Important facts

- What is an audit?

- An audit is an independent, systematic examination of compliance with standards and specifications.

- Why are audits so important?

- They help identify risks and ensure compliance with rules.

- What types are there?

- There are internal, external, financial, environmental, quality and supplier audits.

- Who administers the exams?

- The audits are carried out by internal auditors or external auditors.

- What happens after an audit?

- After the review, the results are documented and improvements are implemented.

Never miss an update on compliance again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Abstract

Audits are a key tool for systematically verifying compliance with legal requirements, internal policies, and recognized standards. In German, “audit” is usually translated as “Prüfung,” “Revision,” or “Betriebsprüfung,” depending on the context. Audits help companies gain transparency into their processes and structures, identify risks early on, and implement targeted improvements. There are various types of audits, including internal and external audits, as well as specialized audits such as financial, environmental, quality, or supplier audits. Depending on the objective, they are conducted either by internal auditors or by external, independent audit firms.

The audit process follows a clearly defined sequence: from planning and execution through evaluation to the development of concrete action plans. The focus is not only on monitoring but, above all, on the continuous improvement and strategic development of the company. Through the systematic documentation and tracking of nonconformities and recommendations, audits make a valuable contribution to ensuring quality, efficiency, and sustainable corporate governance. These audits are becoming increasingly important, particularly in the context of ESG requirements and growing regulatory complexity.

Definition and Objectives of Audits

What is an audit?

An audit (German: Prüfung or Revision) is a systematic, independent examination designed to determine whether certain requirements are being met, such as legal requirements, internal guidelines, or recognized standards like ISO 9001. The term is derived from the Latin word audire (to listen). The goal of an audit is to provide transparency regarding the conformity of processes, products, or management systems and to identify opportunities for improvement.

Audits thus play a key role in quality assurance, risk mitigation, and compliance with regulatory requirements. Depending on the objectives, an audit may be conducted internally by the company itself or externally by independent third parties.

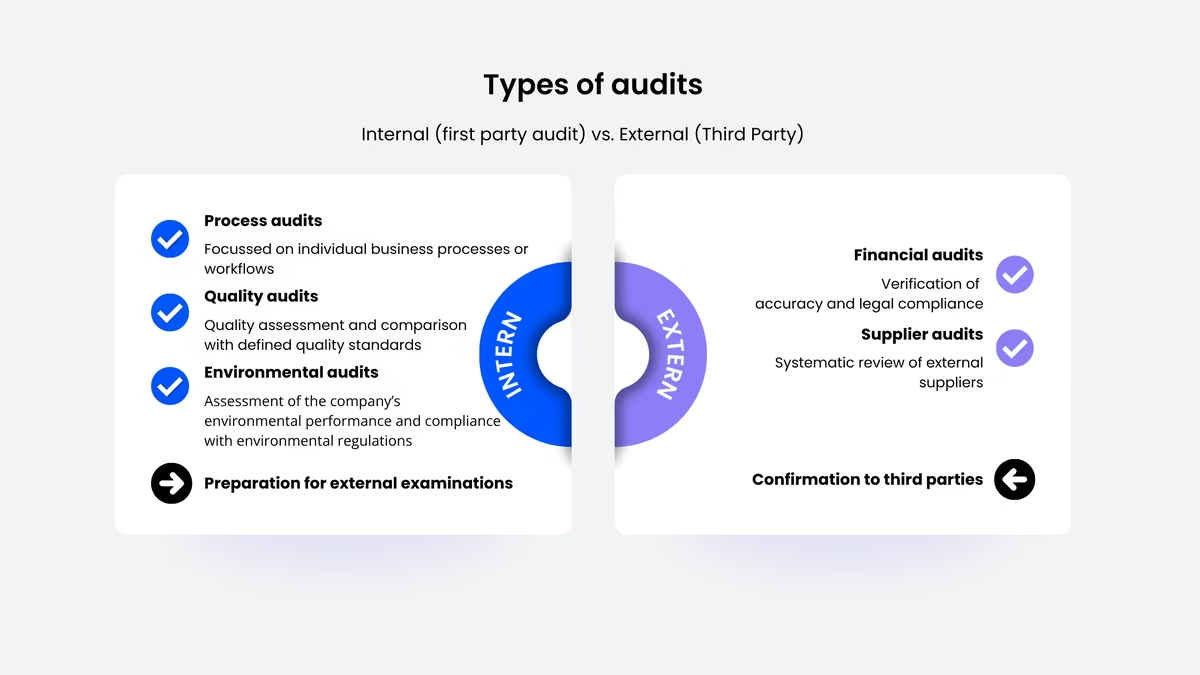

Types of audits

- Internal Audits (First-Party): Conducted by the organization itself to improve processes and identify weaknesses. They are often used to prepare for external audits.

- External audits: Performed by independent third parties to confirm compliance with legal or contractual obligations.

- Process audits: Targeted auditing of individual business processes with regard to efficiency, effectiveness and compliance.

- Financial audits: Focus on the accuracy of financial reports and their compliance with applicable accounting standards.

- Environmental audits: Evaluate a company's environmental performance and compliance with environmental regulations.

- Quality audits: Check whether products or services meet specified quality standards.

- Supplier audits: Systematic review of a supplier's quality, compliance and performance in accordance with contractual and regulatory requirements.

The Importance of Audits for Businesses

Audits are important for a company because they help ensure compliance with legal and internal requirements. Regular audits enable risks to be identified early on, business processes to be optimized, and the trust of investors, customers, and other stakeholders to be strengthened. They provide transparency regarding corporate practices and contribute to the continuous improvement of corporate performance.

Implementing regular audits demonstrates a company's commitment to integrity and sustainability and can secure long-term competitive advantages.

Objectives and Benefits of Audits

An audit serves as a key mechanism for improving efficiency and minimizing risk. By systematically evaluating existing processes, it helps identify weaknesses and implement targeted improvements that go beyond mere compliance with regulatory requirements.

Compliance with legal and internal requirements: Companies must ensure that they comply with all relevant laws, standards and industry-specific requirements in order to avoid legal consequences or financial penalties. An audit uncovers possible deviations and provides recommendations for correction.

Identifying Weaknesses: A detailed analysis of workflows reveals areas that are inefficient or vulnerable to risks, such as redundant processes, opportunities for digital automation, or inefficient use of resources.

Continuous improvement: Audits provide valuable insights that companies can use to continuously develop processes. Regular checks can establish a culture of quality assurance that promotes efficiency and innovation.

Recommended reading: The IIA Global Internal Audit Common Body of Knowledge (CBOK) provides empirical data on the value added by internal audits in companies worldwide.

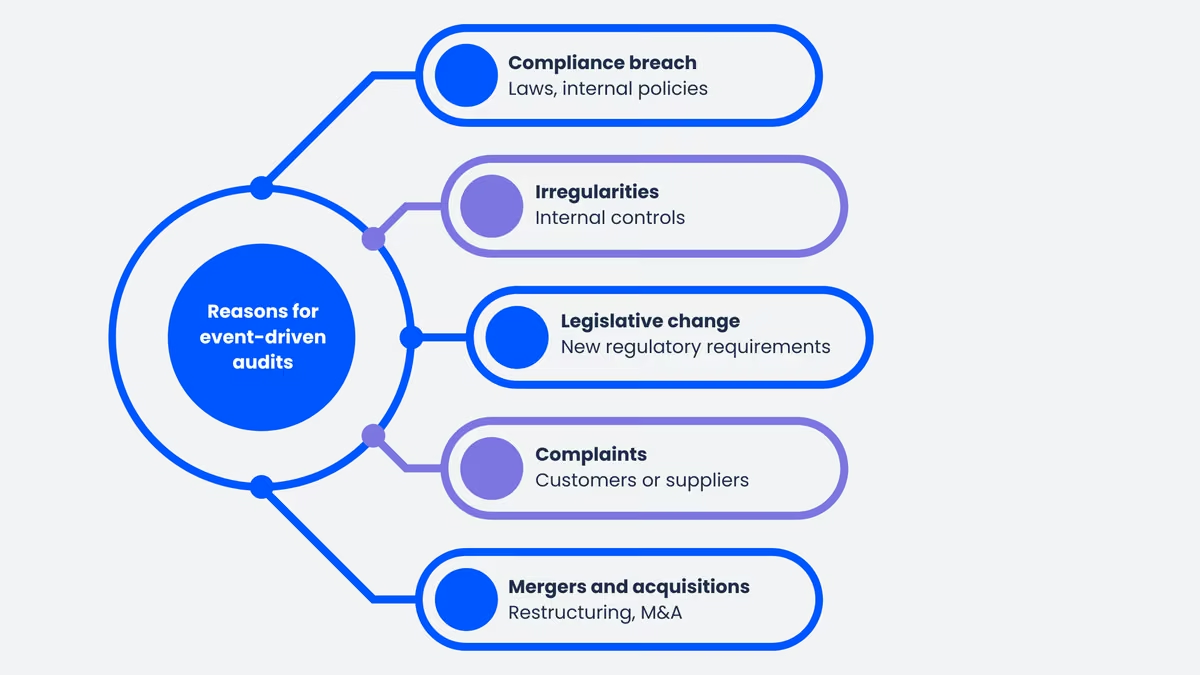

When and how often are audits carried out?

Audits are carried out both regularly and on an ad hoc basis, depending on the specific requirements of a company or sector.

Regular audits are a key component of an effective quality management system. They serve to continuously monitor standards, requirements, and internal guidelines. Many companies conduct internal audits at fixed intervals, such as annually or quarterly. In regulated industries, such audits are often mandatory and subject to strict documentation requirements.

Occasion-related audits are scheduled when special events, risks or deviations require immediate investigation. Typical triggers are compliance violations, irregularities in internal controls, legal changes, customer complaints or mergers and acquisitions.

Event-driven audits enable a targeted investigation of problems and help to develop short-term solutions. They therefore help to minimize financial and legal risks and maintain the trust of customers, investors and other stakeholders.

Costs and Effort Involved in an Audit

The complexity and cost of an audit depend heavily on its type, the scope of the audit, and the size of the company. There is no set figure, but the following guidelines can help with the assessment.

- Internal Audit: The largest cost factor is internal labor time: auditors, process owners, and staff responsible for documentation are tied up for the duration of the audit. Depending on its scope, an internal audit can take anywhere from half a day to several days. Added to this are costs for training and certification of internal auditors, as well as, if applicable, for audit management software.

- External certification audit: External audits, such as those for ISO 9001 certification, incur additional direct costs for the certification body. These costs depend on the size of the company, the industry, and the complexity of the standards, and typically range from four to five figures. Added to this is the internal preparation time, which can be considerable for an initial certification.

- ESG and Sustainability Audits: The CSRD introduces a new cost center: External audits of sustainability reporting are mandatory for affected companies and require specialized auditors. Companies that establish data structures and processes early on can significantly reduce the associated effort.

Rule of thumb

The better the internal preparation, comprehensive documentation, clear responsibilities, and established processes, the shorter and less expensive the audit will be. Those who treat audits as a chore end up paying twice: once for the audit itself, and once for the follow-up work.

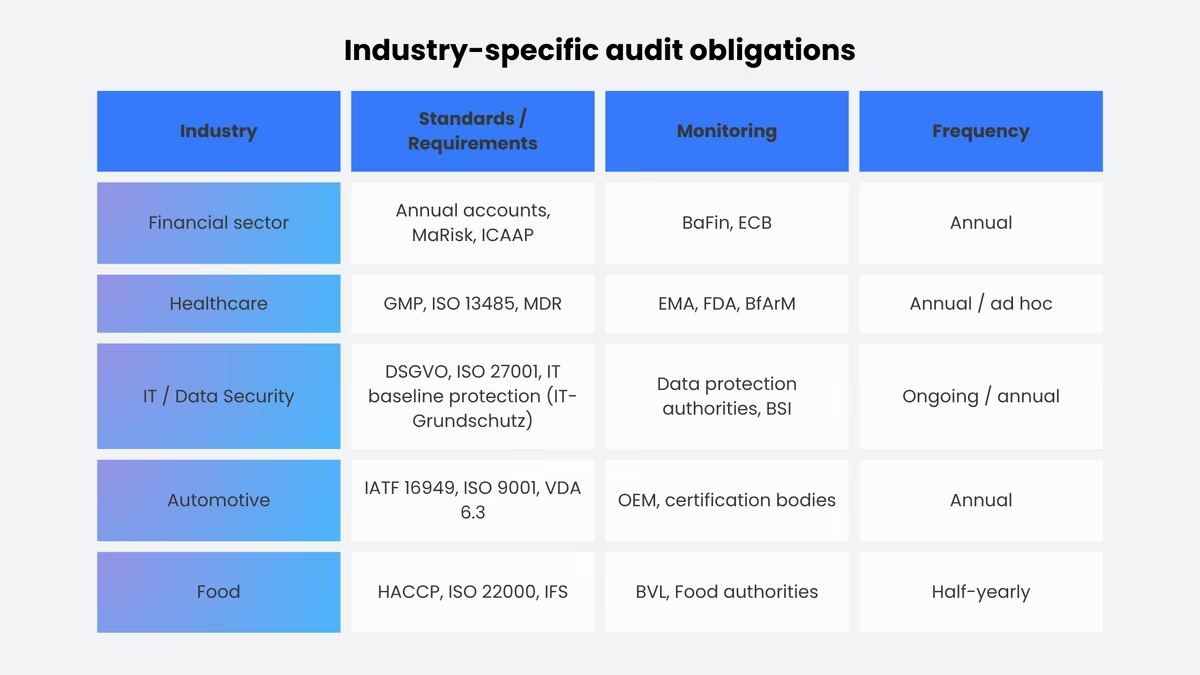

Industry-specific audit obligations

The frequency and nature of these checks depend heavily on legal and industry-specific requirements. Many industries are subject to strict regulatory requirements that oblige companies to conduct certain checks on a regular basis. Meeting these deadlines is essential to avoid legal consequences and financial losses.

Examples of industry-specific audit obligations are:

- Financial sector: Banks and insurance companies are regularly audited by internal and external auditors in accordance with the requirements of BaFin and the European Central Bank.

- Healthcare: Hospitals and pharmaceutical companies must carry out quality assurance and compliance audits in accordance with the guidelines of authorities such as the FDA or EMA.

- Industry and Manufacturing: In the automotive and aerospace industries, quality assurance inspections in accordance with standards such as ISO 9001 or IATF 16949 are mandatory.

- IT and data protection: Companies that process personal data must carry out regular data protection audits in accordance with the GDPR.

Auditors - roles and requirements

Conducting an audit requires expertise, a methodical approach, and an objective evaluation of the processes or systems being audited. In general, audits can be conducted by internal or external auditors, although their roles and responsibilities differ. In addition to in-house auditors, there are independent external auditors as well as specialized institutions and certification bodies that conduct official audits and certifications.

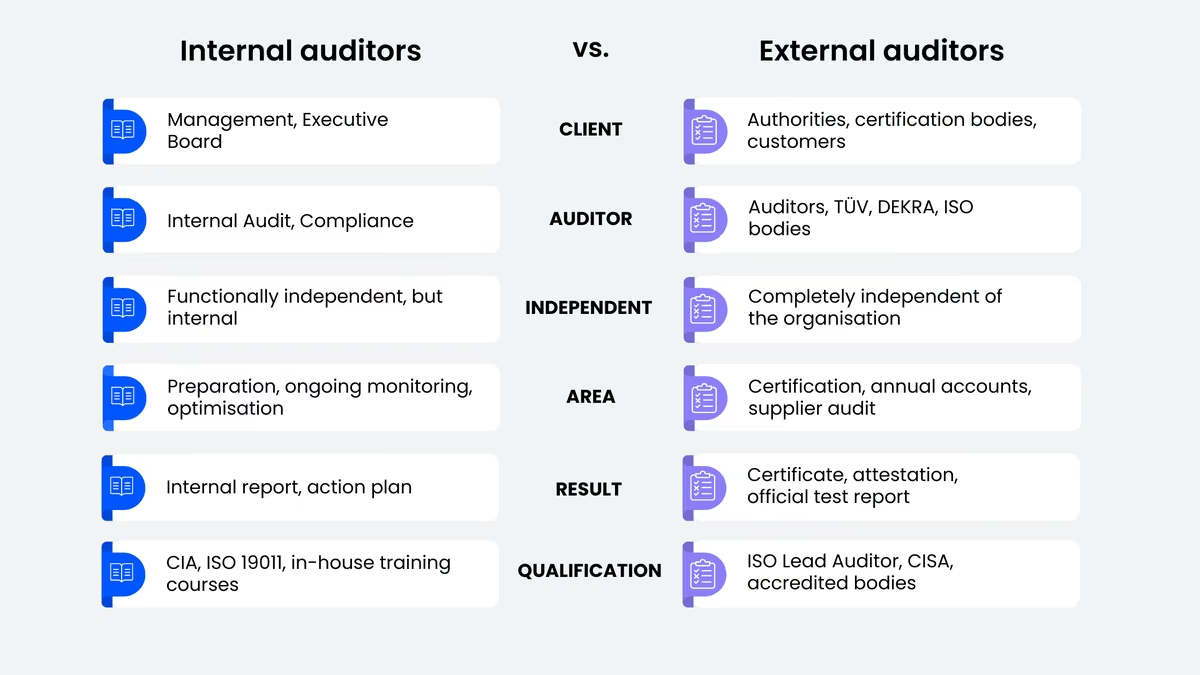

Internal auditors

Internal auditors are internal company auditors who independently monitor and evaluate the organization's processes, structures and regulations on behalf of the management. They are typically based in the internal audit, compliance or quality management departments.

Their independence is crucial: they are not involved in the operational processes of the audited units and report directly to the company management or a supervisory body. Their main tasks include auditing internal guidelines, identifying risks and weaknesses, preparing audit reports and monitoring the implementation of corrective measures.

The main tasks of internal auditors include

- Independent verification of compliance with internal guidelines and external regulations

- Identification of risks and weak points in processes

- Support in the optimization of operational processes

- Preparation of reports and recommendations for management

- Monitoring the implementation of corrective measures

External auditors

External auditors are independent third parties from auditing companies, specialized consulting firms or public authorities. Their independence is a key aspect: they have no internal conflicts of interest and provide objective assessments. They are used for statutory audits (e.g. annual audits), certification audits (e.g. in accordance with ISO 9001), compliance audits by supervisory authorities and supplier audits.

As external auditors have in-depth industry knowledge and specific expertise, they can provide valuable impetus for improving business processes.

Specialized testing institutions and certification bodies

In addition to internal and external auditors, specialized testing institutions and certification bodies play a decisive role in auditing. These organizations specialize in auditing companies according to certain standards and norms and awarding official certifications. The best-known certification bodies include

- TÜV (Technical Inspection Association): Conducts inspections in the areas of quality, safety, and environmental management.

- DIN CERTCO: Certifies products and management systems according to German and international standards.

- DEKRA: Specialized in testing in the areas of safety, environment and automotive.

- ISO certification bodies: Companies that carry out audits for internationally recognized standards such as ISO 9001 (quality management) or ISO 27001 (information security).

Qualifications and requirements

Auditors must have a wide range of specialist knowledge and methodological skills in order to systematically audit and evaluate company processes. The most important technical requirements include

- Knowledge of relevant standards and regulations: Auditors must be familiar with standards such as ISO 9001 (quality management), ISO 14001 (environmental management) or ISO 45001 (occupational health and safety).

- Industry knowledge: Depending on the field of activity, they must have specific specialist knowledge of the requirements of the respective industry, for example in the automotive, finance or food industry.

- Risk assessment and analysis skills: A central task of the auditor is the identification and assessment of risks and the derivation of measures to mitigate risks.

- Communication and interview techniques: Auditors conduct interviews with employees and managers in order to better understand processes. This requires precise questioning techniques and a professional demeanor.

- Documentation and reporting: The ability to document results in a comprehensible and structured manner is essential for the traceability and implementation of audit findings.

In addition to professional expertise, independence, integrity and objectivity are key principles: Auditors must act free of conflicts of interest, handle information confidentially and make judgments based solely on facts.

Recognized certifications include ISO 19011 training for internal auditors, the Certified Lead Auditor (e.g. in accordance with ISO 9001 or ISO 27001), the Certified Internal Auditor (CIA) and the Certified Information Systems Auditor (CISA).

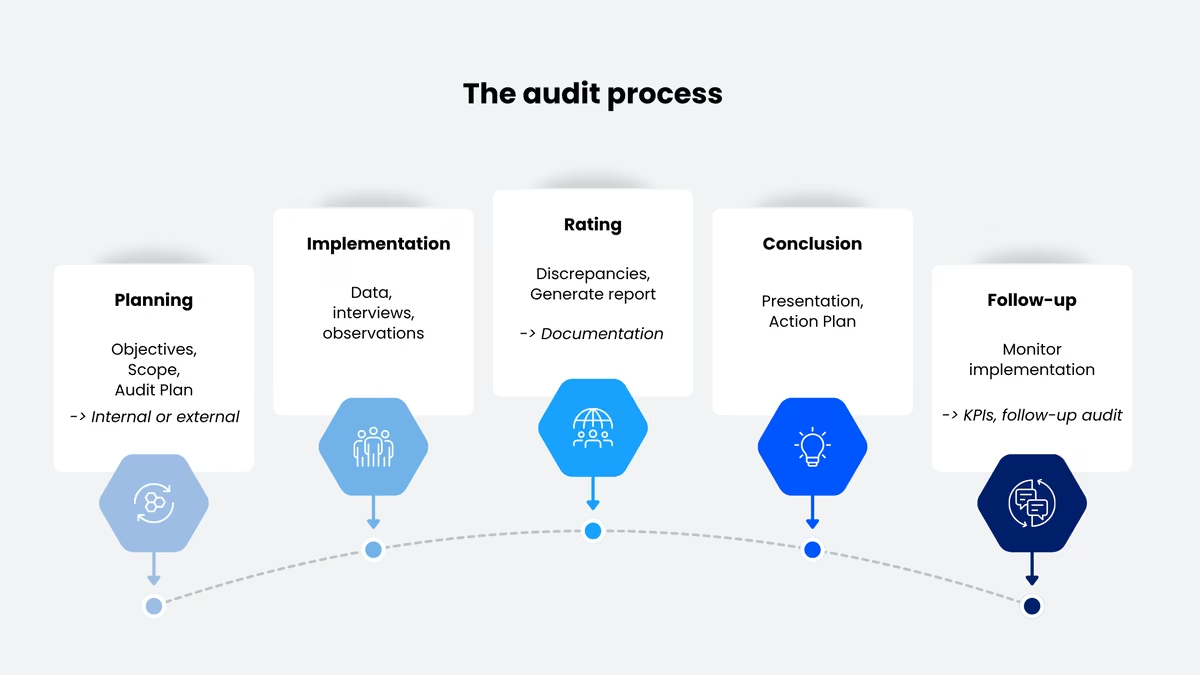

How does an audit process work?

An inspection follows a structured process that ensures all relevant aspects are examined, analyzed, and documented. The process consists of several phases: from planning and preparation through the actual execution to the evaluation of the results and the development of measures for optimization.

Planning and preparation

The first phase consists of detailed planning and preparation. In this phase, the objectives of the audit are defined, the scope of the audit is determined and the necessary resources are organized. This includes identifying the relevant business areas, processes or systems to be audited. A team is also appointed to carry out the audit, which may be internal or external auditors. An essential part of planning is the creation of a plan that describes the exact procedure and methodology of the audit. Relevant documents, guidelines and legal regulations are reviewed in order to create a sound basis for the audit. In addition, initial discussions are held with those responsible in order to gain a comprehensive understanding of the processes to be audited.

Conducting the audit review (data analysis, interviews, observations)

The preparation phase is followed by the actual conduct of the audit. During this phase, the auditors gather relevant information and evaluate the processes using various methods. These include:

- Data analysis: Auditors check company data, reports and documentation to identify deviations or irregularities.

- Interviews: Interviews with employees and managers help to gain an in-depth understanding of internal processes and identify potential problems or areas for improvement.

- Observations: Work processes and operating procedures are analyzed directly on site in order to uncover potential risks or inefficiencies.

This combination of analytical and practical methods enables a holistic assessment of the audited areas. During the audit, the auditors take care to proceed systematically and objectively in order to obtain as realistic an assessment of the company's processes as possible.

Evaluation and documentation of the results

Once all relevant data has been collected, the results are evaluated and documented. In this phase, the collected information is analyzed, reviewed and compared with the defined standards or regulations. The aim is to clearly identify possible deviations, risks or optimization potential. The results are recorded in a detailed report. This report contains

- A summary of the areas audited and methods used

- Detected deviations or violations of guidelines and standards

- Recommendations for remedying identified weaknesses

- Positive aspects and best practices within the company

Careful documentation is essential. It not only serves as proof for internal and external stakeholders, but is also used as a basis for future improvement measures.

Final discussion and recommendation of measures

At the end of the audit process, a meeting is held with the relevant decision-makers and process owners. In this meeting, the auditors present the most important findings from the audit, explain identified risks and make specific recommendations for improvement measures. The aim of the final meeting is to develop a joint strategy for implementing the proposed measures. The following points may be discussed:

- Prioritization of the problems identified: Which deviations need to be rectified immediately, which have long-term effects?

- Development of an action plan: Who is responsible for implementing the recommendations and what deadlines are set?

- Monitoring and follow-up: How is it ensured that the measures taken have a lasting effect?

The final meeting ensures that the results are not only documented, but also actively used to continuously improve the company's processes.

Overview of the audit process

An audit follows a structured process that ensures that all relevant aspects are checked, analyzed and documented.

- Planning and preparation: Definition of objectives, determination of the scope of the audit, organization of resources, creation of an audit plan, review of relevant documents and initial discussions with those responsible.

- Implementation: Auditors gather information through data analysis (reports, documentation), interviews with employees and managers and direct observation of work processes on site.

- Evaluation and Documentation: The information gathered is analyzed and compared against defined standards. The results are documented in a structured report that includes a summary of the areas reviewed, identified nonconformities, recommendations for corrective action, and positive aspects.

- Final meeting: Presentation of the results to decision-makers, development of a joint action plan with clear responsibilities, deadlines and control mechanisms.

Risk management audits

Audits are an essential part of a comprehensive risk strategy. They help identify, assess, and manage risks early on, before they impact the business.

Early risk detection

Targeted audits can be used to identify compliance risks, financial risks (miscalculations, fraud), operational risks (process failures, production errors) and cyber risks (data protection breaches, IT security deficiencies) and limit them through preventive measures.

Cyber risks are a particularly growing problem area, ranging from data protection breaches and IT security deficiencies to targeted hacker attacks. The BSI situation report on IT security in Germany and the ENISA Threat Landscape provide up-to-date data on the threat situation that is directly relevant for IT audits.

Support with strategic decisions

Audits provide valuable insights that help executives with strategic planning and decision-making. Possible applications of audits in strategic planning include:

- Expansion and investments: Assessment of the financial and operational risks associated with new markets or business areas

- Mergers & Acquisitions: Analysis of the financial stability and compliance of the companies to be acquired

- Innovation and digitization strategies: Identification of potential for improvement in IT and process landscapes

- Sustainability management: review of ESG criteria (environmental, social, governance) for compliance with regulatory requirements

Sound results make it possible to make strategic decisions on a solid, risk-conscious basis.

Ensuring financial and operational stability

By systematically reviewing business processes, internal control systems and financial structures, weaknesses can be identified at an early stage and measures taken to stabilize them. In the area of finance, they support the analysis of a company's economic performance by reviewing balance sheets, cash flows and budget controls. This minimizes financial risks and ensures sustainable liquidity planning. At the same time, audits help to identify inefficient business processes and initiate optimization measures in order to use resources more efficiently and reduce costs. Another important aspect is the review of internal control mechanisms for fraud prevention and error avoidance.

Companies benefit from clear governance structures that are strengthened by regular audits.

Standards and guidelines

Internationally recognized standards and guidelines play a central role in the conduct of analyses. They provide a structured framework and specific recommendations for action that significantly enhance the quality and validity of tests.

ISO 19011 - Guide to auditing management systems

ISO 19011 provides a comprehensive guide for auditing management systems. It defines principles and practical guidance for systematic, objective assessments and emphasizes the competence and impartiality of auditors.

Relevant ISO standards

In addition to ISO 19011, there are other standards that place specific requirements on various management systems. Companies that wish to be certified or carry out regular audits are often guided by the following ISO standards:

ISO 9001 (Quality Management): This standard is one of the best-known worldwide and specifies the requirements for an effective quality management system (QMS). Companies certified to ISO 9001 must conduct regular internal and external audits to ensure compliance with quality standards.

ISO 14001 (environmental management): This standard defines requirements for an environmental management system (EMS) and is used by companies to improve their environmental performance. ISO 14001 audits check, among other things, whether a company implements measures to protect the environment and complies with environmental regulations.

ISO 45001 (occupational health and safety management): This standard focuses on the protection of employees and safe working conditions. ISO 45001-certified companies carry out audits to identify hazards in the workplace and reduce risks.

In addition to these widely used standards, there are many other ISO standards that regulate specific aspects such as information security management (ISO 27001) or energy management (ISO 50001). Companies that follow these standards benefit from structured processes and increased credibility with customers and business partners.

CSRD and ESG audits

With the EU's Corporate Sustainability Reporting Directive(CSRD) coming into force from 2024/2025, the importance of sustainability audits will grow considerably. Companies that fall under the CSRD must prepare their ESG reporting in accordance with the European Sustainability Reporting Standards(ESRS) and have it audited externally.

Industry and country-specific regulations

In addition to the international standards, there are also numerous specific regulations that are tailored to certain industries or countries. These guidelines take into account local legal requirements and cultural characteristics. This is particularly important for multinational companies that have to coordinate their business activities worldwide. Industry and country-specific regulations offer additional protection and ensure that audits comply with international requirements. In addition, they also fulfill the intricacies of the respective market segments and legal framework conditions. This not only strengthens legal compliance, but also confidence in corporate integrity.

Examples of industry-specific standards are

- IATF 16949 (automotive industry): This standard supplements ISO 9001 and defines specific quality requirements for the automotive industry.

- HACCP (food industry): This concept is used to analyze hazards and control critical control points in food production.

- GDPR/DSGVO (data protection in the EU): Companies that process personal data must carry out data protection audits to ensure compliance with the General Data Protection Regulation (GDPR).

Preparation and importance of audit reports

The report is the central result of every audit and serves as written documentation of the audit carried out. The comprehensive audit report summarizes the most important findings, records deviations and provides specific recommendations for optimization. A well-structured report is important as it helps management to make decisions and enables targeted improvements.

Structure and main contents

An audit report usually follows a clearly structured outline in order to present the findings in a comprehensible manner. The structure can vary depending on the company and type of audit, but usually contains the following key components:

- Introduction: Description of the scope, the areas audited and the methods used.

- Objective: Presentation of the objectives, such as checking compliance with regulations, identifying weaknesses or assessing risks.

- Methodology: Brief explanation of the audit methods used, such as interviews, document reviews or observations of processes.

- Results: Detailed presentation of the audit findings, including positive aspects and identified deviations or deficiencies.

- Evaluation and conclusions: Analysis of the findings with an overall assessment of the audited processes.

- Recommendations: Concrete proposals for measures to eliminate weaknesses and optimize processes.

- Appendix: Additional documents, test protocols or further analyses that supplement the report.

A clear report helps those responsible to quickly grasp the most important results and implement targeted improvements.

Documentation of deviations and recommendations

A central component of every audit report is the careful documentation of deviations from the defined standards. These deviations must be described clearly and precisely in order to ensure a complete picture of the situation.

- Description of the deviation: Detailed description of the problem identified.

- Relevant regulations or standards: Reference to the standard or directive that has been violated.

- Impact of the deviation: Assessment of the possible consequences for the company.

- Recommended corrective actions: Suggestions for correcting the nonconformance, including timeframes and responsibilities.

In addition to listing deviations, the recommendation of specific measures plays a decisive role. The proposals should be realistically implementable and tailored to the specific circumstances of the company.

Detailed documentation and clear recommendations for action can ensure that concrete improvements are derived from the findings of the audit.

Use of the report for decision-making

Once the process has been successfully completed and the report generated, executives can take targeted actions based on the analyses and recommendations contained in the report. The report plays an essential role, particularly in strategic planning. It helps to better assess existing risks and make informed decisions to improve operational processes. Furthermore, it supports risk management by identifying vulnerabilities and enabling preventive measures before potential problems escalate. Quality assurance also benefits from the recommendations for action outlined in the audit report. It contributes to the continuous improvement of internal processes, which increases efficiency and compliance in the long term.

Another crucial aspect is the follow-up of the recommended measures. The report serves as a reference document that makes it possible to monitor progress in the implementation of the proposed improvements. This ensures that identified weaknesses are not only documented, but actively addressed and remedied.

Development of concrete action plans and monitoring of implementation

Once a review has uncovered weaknesses and opportunities for improvement, these should be set out in a clear action plan. The plan should describe exactly which corrections are necessary in this context, who will implement them and by when they must be completed.

Typical components of an action plan are

- Description of the identified deviation or potential for improvement

- Specification of the necessary measures for rectification or optimization

- Determination of the responsible persons or departments

- Definition of a realistic timetable for implementation

- Definition of success criteria for evaluating the effectiveness of measures

A well-developed action plan helps ensure that the recommendations outlined in the report are implemented in a focused and efficient manner. It also provides clarity regarding the upcoming changes and makes it easier for the employees involved to understand their roles in this process.

Once the action plans have been developed, continuous monitoring of their implementation is essential. Clear milestones and regular progress reports are required in order to document the progress of implementation in a comprehensible manner. Success monitoring plays an equally important role in evaluating the actual benefits of the measures implemented and making adjustments where necessary. This evaluation is based on defined key figures and targets that are compared with the initial results.

The audit report is the central result of every audit. It summarizes the findings, documents deviations and provides specific recommendations. A well-structured report contains: Introduction and audit scope, objectives, methodology used, detailed findings and deviations, evaluation and conclusions, prioritized recommendations and an appendix with audit protocols.

From insight to action: Based on the report, a concrete action plan is developed that defines responsibilities, deadlines and success criteria. Progress is then monitored through regular follow-up audits or review meetings.

Integration into Corporate Strategy: Findings from audits should be incorporated into strategic planning on an ongoing basis, serving as the foundation for investment decisions, process optimizations, and the further development of the compliance strategy. Companies that utilize audits in this way embed improvements in a sustainable manner and enhance their long-term competitiveness.

Digitalization of the audit process

Increasing digitalization is fundamentally changing audit practices. Specialized software makes it possible to standardize audit processes, manage documentation centrally, and analyze results in real time.

In addition, the use of AI and data analytics opens up new possibilities: Instead of traditional spot checks, complete data records can be automatically examined for anomalies. This increases the depth of checks and at the same time significantly reduces manual effort.

For companies, this means that those who digitize their audit processes not only gain in efficiency but also improve the quality and traceability of their results.

The IIA regularly publishes reports on the digital transformation of internal audit functions, including the use of AI in auditing.

Challenges, Advantages, and Disadvantages of Audits

Challenges when conducting an audit

Conducting an audit can present various challenges that complicate the audit process and affect the quality of the results. Auditors often face problems such as insufficient data, limited time and personnel resources, or resistance within the company. Therefore, conducting a successful audit requires more than just methodological expertise and technical knowledge; it also requires forward-looking planning and a sensitive approach to dealing with internal challenges.

Lack of data and documentation: Without complete and precise documentation, it is considerably more difficult to analyze company processes. Digital documentation systems, regular internal checks and a clear assignment of responsibilities help to improve the data situation.

Time and resource management: Auditors are often under time pressure, especially when several business areas have to be audited or external audits are tied to fixed deadlines. Early planning, clear priorities and digital tools for data automation reduce the workload considerably.

Resistance within the company: Employees or managers sometimes view audits as a control mechanism rather than an improvement tool. Auditors should clearly communicate the purpose and benefits, focus on continuous improvement and reduce resistance through a culture of open discussion.

In summary, audits require not only methodological expertise and technical knowledge, but also strategic skill in addressing challenges. A solid foundation of documentation, structured time and resource management, and effective communication with all stakeholders are critical factors for a smooth process.

Pros and Cons

Audits offer companies clear added value, but they are not a sure thing. Those who are aware of the typical weaknesses can take corrective action before they undermine the audit process.

Advantages

Audits provide transparency into processes that often remain hidden in day-to-day operations. They identify risks before they escalate, strengthen the trust of customers, investors, and regulatory authorities, and lay the foundation for continuous improvement. Especially in regulated industries, regular audits ensure compliance with certification requirements and protect against legal consequences.

Disadvantages

The main point of criticism is the resource expenditure: Internal audits tie up employee time, while external audits can sometimes incur significant costs. Added to this is the risk of so-called “audit theater,” where companies optimize processes for the audit rather than for day-to-day operations. When audits are perceived as a control mechanism rather than a tool for improvement, resistance quickly arises within the team, which noticeably reduces the quality of the results.

The benefits outweigh the costs, but only if audits are taken seriously and followed up on consistently. An audit whose recommendations end up gathering dust in a drawer is just a waste of time.

These four developments have a significant impact on current practice.

Audit Trends

Artificial intelligence is changing the way audits are conducted. Instead of traditional spot checks, entire data sets can be automatically analyzed for anomalies, patterns, and deviations. This significantly increases the depth of the audit while reducing the amount of manual work required. Specialized audit management platforms also enable centralized documentation, automated reminders, and real-time analyses that would previously have taken weeks to complete.

Since the pandemic, remote audits have become an established alternative. Video conference interviews, digital document reviews, and cloud-based platforms enable audits without an on-site presence, which is particularly relevant for international supply chains and companies with multiple locations. Many standards, including ISO 9001, now officially recognize virtual audits.

The trend is moving away from rigid audit plans toward risk-based approaches: Instead of auditing all areas with the same level of intensity, auditors focus on the processes with the highest risk potential. This conserves resources and increases the significance of the results. ISO 19011 explicitly recommends this approach.

With the Corporate Sustainability Reporting Directive (CSRD), sustainability audits are no longer optional for an increasing number of companies—they are now mandatory. Companies subject to the CSRD must have their ESG reporting externally audited in accordance with the European Sustainability Reporting Standards (ESRS). This places new demands on auditors, processes, and data availability, making early preparation crucial.

Conclusion

Audits have long since ceased to be merely a compliance tool. From an operational perspective, they reveal vulnerabilities before they turn into serious problems—whether in production, IT, or the supply chain. Financially, they provide the transparency that investors and regulatory authorities demand. And strategically, they form the data foundation for informed decisions regarding expansion, M&A processes, or the development of sustainable business models.

With the CSRD and the European Sustainability Reporting Standards (ESRS), companies are increasingly obliged to have their ESG performance audited externally. At the same time, digitalization is fundamentally changing auditing practices: AI-supported analysis tools and specialized audit management platforms enable deeper, faster and more cost-effective audits. Companies that combine the two at an early stage have a clear advantage.

The key point remains: The value of an audit does not lie in the report itself, but in the actions that result from it. Those who consistently establish the cycle of audit, insight, and implementation are not investing in control, but in trust, quality, and long-term resilience.

Frequently asked questions

The frequency depends on legal requirements, internal company guidelines and the company's risk profile. In many industries, annual or semi-annual audits are common, especially in finance, healthcare or certified management systems. Companies with a high pace of change or increased risk should audit more frequently to stay on track. In addition, ad hoc audits may be required at any time.

An audit is a systematic, process-oriented review procedure aimed at identifying compliance and opportunities for improvement. An inspection is usually ad hoc, focused on specific objects or activities, and tends to provide a snapshot of the current situation. While an audit often results in comprehensive reports and action plans, an inspection aims to make immediate findings. Both procedures can complement each other, but they follow different approaches.

Audits are an important tool for reviewing environmental, social and governance (ESG) criteria. They help companies to systematically evaluate and implement legal requirements, voluntary standards and sustainability goals. Audits make a particularly valuable contribution to the disclosure of ESG key figures or the preparation of sustainability reports. They strengthen credibility with investors and stakeholders and promote correct external communication.

Good preparation begins with the review of relevant documents, the use of clear process documentation and the provision of suitable contact persons. Responsible departments should be informed in advance about the scope and actively involved. An internal pre-check or self-audit can also help to identify potential weaknesses at an early stage. Transparency, openness and organization are crucial here.

Frequent sources of error are incomplete documentation, a lack of communication between departments and a lack of follow-up of measures. Time pressure or unclear responsibilities can also affect the quality of an audit. If auditors cannot act independently or do not have sufficient training, objectivity suffers. To avoid these risks, good planning and a clear allocation of roles are important.

Effectiveness is measured by whether the measures recommended in the report have been implemented and have achieved concrete improvements. Key performance indicators (KPIs), deadlines and target values are usually defined to measure progress. Follow-up audits or regular review meetings are also used to monitor success. An effective audit shows sustainable process improvements, not just formal implementation.

Auditors need sound specialist knowledge, knowledge of relevant standards and practical experience in the process. Methodological skills such as analytical thinking, conducting interviews and preparing reports are also important. In addition, they must act independently and with integrity to ensure objective assessments. Certifications such as ISO Lead Auditor, CIA or CISA strengthen the formal qualification.

Alexander Hilmar

LinkedInESG compliance expert - lawcode GmbH

Alexander Hilmar advises companies on the implementation of ESG compliance, sustainable reporting and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.