Important facts

- Are used goods generally affected by the EUDR?

- No, anyone who resells, leases or exports goods that were already legally marketed in the EU before June 29, 2023 does not have to carry out a new EUDR test.

- When can used goods still be subject to EUDR?

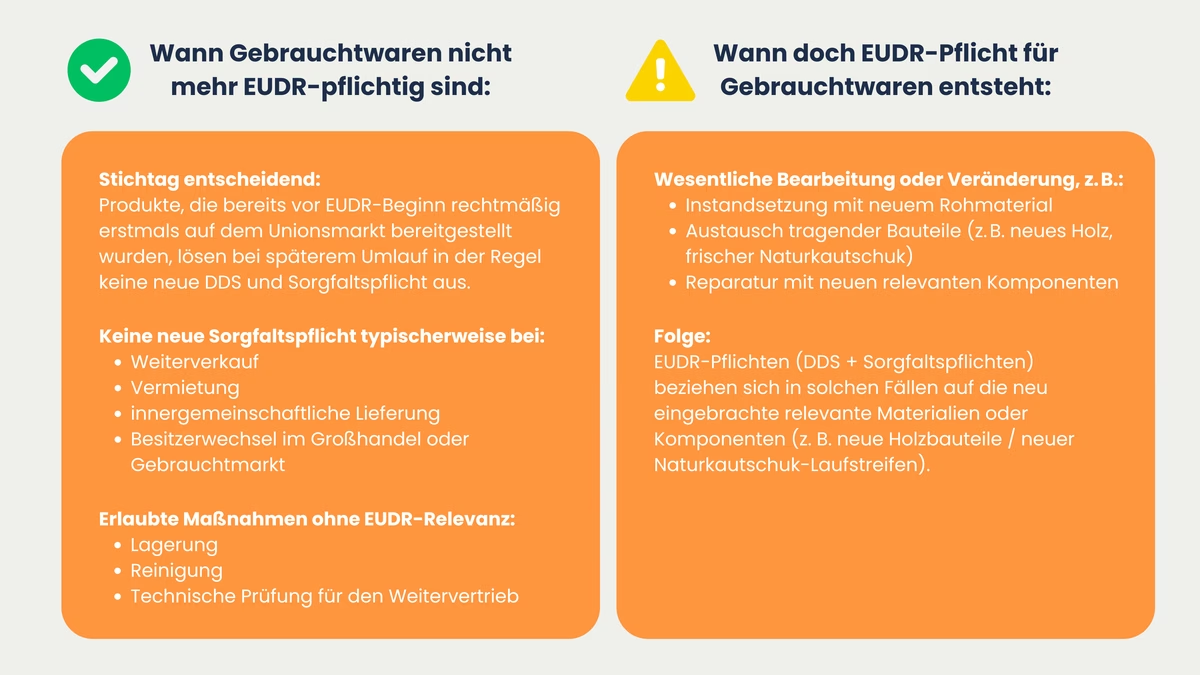

- As soon as it is significantly modified, for example with new wooden parts on pallets or new natural rubber for retreads, it is considered a new product and is again subject to due diligence.

- What is considered a "significant change"?

- This does not include minor repairs or cleaning, but it does include extensive conversions or upcycling that fundamentally change the material composition or function.

- What documentation is useful for used goods?

- Proof of purchase date, origin, serial numbers and maintenance history are recommended in order to be able to fully document the used status.

- Do exports of used goods outside the EU have to be checked?

- No, provided the goods have not been significantly modified, no new EUDR inspection is required for export.

- What should companies bear in mind when dealing with used EUDR-relevant products?

- Clear labeling of the used status and transparent communication along the supply chain, in invoices, delivery bills or digital systems are crucial.

Executive Summary

The EUDR obliges companies to prove the legal and deforestation-free origin of certain raw materials before products made from them are placed on the EU internal market for the first time. A distinction must be made between market participants and downstream traders: The latter do not submit a due diligence declaration, but must provide certain information. Non-SMEs are also obliged to register in the EU information system.

In principle, the EUDR does not apply to used goods if they were already lawfully made available on the Union market before the respective date of application. The prerequisite for this is that they have not been significantly modified since then. A significant change occurs when new EUDR-relevant material is introduced, for example when replacing load-bearing wooden elements on pallets or when retreading tires with fresh natural rubber. In such cases, the EUDR obligations relate to the newly added components.

Companies should therefore ensure proper documentation of the product origin and record reference numbers of due diligence declarations. Clear labelling of new and used goods along the supply chain effectively minimizes regulatory risks.

What does the EUDR say about second-hand goods?

Trade in used goods has a long tradition in Europe and is becoming increasingly important due to the scarcity of resources and sustainability goals. Products such as tires, containers or transport pallets in particular regularly go through several usage cycles. Uncertainty is now arising in the wake of the EUDR: Does the same duty of care apply to any resale or export of a used good as to new goods? Many companies are confronted with inventories for which only incomplete prior information is available, especially if products entered the EU years ago.

This uncertainty is omnipresent in the supply chain. On the one hand, there is often a lack of transparency as to when exactly a product was "placed on the market" for the first time. On the other hand, there are many different constellations in practice: Products are repaired, refurbished or supplemented with new parts and then resold. While the regulation primarily addresses the direct origin of raw materials, the question arises as to whether and when used goods are considered "new" products within the meaning of the EUDR.

Focus of the regulation: avoiding deforestation through primary raw materials

The aim of the Deforestation Regulation ( EUDR for short) is to keep products with a risk of deforestation and forest degradation out of the European internal market as far as possible. This includes not only raw materials such as soya, coffee, palm oil, cattle and wood, but also products made from them, such as furniture, paper products and tires made from natural rubber.

Essentially, the regulation requires that only deforestation-free products may be placed on the market, sold or exported within the EU. Companies must rely on verifiable evidence to prove that their products are deforestation-free.

As a rule, companies are obliged to carry out a comprehensive due diligence and risk analysis. This includes the traceability of the origin of raw materials, compliance with local laws and the submission of due diligence declarations as well as the submission of comprehensive verification documents. The due diligence obligation applies in principle both to new products and to processed or composite articles that are associated with the relevant products if they are placed on the Union market for the first time.

"Placing on the market" within the meaning of the EUDR

A central element of the EUDR is the term "placing on the market". According to the content of Article 2 No. 16 of the Regulation, this means: "any making available for the first time on the Union market of a relevant product for distribution or use." The decisive factor is therefore when a product, be it a raw material, an individual part or a finished product, is made available on the market for the first time within the scope of the Regulation. If a product was already imported in compliance with the law before the EUDR came into force or elsewhere in the internal market, it is deemed to have been "placed on the market". Such goods do not have to be tested again. Furthermore, second-hand is only expressly excluded from the scope of application if the product has completed its life cycle and would otherwise be disposed of as waste.

Subsequent changes of ownership, resale, rental or storage within the EU do not generally trigger a new first making available if the product has already been lawfully placed on the market in the EU. However, if a used product is imported into the EU from a third country for the first time after the start of use, this may constitute making available for the first time.

Update legal status (Amendment Ordinance 12/2025):

The Regulation now explicitly distinguishes between market participants and downstream market participants (obligations such as traders). In principle, traders and downstream operators do not transmit DDS and do not generally have to ensure compliance with the due diligence obligation. However, non-SMEs among them must register in the EU information system and may only trade, supply or export relevant products if they comply with the prescribed information and record-keeping obligations.

When do used goods typically not trigger a new EUDR obligation?

In practice, this means that products that were placed on the market in an EU member state before the EUDR came into force (from 30.12.2026 or 30.06.2027 for micro and small enterprises) are not subject to a new EUDR test, even if they are resold, rented or exported. This applies analogously if a product changes from buyer to buyer, for example in wholesale, in the second-hand business or in cross-border trade from country to country within the EU.

The decisive factor is whether a significant processing or treatment step has taken place in the meantime. If the product is merely stored, cleaned or tested for resale, it remains a used product from an EUDR perspective. Only if new relevant materials or components are added in the course of repair or reprocessing (e.g. new wood or new natural rubber) can EUDR obligations arise for these newly introduced components. Pure cleaning, testing, sorting or resale reconditioning without new relevant components generally leaves the product with the status already placed on the market from an EUDR perspective.

Case study 1: Used tires

Why tires are generally EUDR-relevant

Tires consist to a large extent of natural rubber, which is explicitly listed as risk-relevant in Annex I of the EUDR. According to estimates by the International Rubber Study Group, the annual global production of natural rubber amounts to around 14 million tons, the majority of which is harvested in Asia. According to a study by the Vrije University of Amsterdam, five percent of the natural rubber produced worldwide is used for tires for European vehicles, primarily for car tires. As forests were deliberately cleared for many plantation areas, the EU explicitly classifies tires as subject to EUDR if they are sold in the EU for the first time.

New tire importers must therefore ensure that both the rubber material obtained and the production process can be documented as deforestation-free and legal in accordance with the EUDR. The verification requirements are considerable: in addition to proof of the country of origin, traceability to the parcel of land on which the rubber was grown is also required.

When used tires are considered "not affected"

When reselling used tires within the EU, there is generally no new initial provision if the tires have already been lawfully placed on the market in the EU. According to the Commission's clarification, the following applies to retreaded tires: EUDR obligations only apply to the newly added natural rubber components (e.g. new tread), while casings or carcasses as such are outside the scope.

The typical example: A truck fleet renews its tires after three years and sells the tires to a second-hand dealer or to other European countries. As the tires have already been imported and taxed as a new product, the goods are treated as used in every subsequent trade transaction and are no longer subject to compliance from an EUDR perspective. This exemption also applies to tires that are exported within the EU or transferred between companies as long as no further processing has taken place.

However, if a used tire is imported into the EU from a third country for the first time after the start of use, this may constitute first-time supply, in which case the obligations apply in principle.

Exceptional case: Retreaded tires

However, retreaded tires are handled differently. Here, the worn tire substructure (carcass) is reconditioned, vulcanized and provided with a new tread layer. According to the Commission's updated FAQ clarification, used carcasses and casings are generally outside the scope of application, while retreaded tires are only covered to the extent that new natural rubber components (e.g. new tread, tread) are added. Accordingly, due diligence obligations and DDS refer to these new natural rubber parts, not to the entire carcass.

The decisive factor for EUDR classification is not so much a general materiality criterion from customs law, but rather the question of whether and which new relevant natural rubber components are introduced during retreading and subsequently placed on the market as retreaded tires. In this case, the EUDR obligations apply to these new natural rubber components. If only a minor repair is carried out without significantly changing the identity of the tire, it remains to be classified as used goods. However, if extensive retreading or reconstruction is carried out, the tire is considered a new product and is therefore subject to EUDR. A detailed examination of each individual case is therefore required.

Case study 2: Used pallets

New pallets generally subject to EUDR as a wood product

Wood products play a central role in the context of the EUDR, as raw wood is a potential driver of global deforestation and is one of the relevant raw materials covered by the regulation. Transport pallets, in particular the widely used Euro pallets, are made of various types of wood and are produced, exchanged and reused in Europe by the millions. The majority of pallets circulating in the EU originate from domestic or European production. Nevertheless, some pallets from non-European sources, such as Asia or South America, are also used, which can be traced back to deliveries or disposable packaging.

The full EUDR due diligence obligation therefore applies to new pallets, regardless of whether they are exchangeable or disposable. Manufacturers and importers must prove the legal and deforestation-free origin of the wood during production by means of suitable documents and declarations before the pallets can be sold or passed on in the EU.

Note: Pallets (CN/HS 4415) are not in scope as packaging materials if they are used exclusively to carry, protect or support other goods. Pallets are particularly relevant to EUDR if they are placed on the market or exported as a separate product (e.g. empty pallets or packaging as merchandise).

Used pallets: When does the exception apply in the EU market?

Once pallets have been made available as a finished product on the EU internal market, for example by a European manufacturer or an importer, they are considered to have been placed on the market. With this introduction into the internal market, they are considered used packaging when subsequently traded, rented, exchanged or passed on within the EU and, according to the FAQ and guidance clarification, are outside the scope of application as long as they have already been used once to carry, protect or support other goods and no new relevant wood components are introduced.

This applies in particular to the widespread exchange networks such as the open Euro pallet pool, in which millions of pallets have been in circulation for decades. Customs and inspectors also recognize that no new EUDR due diligence obligation arises for pallets that have already been introduced into the economic cycle in Europe as long as no changes are made to the essential components of the pallet. This applies in particular to exchange or closed-loop systems (e.g. pallet pools): According to the Commission FAQ, empty, already used packaging in circulation is not in scope.

If a used pallet is merely cleaned, checked, marked or pooled, it continues to be traded as a component part of an existing product. However, if wooden components are replaced (e.g. board, strip), the FAQ clarification states that the EUDR obligations apply to these new wooden components. In this case, a DDS must be submitted for the repaired pallet, whereby the due diligence only covers the new wooden parts.

When pallets can be relevant after all

Repairs are EUDR-relevant if new timber components are introduced (e.g. replacement of deck or supporting boards). A DDS is then required, but the due diligence only relates to the new wood components. Pure processing without new wood parts (cleaning, sorting, marking) remains outside the scope.

In the case of upcycling, it must also be checked whether the new product even falls under a CN heading listed in Annex I; only then do EUDR obligations arise.

A detailed examination of the individual case is recommended here: If the modification is only carried out to restore the original functionality, without any substantial addition of material, it can still be legally considered a used pallet. However, if new raw materials are added on a larger scale and the product is given a new function or identity as a result of the modification, the EUDR testing obligation applies again. This creates a need for action, particularly for commercial upcycling providers.

Summary: When are second-hand goods subject to EUDR?

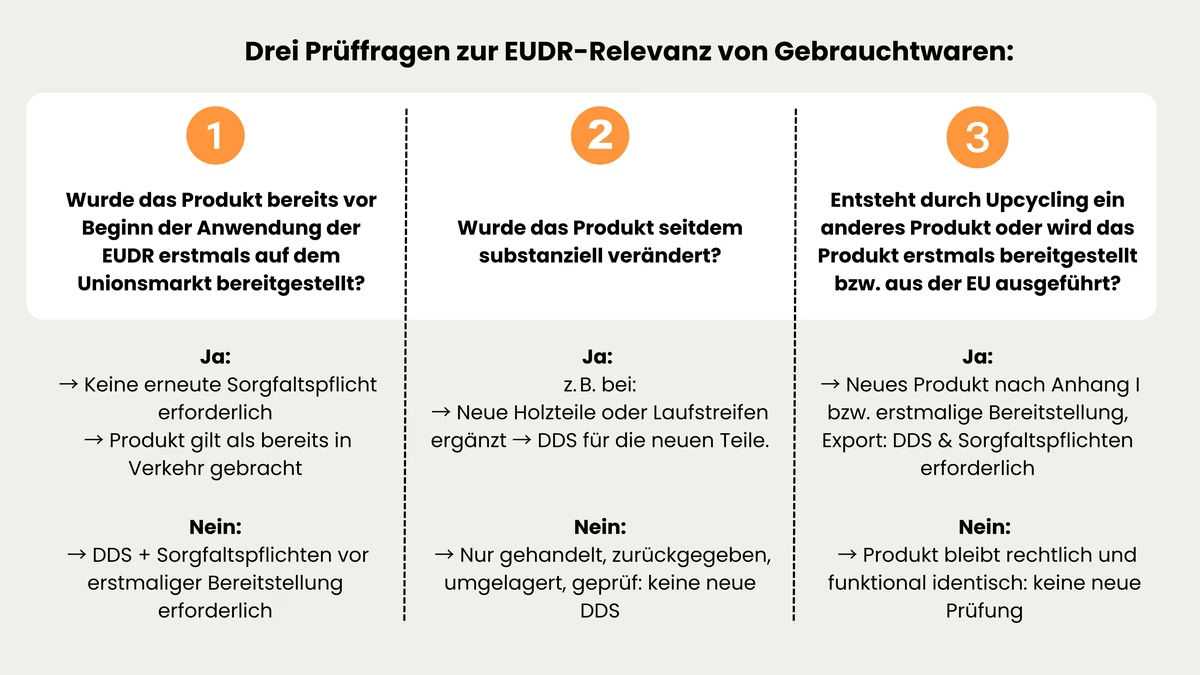

Three key questions determine whether and how the EUDR applies to second-hand goods.

Decision logic for practice

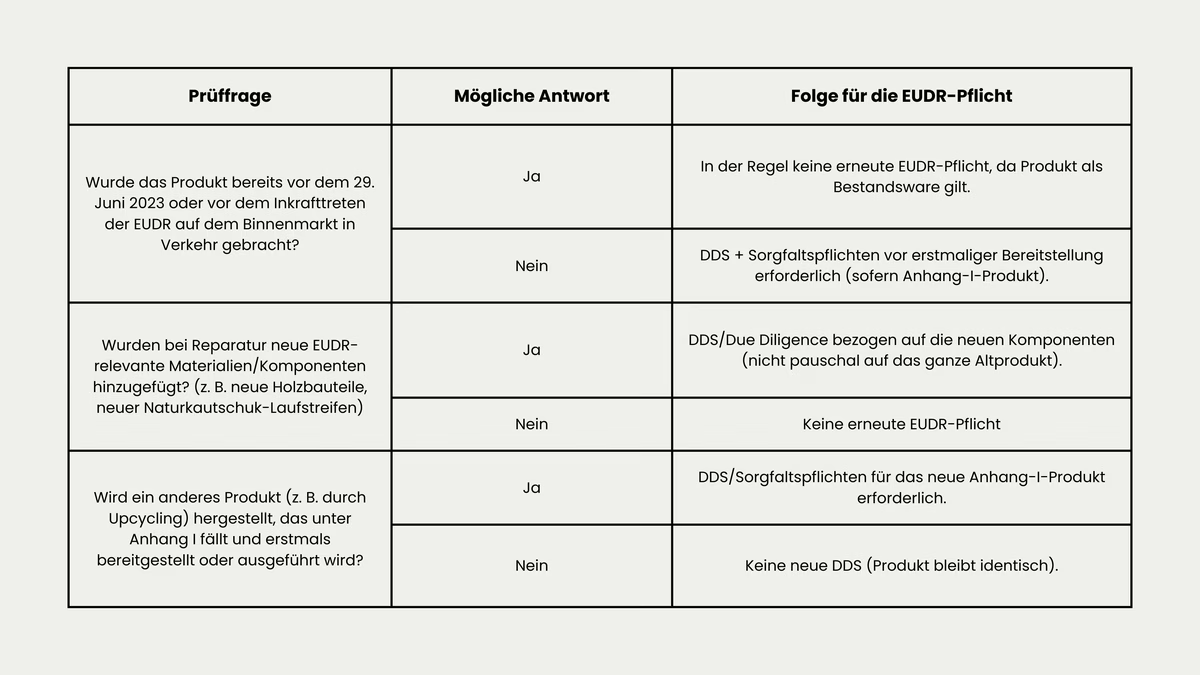

Firstly, it must be clarified whether the product concerned was already made available on the Union market for the first time before the EUDR came into force. If this is the case, there is generally no need for any new due diligence and risk assessment under the Regulation. In addition, second-hand products that have completed their life cycle and would otherwise be disposed of as waste are not subject to the EUDR obligations according to the FAQ clarification. In the case of packaging (e.g. pallets), a distinction must also be made as to whether it is used as packaging to support or protect a product (then regularly outside the scope) or is traded as an independent product.

Secondly, it must be checked whether new relevant materials have been added in the process. In this case, EUDR obligations arise in relation to these newly introduced relevant components (e.g. new wooden components for pallet repair or new natural rubber parts for retreaded tires). Pure reprocessing without new relevant materials (cleaning, testing, marking, pooling) generally remains outside the obligations.

Thirdly, it must be clarified whether the conversion/upcycling results in a different product that (i) falls under an Annex I item and (ii) is made available on the Union market or exported for the first time. In this case, the EUDR obligations regularly apply to the newly added relevant materials in the case of repairs or refurbishment.

Used goods (e.g. tires or pallets) are generally not subject to a new EUDR test if the product was already lawfully made available on the Union market before the EUDR was applied and is merely resold, rented out or kept in circulation.

It is important to note that there is no blanket exemption simply because of a production date before June 29, 2023. Rather, transitional rules apply to certain timber and timber products that were produced before June 29, 2023 and fell within the scope of the former EU Timber Regulation (EUTR): If such products are placed on the market from December 30, 2026, the classification will continue to run in principle via the EUTR regime until December 31, 2029. From December 31, 2029, they must then meet the EUDR criteria in accordance with Article 3.

In particular, no new relevant materials (e.g. new wood components or new natural rubber components) may have been introduced in the course of repair or refurbishment, otherwise obligations arise in relation to these newly added components.

Overview: Implementation checklist for companies

Recommendations for companies

Document evidence of prior use

Large, medium-sized and small companies that trade in used goods such as tires or pallets should attach importance to complete documentation of product introduction and use. It is particularly important to document the reference number of the due diligence declaration or identification number (in the case of simplified declarations). Especially where the first downstream market participant or trader takes over the goods from an upstream stage. The reference and identification numbers must be recorded for the first downstream actor, not for all of them. This collection of information includes details such as the date and proof of first purchase, the unique origin from the EU internal market, any existing serial numbers or proof of delivery, as well as descriptions of previous use and any maintenance steps. The creation of a central register in which this product information is stored has already proven its worth in practice. In this way, gaps in evidence can be minimized even years later and official inquiries can be answered quickly.

To Do:

Create a central register that fully documents the initial purchase, origin and usage history of used goods, including DDS reference numbers, for at least five years.

Strengthen communication with suppliers and customers

Clean communication along the entire supply chain is just as important. Companies should clearly indicate to suppliers and downstream business partners at an early stage whether they are dealing with new or used items. This can be done as part of invoicing, in delivery bills or technical product descriptions. In the case of EUDR-relevant processes, DDS reference numbers (verification numbers if necessary) should also be linked for each batch or transaction in the ERP and on the accompanying documents so that the chain remains traceable. Clear product identification is also useful, for example by means of barcode tags, labeling or entries in the digital merchandise management system. This is the only way to avoid queries and misunderstandings.

To Do

Clearly identify new and used goods in invoices, delivery bills and digital systems and consistently link DDS reference numbers to each relevant transaction.

Check special cases at an early stage

Borderline cases such as retreaded tires, repaired pallets with replacement boards or industrially refurbished components should be subjected to an in-depth inspection at an early stage. In particular, companies that specialize in refurbishing, upcycling or the series repair of industrial goods must clearly document which new EUDR-relevant materials or components have been introduced (e.g. new wooden components, new natural rubber treads). In such cases, the obligations are linked to these new relevant components. If in doubt, specialist or legal advice should be sought in good time. It may also be advisable to contact local authorities or customs if there is uncertainty about the classification of individual production steps.

To Do

When repairing, retreading or upcycling, document exactly which new EUDR-relevant materials have been used and, if in doubt, seek legal or official advice at an early stage.

How do I find the right EUDR tool?

Conclusion

Used goods such as tires or pallets generally do not trigger a new EUDR due diligence obligation as long as they have already been lawfully made available on the Union market and are not significantly modified. However, if new EUDR-relevant materials are introduced, the requirements are linked to these new components.

Clear product and process classification, complete documentation and the linking of relevant processes with the DDS reference number for at least five years are crucial for legal certainty. Compliance officers should set up their processes in such a way that EUDR-relevant processes are identified at an early stage and evidence can be retrieved at any time.

Frequently asked questions

Significant changes are defined as processing steps that change the fundamental identity of the product, for example by adding new raw materials (e.g. new wood for pallets or fresh rubber for tires) or converting to a different product type. As a rule, this does not include mere cleaning or maintenance.

No, a minor repair, such as repairing minor damage without using new raw material, does not change the status of the tire. It remains exempt from the EUDR as used goods. A complete retread, on the other hand, may require a new assessment in individual cases.

No, used goods that have already been placed on the market within the EU can generally be exported without a new EUDR test as long as they have not been significantly modified or reassembled since then. When exporting, the reference/identification numbers must always be provided to the customs authorities. However, this does not apply to exports by downstream market participants.

Careful documentation of previous use, precise classification of used products and transparent communication along the supply chain can largely prevent unwanted compliance risks.

Yes, the greater the proportion of new, EUDR-relevant material in the remanufacturing of a product, the more likely it is to be classified as a new product and therefore subject to EUDR. Used products without substantial material additions are generally exempt.

Karim Boukaouche

LinkedInESG-Compliance Experte · lawcode GmbH

Karim Boukaouche berät Unternehmen bei der Umsetzung der EU-Entwaldungsverordnung (EUDR) und begleitet die Implementierung digitaler Lösungen für rechtssichere Lieferketten. Seine Fachbeiträge auf dem lawcode Blog verbinden regulatorische Tiefe mit praxisnahen Handlungsempfehlungen.