The most important facts

The regulation is intended to reduce bureaucracy, ease the burden on companies and at the same time secure the sustainability goals of the Green Deal.

It brings higher thresholds, postponed deadlines and simplified requirements in all four areas.

Large companies remain the main addressees of the detailed obligations, while medium-sized companies and SMEs benefit from reduced data depth and longer transition periods.

Important are the start dates from 2024 for large companies, the postponed sector-specific ESRS from 2026 and opt-out rules for SMEs until 2028.

They should use the time to build up their data architecture, anchor dual materiality and closely link ESG processes with management and controlling.

Executive Summary

The EU Omnibus Regulation brings far-reaching changes to sustainability reporting in Europe. The focus is on raising the threshold values, which will reduce the burden on medium-sized companies in particular, as well as postponing key deadlines, such as for sector-specific ESRS and third-country reports. Large, capital market-oriented companies remain the main addressees of detailed CSRD and taxonomy obligations, while SMEs can make use of simplified standards and longer transitional arrangements. The Corporate Due Diligence Directive (CSDDD) and the Carbon Border Adjustment Mechanism (CBAM) will also be administratively streamlined by focusing requirements more on large market players and introducing default values and safe harbor rules. For German companies, the actual relief will depend on how the requirements are implemented in the German Commercial Code and national accompanying regulations. However, one thing is clear: the Omnibus Regulation does not mean a move away from ESG, but rather buys time to professionally set up data architectures, internal control systems and reporting processes. With tools such as EMAS, the DNK platform and the Sustainability Reporting Navigator, companies can structure their reporting efficiently, meet audit requirements and at the same time realize operational benefits such as cost reductions and greater transparency.

EU Omnibus at a glance: Effects on companies and the economy

The Omnibus Regulation bundles a series of selective amendments to existing legal acts and regulations. The EU Commission's aims are to reduce bureaucracy and make things easier for companies. The focus is on three signals:

- Increase in relevant size categories for the classification of companies,

- the equalization of schedules in sustainability reporting and

- proportional requirements along the size of the company.

The combination of these elements reduces the complexity of reporting in the short term without abandoning the long-term objectives of the EU Green Deal. Medium-sized companies in particular, which are building up their reporting and due diligence obligations with limited resources, gain time and room for maneuver, but should not postpone the strategic development of robust sustainability management.

Fewer reporting obligations due to higher thresholds

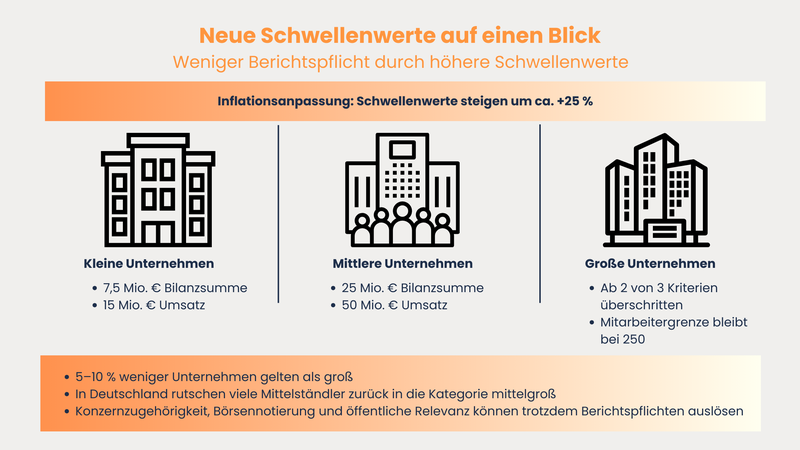

A core element of the Omnibus Regulation is the adjustment of the thresholds in the EU Accounting Directive. This defines which companies are considered small, medium-sized or large - and therefore whether they fall within the scope of additional reporting obligations such as the CSRD (Sustainability Reporting Directive). The inflation adjustment generally increases the balance sheet total and turnover thresholds by around a quarter. Specifically, the thresholds for small companies will rise to around 7.5 million euros in total assets and 15 million euros in net turnover, and for medium-sized companies to around 25 million euros in total assets and 50 million euros in net turnover. The employee limit of 250, on the other hand, is to remain unchanged. Large companies are those that exceed at least two of these three criteria. This increase means that, depending on the member state, an estimated five to ten percent fewer companies will be considered large and therefore formally fall under the obligation for comprehensive sustainability reports in accordance with the CSRD. For Germany, this means that Some of the medium-sized companies previously classified as "just under large" will slip back into the medium-sized category and should be able to benefit from simplified obligations. However, it is important to note that group affiliation, stock market listing and public relevance can continue to trigger obligations independently of the threshold values of an individual company.

Postponed deadlines for implementation

The Omnibus Regulation gives companies one thing above all: more time. Important dates for the introduction of individual reporting obligations have been postponed. For example, the sector-specific ESRS standards will not apply until 2026. Third-country reporting in accordance with Article 40 CSRD, which affects non-European parent companies with extensive activities in the EU, will also take effect two years later than originally planned. Although the start date for listed small and medium-sized enterprises remains the same for financial years from 2026 onwards, they can practically use the opt-out until 2028 - by which time there will also be more tools and tried-and-tested processes. The postponements are not a "carte blanche", but rather a breather: companies should use them to set up their data and IT systems and prepare internal processes for audit-proof reporting.

Differences according to company size

The Omnibus Regulation adapts the reporting obligations more closely to the size of companies. Large, capital market-oriented companies remain the main addressees of comprehensive sustainability reports - including detailed key figures and, in future, industry-specific requirements. Medium-sized companies below the new thresholds, on the other hand, will benefit from less detail, additional options and longer transition periods. For listed SMEs, there are simplified ESRS standards that are closer to existing management information and are intended to reduce the effort involved in data collection, particularly in the supply chain. Overall, the requirements should be better suited to the performance and organization of companies. For group parent companies, however, the challenge remains: Anyone who is required to report at group level will still need data from all subsidiaries in the future - even if individual units benefit from simplifications.

Background: Why the EU is making adjustments

The Omnibus Regulation does not represent a step backwards in terms of sustainability targets, but is intended to make implementation more realistic. There are three reasons why the readjustment is necessary: firstly, the large number of parallel regulations, secondly, the economic slowdown with increasing cost pressure in many sectors and thirdly, feedback from the field that the tight timing of the requirements is leading to bottlenecks in data compilation and audits. It has also become clear at EU level: If you want to survive in the global competition for green lead markets, you not only need ambitious targets, but also leaner procedures to keep investments in Europe.

From the CSRD to the Omnibus Directive

With the CSRD, the EU fundamentally modernized the rules of sustainability reporting in 2022. Instead of voluntary frameworks, binding ESRS standards, assurance obligations and digital tagging requirements now apply. In terms of implementation, however, this reform clashed with other major projects such as taxonomy, CBAM, supply chain guidelines and the introduction of European data rooms. The European Commission's omnibus regulation responds to this by selectively adapting and coordinating several pieces of legislation in order to give companies planning security and reduce duplication of effort. The Commission's proposal is a "technical" directive with a strategic effect: it does not change the requirement for transparency, but it does change the timing and depth of the individual steps.

Goal: Less bureaucracy, more competitiveness and simplification

The draft omnibus regulation aims to ease the burden on companies without abandoning the sustainability goals for climate, biodiversity or human rights. The background to this is that starting too quickly would force over 50,000 companies to comply with complex reporting obligations at the same time - while there is still a lack of auditors, data interfaces and industry-specific guidelines. The regulation therefore postpones certain requirements, allows default values and creates transitional rules ("safe harbor"). The EU taxonomy and CBAM are also to be more closely aligned with the principle of proportionality. The idea behind this: Companies should invest their resources in genuine sustainability projects such as decarbonization, the circular economy and transparent supply chains - instead of putting them into reports that currently offer little added value.

The political decision-making process

The omnibus proposal was supported by all major political forces - with the realization that the Green Deal would lose its impact without pragmatic adjustments. The Council, Parliament and Commission negotiated the changes together in trilogue. National particularities were taken into account, for example different company structures or inspection systems. In the end, they agreed on clear key points: higher thresholds (due to inflation), postponed deadlines for the CSRD and more proportionality for taxonomy and CBAM obligations. For companies, this means that the omnibus rules have broad political support and will provide a reliable basis for planning in the coming years. However, the proposal still needs to be transposed into national law.

Core elements of the reform

The EU omnibus entails three main changes: it specifies the requirements of the CSRD, it limits the scope of application of the EU taxonomy and it simplifies individual obligations in the areas of supply chain and carbon border adjustment. For companies, it is not so much the detailed legal framework that is decisive, but the practical question: what data must be available, when and in what depth, and what audit or liability risk does this entail?

CSRD: New rules for reports and standards

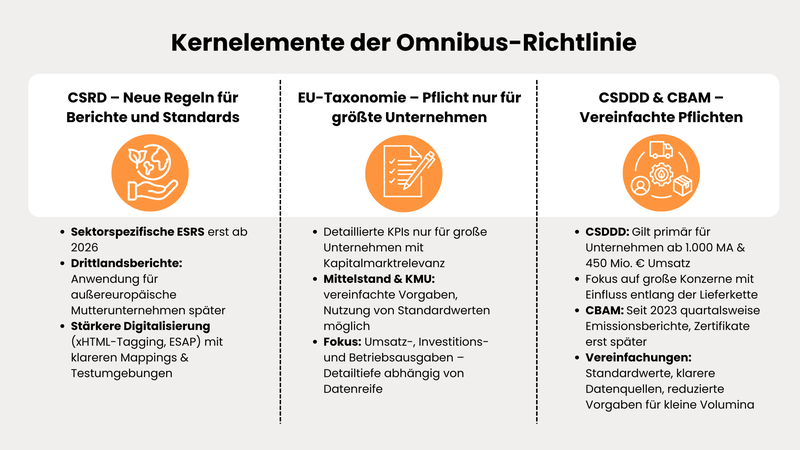

Within the framework of the Omnibus Regulation, three points are crucial for the CSRD. Firstly, the regulation postpones the deadline for sector-specific ESRS to June 30, 2026, giving companies in particularly high-emission or high-risk sectors, such as cement, chemicals or financial services, two additional reporting cycles to prepare sector-specific KPIs, taxonomies and processes. Secondly, the reform facilitates third-country reporting by extending the application period for non-European parent companies with an EU subsidiary presence. Thirdly, it strengthens the digitalization of reports without throwing companies in at the deep end: Mandatory tagging in xHTML format and submission via the European Single Access Point remain targets, but are technically accompanied by clearer mappings and test environments. This allows companies to professionalize the dual materiality analysis, the internal control system for sustainability data and the external audit step by step instead of implementing everything at the same time and under great time pressure. EFRAG's Datapoint List and the ESRS implementation material remain the authoritative references. However, using the information will be easier because there will be more time for data quality, consolidation logic and interfaces to financial reporting.

EU taxonomy: mandatory only for the largest companies

The EU taxonomy remains a key instrument for channeling capital flows into sustainable projects. However, the Omnibus Regulation defines the user group more specifically and simplifies reporting. In future, the taxonomy will only apply to smaller companies with fewer than 1,000 employees and a turnover of less than 450 million euros on a voluntary basis. Companies that employ more than 1,000 people but remain below the turnover threshold only have to disclose turnover and investment figures (CapEx), while operating expenses (OpEx) remain optional. However, companies that exceed both thresholds - more than 1,000 employees and more than 450 million euros in turnover - are subject to full reporting requirements. They must publish all taxonomy key figures; they can only waive disclosure of the OpEx KPI if the proportion of taxonomy-eligible turnover is less than 25% of total turnover.

In addition, reporting will be simplified by new materiality thresholds. In future, activities that affect less than ten percent of the relevant financial indicators will be considered immaterial and therefore do not have to be assessed in detail. At the same time, a public consultation on the revision of the taxonomy reporting will run until March 26, 2025, which is intended to bring further practical simplifications. This will focus the taxonomy more strongly on large and relevant market players and at the same time improve the quality of the disclosures without overburdening SMEs with detailed requirements.

CSDDD and CBAM: Simplification of due diligence obligations, supply chain directive and border adjustment

The Omnibus Regulation also amended the Corporate Due Diligence Directive(CSDDD) and streamlined key points. In future, its scope of application will be aimed primarily at large companies with more than 1,000 employees and an annual turnover of over 450 million euros. The focus will be more on direct business partners in the supply chain: in future, companies will only have to systematically analyze sustainability risks for their direct suppliers. For more distant stages in the value chain, extended obligations only apply if there are plausible indications of risks - such as media reports, NGO research or other reliable evidence. Nevertheless, it remains the responsibility of companies to anchor theircode of conduct along the entire value chain.

The Omnibus Regulation also makes things easier in terms of time. Instead of an annual review of the measures implemented, companies will only have to evaluate their due diligence obligations every five years in future. In addition, Europe-wide liability for infringements has been weakened, significantly reducing the risk of widespread legal action. Finally, the initial application of the CSDDD has also been postponed by one year: the new obligations will now take effect for the first time on July 26, 2028. The EU is thus targeting the CSDDD more specifically at those companies that have sufficient resources and influence to enforce effective standards - and at the same time reducing the bureaucratic burden for companies that were previously overwhelmed by the breadth and depth of the due diligence obligations.

Simplifications have also been made to the carbon border adjustment mechanism (CBAM). Since October 2023, importers of affected goods have had to report emissions on a quarterly basis, but do not yet have to purchase certificates. The EU Commission's Omnibus Regulation makes this easier by allowing standard values, specifying data sources and allowing smaller import volumes to benefit from simplified rules. This reduces the bureaucratic burden during the transitional phase until the subsequent financial pricing. For industry, this creates more planning security: companies can prepare investments in climate-friendly materials and processes without time-consuming reporting obligations blocking their scarce specialist resources.

Germany: Focus on national implementation

For German companies, the decisive factor will be how the omnibus requirements are transposed into national law. Although the EU omnibus has been adopted at European level, the actual relief effect depends on how the German CSRD Implementation Act, the auditing standards and the IT systems for data exchange within groups and with auditors are designed. National regulations such as the Supply Chain Due Diligence Act (LkSG ) also play an important role, as they are closely interlinked with the European requirements.

Stop-the-Clock Directive and its consequences

In Germany, the term "stop-the-clock" has become established for the postponement of deadlines in the CSRD environment. This refers to the targeted extension of individual deadlines - such as for sector-specific ESRS or third-country reports - so that companies are not overloaded right from the start. In practical terms, this means that companies that start CSRD reporting from the 2024 financial year do not have to submit any additional sector-specific information for the time being.

The audit market also benefits: There is more time to build up capacity for the mandatory audit with limited assurance before a decision is made later on whether to expand the scope of the audit. For groups with parent companies in the US or the UK, the pressure to coordinate is also reduced, as the transition periods make it easier to align with SEC or TPT standards. "Stop-the-clock" therefore does not mean a standstill, but a deliberate pause for breath so that reports, audits and digital systems can interact reliably step by step.

Open questions regarding CSRD implementation

Despite the relief provided by the Omnibus Regulation, important detailed issues remain unresolved. These include, for example:

- How are thresholds audited in international groups with different accounting standards

- Should the sustainability report be a separate section of the management report or a separate document with the same audit scope?

- What exactly will the EU-wide digital taxonomy for ESRS tagging look like, and what penalties will there be for late or incomplete submission?

In Germany, companies are also discussing how to divide responsibility between the sustainability, finance and legal departments in order to embed dual materiality in strategies, key figures and incentive systems. Although the Omnibus Regulation provides more time and sets priorities, it does not replace the need to establish clear responsibilities, robust processes and reliable data quality that also stands up to scrutiny.

Significance for German companies and SMEs

The Omnibus Regulation makes things noticeably easier for German SMEs, but by no means does it mean an exit from ESG issues. National requirements such as the Supply Chain Duty of Care Act remain in place. In addition, investors are increasingly demanding comprehensible climate strategies and customers are increasingly including ESG criteria in tenders. If you want to remain competitive in the long term, you cannot escape these developments.

However, the postponements within the framework of the omnibus create a valuable time buffer. Companies can use it to structure their sustainability and financial data properly and set up their reporting efficiently. This includes, for example:

- Master data maintenance and chart of accounts mapping to consistently record taxonomy key figures.

- Automated emissions calculations in Scope 1-3 that can be integrated into existing systems.

- Interlocking with risk management and the internal control system (ICS) so that sustainability issues are embedded in overall management.

Professional reporting not only brings compliance, but also tangible efficiency gains. Energy and material flow costs can be significantly reduced through systematic analyses - for example within the framework of EMAS or ISO management systems. At the same time, data quality increases, which not only makes external auditing easier, but also creates the basis for better decisions within the company. Particularly in Germany, where high energy prices are a structural competitive issue, ESG is becoming a real location factor: those who use the new scope wisely now will strengthen their resilience, reduce costs and gain a head start with customers and investors.

Practical help for reporting

The Omnibus Directive changes the obligations, but it does not make the substantive task any smaller: identify key issues, manage objectives and measures credibly, provide robust evidence of progress, make risks transparent. Three tools and principles are particularly useful in practice.

EMAS, the EU's environmental management and audit system, is more than just a label. It provides a structured, audited basis and support for environmental data that can be reused in the CSRD logic. Those who already continuously collect key figures on energy, emissions, waste, water and compliance issues and have them audited externally can continue to use them in ESRS E1 to E5 in many cases. EMAS also requires regular environmental audits and the involvement of employees, which increases data quality and organizational awareness. In practice, it has been shown that companies with EMAS or ISO 14001 make reliable Scope 1 and Scope 2 emissions data available much more quickly and set up model-based methods for Scope 3 in a coherent manner. This reduces redundant data collection, especially in corporate groups, and makes external auditing easier because established audit trails exist. In combination with energy and CO2 management systems, this allows decarbonization measures to be set up with planning and investment certainty, which in turn has a positive impact on the taxonomy conformity of capex projects.

The platform of the German Sustainability Code (GSC ) offers companies a practical way of establishing their reporting structures, documenting content consistently and creating transparency for external stakeholders. Even though the CSRD sets its own standards, the DNK is particularly helpful for companies that want to report systematically for the first time and create a foundation for materiality, target systems and key figures.

In addition, the Sustainability Reporting Navigator (SRN) provides support in navigating the complex set of ESRS regulations. It shows in a modular way which disclosure obligations are relevant, how they are connected and from which sources the necessary data originates. Those who combine the DNK and SRN benefit twice over: data is recorded in clear reporting modules right from the start, responsibilities are defined for each key figure and media disruptions are avoided. This makes auditing easier, increases traceability and reduces errors - a decisive advantage when requirements become more complex over time.

Dual materiality remains the central principle of CSRD and at the same time the most effective protection against unnecessary bureaucracy. It means that only topics that either have a tangible impact on the environment and society or are financially relevant to the company are considered material. Everything else may be omitted or reported in a simplified form.

The Omnibus Regulation does not change this, but gives companies more time to set up their methodology properly. In practice, a three-stage approach is recommended:

- Risk screening along the value chain to identify potentially relevant issues.

- Scoring with clear thresholds to decide what is actually material.

- Linking with planning and controlling so that concrete goals, measures and budgets can be derived from the results.

Companies that consistently apply this logic not only report in a leaner way, but also manage in a more targeted manner. A clear focus on materiality significantly increases the impact of ESG investments in the long term, as resources are directed to the levers that really matter.

Outlook: What companies should do now

The Omnibus Regulation means relief, but not a step backwards: sustainability reports remain mandatory, only the framework conditions have become more practical. Those who make use of the additional leeway can not only act with regulatory certainty, but also make their internal processes more efficient and create added value. It is crucial that companies do not see the shifts as an opportunity to wait and see, but instead actively work on their reporting architecture.

Next dates and deadlines at a glance

The new timing provides orientation for planning and resources:

- Large companies (CSRD Wave 1/2):

First report for financial years from 2024, publication 2025. Audit initially with "limited assurance". - Sector-specific ESRS:

Application planned from 2026 - with a noticeable impact on 2026/2027 reports. - Listed SMEs:

Regular start from 2026, opt-out possible until 2028. - Third country reports (Article 40 CSRD):

Due two years later than originally planned - important for groups with US or UK parent companies. - CBAM:

Quarterly emissions reports remain, financial levies increase gradually with decreasing EU ETS allowances. - CSDDD:

Graduation according to size classes over several years - starting with the largest companies (1,000 employees / € 450 million turnover or more).

Practical tip: Companies should create their own regulatory roadmap that bundles all deadlines for CSRD, taxonomy, CBAM and CSDDD. This roadmap serves as the basis for IT milestones, budget planning and internal resource allocation.

Preparatory steps for affected companies

The Omnibus Regulation provides breathing space - companies should use this time to build robust structures:

- Check affectedness

- Analyzing new thresholds and group consolidation: Which entities are (still) in scope?

- Consider scenarios for growth or acquisitions - thresholds may be exceeded in the coming years.

- Further developing dual materiality

- Screening of climate, environmental and supply chain risks with scenario analyses (e.g. physical vs. transition risks according to ESRS E1).

- Document methodology to pass external audits.

- Modernize data architecture

- Transfer EMAS or ISO 14001 data to a central model.

- Start digital preparation for ESRS tagging (XBRL).

- Ensure data quality with internal controls.

- Use external tools

- DNK platform: Establish initial structure for content and KPIs.

- Sustainability Reporting Navigator (SRN): Modular recording of relevant disclosure obligations.

- Build up audit security

- Implement an internal control system (ICS) for non-financial data.

- Involve auditors at an early stage to avoid queries during the year-end closing phase.

- Integration into the operating business

- Purchasing: Request supply chain data and VSME standards.

- Sales: Consider ESG criteria in tenders.

- Product management: Include taxonomy KPIs and CBAM data in product calculations.

Practical tips for implementation

- Secure quick wins: Start with a few core KPIs (e.g. energy consumption, CO₂, supplier structure) and expand these step by step.

- Use pilot projects: First convert a business unit or subsidiary completely to CSRD logic, gain experience, then roll out.

- Pool resources: Form internal project teams (sustainability, finance, legal, IT) to avoid silos.

- Prepare supplier management: Develop standardized queries to increase data quality and reduce effort.

- Plan for external support: Auditors, ESG consultants or IT service providers can help to cushion bottlenecks in expertise and capacity.

Conclusion: Relief yes, but no standstill

The EU Omnibus Regulation is not a step backwards, but a necessary adjustment: it takes the pace out of implementation without changing direction. For companies, this means less complexity, more time and better proportionality - but by no means a return to voluntary sustainability reporting. German companies in particular should use the relief to set up their reporting and governance structures professionally: from clean data architecture and clear responsibilities to integration into planning and management. Those who invest now in robust processes, digital tools and a clear materiality logic will not only ensure compliance, but will also gain efficiency, credibility and an edge in the competition for capital, customers and talent. The message is clear: the Omnibus Regulation provides breathing space - it is up to each company to decide how well it is used.

FAQ

Yes, even if the increased thresholds mean that some SMEs are considered "medium-sized" instead of "large", other factors remain decisive. Listed companies, group parent companies or subsidiaries in groups subject to reporting requirements often still have to report comprehensively - regardless of their individual size.

The Omnibus Regulation only provides relief at individual company level. At group level, the following applies: as soon as the parent company falls under the CSRD, data from all relevant subsidiaries is required. This means that even small or medium-sized companies must provide data if they are part of a group subject to reporting requirements.

Large companies must submit complete sustainability reports in accordance with the ESRS standards with comprehensive data depth. Medium-sized companies benefit from simplified disclosure requirements and longer transition periods. Listed SMEs will receive their own, leaner ESRS sets and can use the opt-out until 2028 - giving them more time to set up processes.

As things stand, the industry-specific standards (e.g. for chemicals, construction, financial services) will not come into force until 2026. This will give companies two additional reporting cycles to develop industry-specific key figures, identify data sources and set up processes.

The extended deadlines for third-country reports facilitate alignment with international standards such as the SEC Climate Disclosure or the TPT requirements from the UK. This reduces the pressure to coordinate in the short term and international groups can better synchronize their ESG reporting.

Large companies must disclose detailed taxonomy figures, while medium-sized and listed SMEs meet simplified requirements. Safe harbor regulations allow the use of default values if supplier data is not yet available - so companies can submit their reports in a legally compliant manner without having to rely on complete primary data immediately.

The directive starts in stages: Large companies with more than 1,000 employees and a turnover of €450 million will be covered first, with medium-sized companies following later. Medium-sized companies should analyze their supply chains now, document risks and implement initial prevention measures to avoid being under time pressure later.

Since October 2023, importers have had to report emissions on a quarterly basis, but certificates are not due until later. The Omnibus Regulation makes this easier by allowing standard values, defining data sources more clearly and allowing simplified information for small import volumes. This significantly reduces the bureaucratic burden during the transition phase.

The LkSG remains unchanged and supplements the EU requirements. Companies should set up their processes in such a way that risk analyses and control mechanisms cover both the national obligations and the future CSDDD requirements - this avoids duplication of effort.

The shifts are an opportunity to take a structured approach: Establish data architectures, professionalize materiality analyses, introduce internal control systems for sustainability data and clearly divide responsibilities between sustainability, finance and legal. Investing early avoids later hectic and costs.

EMAS provides verified environmental data that can be reused in CSRD logic. The DNK platform offers a practical framework for setting up reporting structures and key figures. The SRN helps to systematically record ESRS obligations and allocate data sources. Together, they shorten the start-up time and increase quality.

In addition to fines and warnings, companies risk reputational damage and the loss of investor confidence. Companies that report inadequately also weaken their competitive position, as customers and investors are increasingly demanding transparency and ESG evidence.