and application of the CN and TARIC codes is a prerequisite for a valid risk analysis and legally compliant due diligence declaration in accordance with EUDR.

Obligation to declare raw materials and end products - What applies when?

The obligation to notify raw materials and end products is a crucial aspect of the EUDR. Above all, the question arises: if a raw material is affected by regulation, does this automatically apply to the resulting end product? The answer is complex and depends on various factors. The obligation to collect and hold reference numbers practically only affects the first downstream operator, as the transfer along the entire chain was explicitly defused at the end of 2025.

An end product becomes EUDR-relevant if it fulfills certain criteria. These include the CN heading, the level of processing and the ex designation of the product. The CN heading, also known as the Combined Nomenclature, is an important factor as it regulates the classification of goods in international trade and helps to determine the regulatory requirements. The level of processing and the ex designation also provide information on the extent to which a product is affected by regulation.

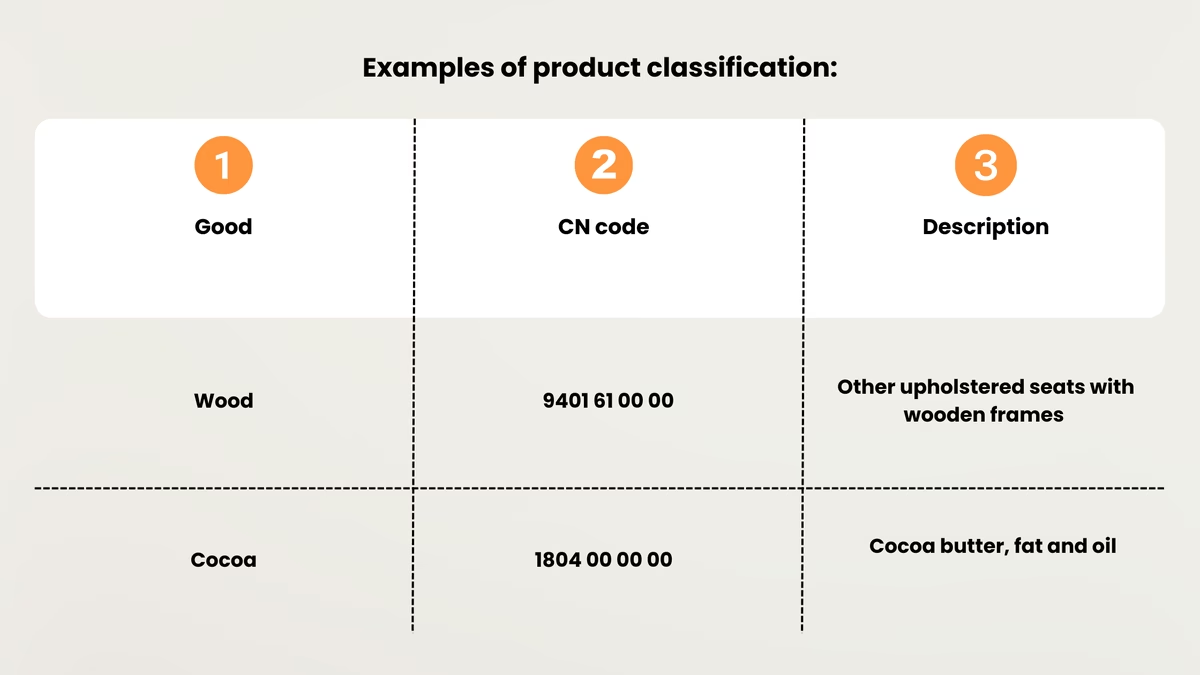

Examples of product classifications are helpful to illustrate this.

Step 1: View Annex I of the EUDR

✔️ The table in Annex I lists the goods according to their classification in the Combined Nomenclature.

Step 2: Determine the CN heading

✔️ Determine the CN codes for the goods concerned in TARIC. For example, Chapter 44 concerns wood and wood products.

Step 3: Check Annex I for ex code in the corresponding category

✔️ Check Annex I for relevant raw material and relevant products. The ex codes must be observed. Example: Tariff code ex9401 includes seating furniture made of different materials, whereby only the wood products are subject to the specific requirements of the EUDR.

Planned changes to the product scope: Delegated act 2026

The EU Commission is authorized under Article 34(1) EUDR to amend Annex I via delegated acts. The current draft (as of May 2026) is subject to public consultation until June 1, 2026 and is only binding upon publication in the Official Journal. As the entry into force will take effect directly on the day after publication without a transition period, companies should proactively prepare their HS code mappings, DDS templates and supplier communication now.

Substantial scope changes at a glance:

- Inclusion: frozen bovine tongues (ex 0206 21 00), soluble coffee (2101 11 00) and additional palm oil derivatives from oleochemistry (including various alcohols, fatty acids, soap bars and flakes).

- Deletion: Hides, skins and leather of bovine animals (ex 4101, ex 4104, ex 4107) - Reason: low economic leverage of EU actors on upstream suppliers, separate value chains compared to meat.

- Cattle adjustment: ex 0102 replaces 0102 21 / 0102 29 - one collective code, editorial, no scope change.

- Adjustment rubber: ex 4012 90 30 instead of ex 4012 - EUDR obligations for retreaded tires will in future be limited to the new rubber tread, the carcass casing will be removed from the scope.

- Clarification of the "ex" codes for oil palm and rubber: Only products that were actually manufactured from the relevant raw material are included.

There are also technical clarifications, including on waste, used and second-hand products and their components, sample and test products, non-wooden and reusable packaging, marketing and information material and correspondence within the meaning of Regulation (EU) 2015/2446.

Recommendation: Mark the planned codes internally as "expected" and monitor the Commission's FAQ updates and guidance documents. Anyone who is already affected by soluble coffee, frozen beef tongues, palm oil oleochemicals or retreaded tires - or who needs to check whether leather products fall outside their own scope - should actively use the consultation phase to prepare.

Mandatory information in the customs declaration: How the codes come together

In practice, compliance is often decided directly at customs. Certain information must be included in the customs declaration for the import or export of EUDR-relevant goods - otherwise the goods will not be released. The prerequisite is that the DDS (or, if applicable, the SD) has been submitted in the EU information system before the customs declaration is submitted and the reference number has been received.

This mandatory information must be included in the application:

- Customs tariff number (incl. TARIC): The ten-digit EU customs tariff number on HS/CN basis, supplemented by TARIC.

- Quantity: in kilograms net weight (without packaging), plus additional unit if applicable.

- Document coding (TARIC document code): indicates to customs that the EUDR requirement has been met (e.g. C716 for "Due diligence declaration available", C717 for SME exemption in accordance with Art. 4(8) EUDR).

- Document number = DDS reference number: The reference number from the EU information system is specified as the document number. Several DDS reference numbers can be combined in one customs declaration.

- Y-codes, if applicable: for exemptions and simplifications (SME constellations, transitional periods, "ex" HS codes from Annex I or products made from recycled material).

What HS code depth must be specified in the DDS?

When creating the DDS or SD, the HS code must be specified to at least the digit level listed in Annex I (FAQ 7.24). It can be extended by up to six digits on a voluntary basis. Example: HS 1201 (soybeans) can be selected; subheadings 1201 10 (seeds) or 1201 90 (other) can be added voluntarily. If Annex I already lists six positions, the declarant cannot switch to a shorter depth.

Special cases:

- Re-import: The conventional reference number 99EU999999999999 can be used instead of a separate DDS for products that were demonstrably previously placed on the EU market and exported. Customs documents, contracts, delivery bills, CMR, Bill of Lading, Air-Way-Bill or invoices can be used as proof.

- Export by a downstream operator: The DDS reference number is omitted here; a dedicated TARIC certificate code is used instead.

Important: The goods will only be released if the coding is complete, including the reference number. If any information is missing, the import or export cannot be processed.

Practical implementation for companies

Companies involved in international trade face the challenge of using correct and up-to-date HS (Harmonized System) and TARIC (Integrated Tariff of the European Communities) codes. Accurate classification of goods is essential to fulfill customs obligations and avoid potential legal risks. Regularly checking and updating these codes within the company is therefore of great importance.

Cooperation between the customs department, purchasing and product management plays a central role here. An effective internal exchange ensures that all relevant departments are always up to date and work together on the correct classification of goods. This not only prevents delays in the operational process, but also promotes compliance with legal regulations.

In order to manage the complexity of tariff classification effectively, companies should ensure that their goods are classified correctly. The use of practical instructions and digital aids such as the EU customs tariff database (TARIC) and EZT-Online is recommended for this purpose. These tools enable precise and efficient classification and help companies to achieve their compliance goals in the long term.

Tips for implementation:

- Check HS and TARIC codes regularly to ensure they are up to date and correct

- Ensure cross-departmental cooperation between customs, purchasing and product management

- Actively use digital tools such as the EU customs tariff database (TARIC) and EZT-Online

- Document and standardize internal processes for classifying goods

Conclusion

Commodity codes are the basis for EUDR-compliant, transparent supply chains and compliance with legal requirements. Incorrect classification can result in significant regulatory risks - from delayed customs clearance to import and export bans.

Companies should keep an eye on three points in particular in 2026: Firstly, the upcoming Delegated Act with its inclusions (soluble coffee, frozen bovine tongues, palm oil derivatives), deletions (hides, skins, leather) and clarifications of "ex" codes. Secondly, the correct application of TARIC document and Y codes in the customs declaration, including re-import constellations with the conventional reference number 99EU999999999999. Thirdly, the question of whether processing steps in your own company change the Annex I-relevant positions of the goods code - only then does your own role shift from trader to downstream operator.

Establishing a structured process for regularly reviewing and updating HS, CN and TARIC codes and fully documenting all changes creates the basis for internal audits, transparent reporting and legally compliant due diligence declarations.

Frequently asked questions

The HS Code (Harmonized System) is an international classification method with six digits that is used worldwide for the systematic classification of goods. Within the EU, two digits are added to the Combined Nomenclature (eight digits). The TARIC code adds two further digits to reflect EU-specific trade protection measures such as customs duties or restrictions. An eleventh digit can include national special features or regulations.

The HS and TARIC codes are crucial for the implementation of the EU regulation to prevent deforestation (EUDR), as they identify the product groups covered by the regulation. The mandatory HS code list of all raw materials and products subject to EUDR can be found in Annex I of the regulation - from cocoa beans and chocolate to furniture, tires and paper. Companies can use this HS code list to clearly check whether a product falls within the scope of the EUDR. New TARIC codes such as C716 and C717 also help to monitor compliance with due diligence obligations and ensure that affected products meet the EUDR requirements.

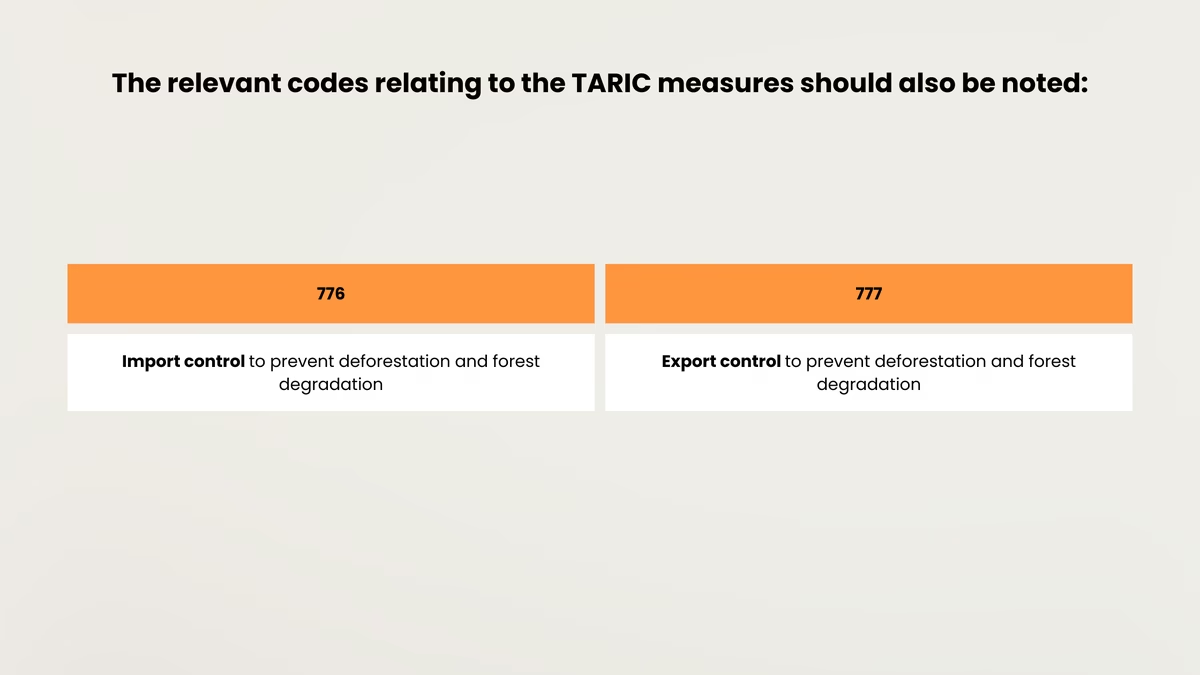

The TARIC code is crucial for import control, as it indicates specific measures such as customs duties and import restrictions. Codes 776 and 777 in the TARIC system are relevant, for example, for import and export controls to prevent deforestation and forest degradation.

C-codes in the TARIC system are relevant for the due diligence declaration of products, while Y-codes document specific exceptions, such as for recycled goods or special SME regulations. These codes help companies and customs authorities to act in accordance with EU regulations and ensure compliance.

The obligation to declare depends on the classification of the products according to the Combined Nomenclature (CN). Raw materials and resulting finished products are subject to EUDR if they fulfill the specific criteria of the regulation, which relate to the CN heading, the depth of processing and the ex designation. Companies must check the relevant product specifications to ensure their EUDR compliance.

Companies should regularly review and update their commodity codes to comply with customs requirements for international shipping and minimize legal risks. Close cooperation between the customs department, purchasing and product management is crucial. Online tools such as the EU Customs Tariff Database (TARIC) and EZT-Online can assist with correct classification and facilitate compliance with EUDR.

The correct use of commodity codes is essential for EUDR compliance. Companies should proactively implement structured processes to regularly review and update classifications. In addition, a comprehensive documentation system promotes transparency and traceability, which is helpful in meeting regulatory requirements. Companies should ensure that their internal systems and processes are regularly reviewed and adapted to new regulatory requirements.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.