Important facts

- What does the Delegated Act 2026 change about the EUDR?

- It amends Annex I: 17 new product codes are included, three are deleted and one is clarified.

- Which products are new to the EUDR scope?

- Frozen beef tongues, soluble coffee, a range of oleochemical palm oil derivatives and soap bars and flakes.

- Which products are out of scope?

- Cattle hides, skins and leather are deleted, and for retreaded tires EUDR obligations only apply to the new rubber tread.

- Is the delegated act already binding?

- No, as of May 2026 only the draft is available, the public consultation runs until June 1, 2026, it will only become binding when it is published in the Official Journal.

- What do the changes mean in economic terms?

- The overall compliance costs of the EUDR are expected to fall by around 75%, with the expected environmental benefits amounting to around EUR 7 billion per year.

Never miss an update on the EUDR again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Executive Summary

The draft delegated act of May 2026 amends Annex I of the EUDR on the basis of Article 34(1) and a systematic assessment of 31 product codes by the Commission. Frozen bovine tongues, soluble coffee, a range of oleochemical palm oil derivatives and soap bars and flakes will be added to the scope, while bovine hides, skins and leather will be removed and the EUDR obligations for retreaded tires will in future only apply to the new tread.

At the same time, the legal act specifies what is explicitly not covered: waste, used and second-hand products, samples, packaging of any material including reusable packaging, marketing material and correspondence. It also specifies the species boundaries for cattle, palm oil and rubber as well as the list of non-relevant woody materials such as bamboo, rattan and lime bark.

For companies, this means preparing HS code mappings now and marking them as "expected" while publication in the Official Journal is pending, initiating supplier communication for the new registrations and keeping an eye on the start of application of the EUDR, i.e. December 30, 2026 for large and medium-sized companies and June 30, 2027 for micro and small companies.

Why a delegated act at all?

Article 34(1) EUDR empowers the Commission to adapt Annex I, i.e. the list of relevant products, by means of delegated acts. This is not a bureaucratic end in itself: the original impact assessment for the EUDR did not contain a detailed assessment of the individual HS codes. Stakeholders from industry, associations, NGOs and third countries quickly realized in practice that individual codes were missing, with the result that the deforestation risk could be shifted from the regulated to the unregulated part of the supply chain.

The Commission then systematically evaluated 31 product codes proposed by stakeholders for inclusion or deletion. The assessment combined two components:

- Quantitative: deforestation footprint, monetized environmental benefits (€10,000 per hectare of avoided deforestation, €100 per tonne of CO₂) and recurring compliance costs at HS Code level.

- Qualitative: Consistency along the supply chain, avoidance of circumvention risks, proportionality of the burden.

For a product to be included, there must either be a risk of displacement (upstream inputs are already regulated and the product contains more than 75% of the relevant raw material) or the environmental benefits must clearly outweigh the compliance costs, with a maximum administrative cost of 5% of the commercial value.

Important: As of May 2026, the legal act has not yet been published in the Official Journal. The public consultation runs until June 1, 2026 and the changes will only become binding once they have been formally adopted. Companies should prepare their HS Code mappings, but mark them as "expected" until then.

Substantial scope changes

The Commission has developed a two-path logic for the inclusion of a product. This is preceded by an assessment of supply chain continuity: if an upstream product is already regulated, the downstream derivative should not fall through the cracks. If a product does not meet this requirement, the assessment runs via two alternative paths. Path I ("relocation risk") applies if the share of the relevant raw material in the end product is over 75% and the EU production capacity accounts for at least 50% of the import volume. Pathway II ("deforestation and administrative burden") requires a minimum deforestation threshold of 0.005 hectares per tonne of product or 100 hectares in absolute terms, combined with an administrative burden of no more than 5% of the commercial value.

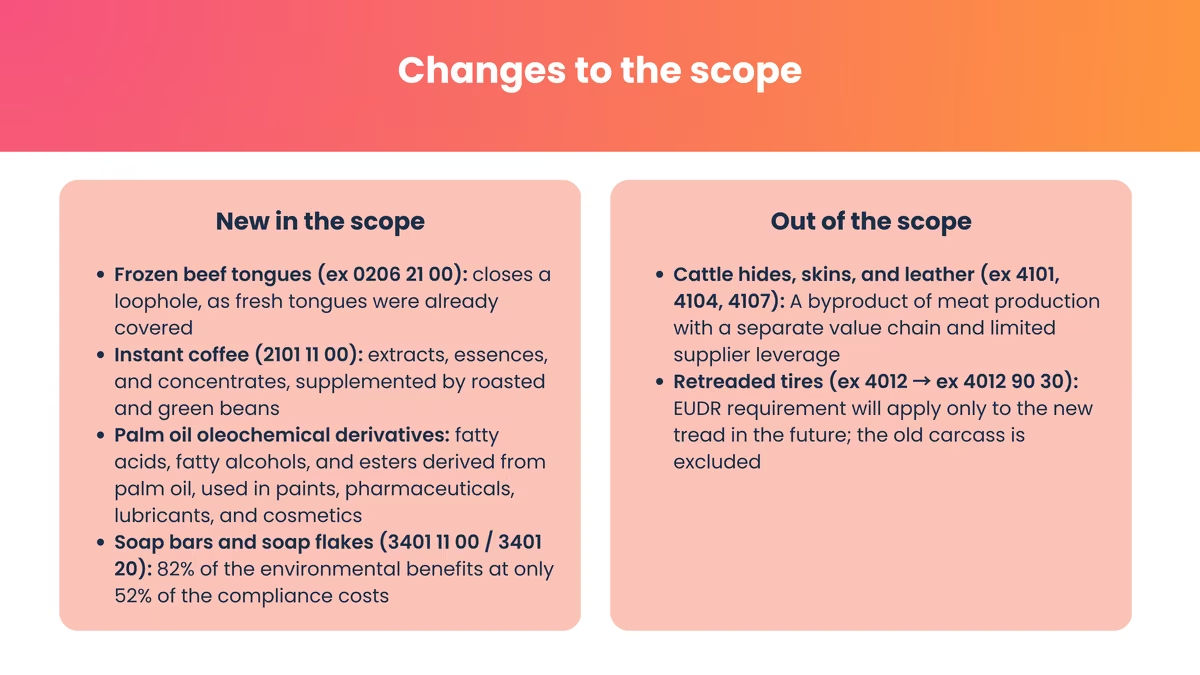

What's new in the scope

- Frozen beef tongues (ex 0206 21 00): Fresh beef tongues were already recorded, the frozen variant was not. This would have opened up a classic bypass scenario: Importers could have simply switched to the frozen form. The inclusion establishes consistency within the cattle supply chain.

- Soluble coffee (2101 11 00): Roasted and green coffee beans were already in scope, soluble extracts, essences and concentrates were not. The quantitative analysis shows clear environmental benefits; in qualitative terms, the inclusion closes the gap for a highly processed product with a high market volume.

- Palm oil oleochemical derivatives: Probably the most extensive extension concerns palm oil derivatives used in paints, varnishes, pharmaceuticals, lubricants, food additives and cosmetics. First of all, the partially or fully hydrogenated, interesterified, re-esterified or elaidinized palm, palm kernel and babassu oils (ex 1516 20) and their boiled variants (ex 1518 00) are included. In addition, there are alcohols synthesized from oil palms such as octanol, dodecan-1-ol, hexadecan-1-ol and octadecan-1-ol (ex 2905 16, ex 2905 17, ex 2905 19), the esters of acetic acid (ex 2915 39), palmitic acid and stearic acid together with their salts and esters (ex 2915 70), other saturated acyclic monocarboxylic acids from oil palms (ex 2915 90) and undecenoylic acids with their salts and esters (ex 2916 19 10). Industrial oleic acid and other industrial monocarboxylic acids (ex 3823 12, ex 3823 19) will also be included in the scope in future, as will industrial fatty alcohols from oil palms (ex 3823 70 00), other chemical products with palm oil components (ex 3824 99) and polyethers in primary forms from palm oil (ex 3907 29). Oleic, linoleic and linolenic acids (2916 15) and acyclic polyamines (2921 29 00) were not included because the cost-benefit analysis was negative in this case.

- Soap bars and soap flakes (3401 11 00 and 3401 20): Across the entire "soaps and surfactants" group, inclusion would not have been economical. However, soap bars and soap flakes are a special case: they have a significantly higher natural oil content and account for 82% of the total environmental benefits of this product group, with only 52% of the estimated compliance costs. They were therefore specifically included, while the rest of HS 3401 was not.

What falls outside the scope

- Hides, skins and leather of bovine animals (ex 4101, ex 4104, ex 4107): The deletion follows a differentiated justification. Leather is a by-product of meat production with comparatively low economic weight. In practice, leather operators have little leverage over upstream suppliers outside the EU. The value chain for leather is also separate from the meat chain, which makes it disproportionately difficult to obtain information. There is also an imbalance: finished leather goods such as shoes or handbags would never have been covered anyway, so EU leather processors would have been more strictly regulated than importers of finished end products.

- Retreaded tires - restriction to the tread: The previous entry ex 4012 is replaced by the more specific entry ex 4012 90 30 (tire covers). The logic: Around 75% of retreaded tires consist of an old, used carcass, for which traceability is practically impossible. The new tread only makes up around 25% and contains only around 20% natural rubber. In future, EUDR obligations will therefore only apply to the newly applied tread. The used tire carcass falls out of scope as waste at the end of its life cycle. This explicitly promotes the circular economy and resource efficiency.

Editorial adaptation for live cattle

The previous entries "0102 21 Live bovine animals, pure-bred breeding animals" and "0102 29 Live bovine animals, other" are replaced by thecollective entry ex 0102 Live bovine animals. This is purely editorial, the product scope does not change. The preceding "ex" clarifies that only cattle of the genus Bos and its subgenera are included, not buffalo(Syncerus) or bison(Bison).

Technical clarifications: What is explicitly not covered

In addition to the substantial changes to the scope, the draft specifies a number of exceptions that had previously raised questions of interpretation in practice.

Waste, used and second-hand products, including their components, are excluded insofar as they qualify as waste within the meaning of Directive 2008/98/EC, used or second-hand. If a product contains non-recycled components, the EUDR applies to these components. The exemption only applies if the product consists entirely of material that has completed its life cycle and would otherwise have been disposed of as waste. If a product contains non-recycled content from relevant raw materials, this content is still subject to the EUDR.

Samples and test products with negligible value and small quantities are exempt if they are only used for order acquisition or for the examination, analysis or testing of composition, quality or other technical characteristics. The legal anchor is Regulation (EC) 1186/2009.

Packaging, and not just wooden packaging, but packaging materials and containers regardless of material, is exempt as soon as it is used exclusively to support, protect or carry another product. This also applies explicitly to reusable packaging (reusable containers, pallet pools). EUDR obligations only apply when packaging is placed on the market independently for the first time, for example when new pallets are sold, or when used packaging is repaired and sold with new wooden components; in the case of repairs, only for the new components.

Marketing and information material, such as manuals, brochures, labels that accompany a product or are provided free of charge for marketing purposes are not covered by the regulation. Neither does correspondence within the meaning of Regulation (EU) 2015/2446 (UCC-DA).

Extended list of non-relevant materials

The legal act also specifies which species and materials are not covered:

- Cattle: Only Bos and subgenera, no buffalo, no bison.

- Palm oil: Only Elaeis spp. - Babassu oil(Attalea spp.) and other palm species are excluded.

- Rubber: Only Hevea brasiliensis - Balata, Guttapercha, Guayule, Chicle and synthetic rubber are not included.

- Wood: Bamboo, rattan, reed, rushes, willow rod (osier), raffia, cleaned/bleached/dyed cereal straw and lime bark are not included in the wood scope.

For mixed products, such as "ex 4011 New pneumatic tires made of rubber" made of synthetic and natural rubber, the due diligence only applies to the natural rubber component.

Proposals that were not implemented

Three stakeholder proposals are particularly noteworthy because the Commission decided against them, for different reasons:

- Biodiesel (HS 3826 00 10): The quantitative analysis would have supported inclusion, the deforestation footprint is significant. However, biodiesel is already subject to the Renewable Energy Directive (EU) 2018/2001 (RED II), which comprehensively regulates environmental impacts. Additional EUDR coverage would be double regulation without added value.

- animal feed preparations (HS 2309): In quantitative terms, the environmental benefits (€51.4 million/year) exceeded the compliance costs (€12.4 million/year) by a factor of four. However, the Commission did not consider the impact on the agricultural sector, in particular on food sovereignty and strategic dependencies, to be sufficiently assessed and has suspended the inclusion for the time being.

- Oil cake from palm nuts or kernels (HS 2306 60): Stakeholders had called for this to be removed. The Commission rejected this: environmental benefits of € 154.5 million are offset by compliance costs of only € 187,000. In qualitative terms, deletion would contradict the coherent approach in the palm oil supply chain and create an imbalance with soybean cake or cocoa shells, which are still covered.

What this means in practice - three examples

Chocolate manufacturer with palm oil esters

A medium-sized manufacturer of industrial cleaning and care products imports certain acetic acid esters from palm oil (HS ex 2915 39) as a separate raw material for its production. Until now, this import did not fall within the EUDR scope. The Delegated Act changes this: when importing, the operator must perform full due diligence with geolocalization of the cultivation areas, risk assessment and DDS. This closes a gap and increases the administrative burden.

Important distinction: In the case of composite products such as chocolate (HS 1806), where cocoa is the main product "linked" according to Annex I, the due diligence would only relate to the cocoa components, not automatically to the palm oil or palm oil derivatives contained, even if these are listed in Annex I in isolation. The scope of obligations therefore depends on whether the palm oil derivatives are imported as a relevant product in their own right or are part of another composite product.

Importer of leather goods

An importer of high-quality bags and belts used to purchase tanned cowhide (HS 4104) in the EUDR scope. According to the Delegated Act, this leather falls out of Annex I. The relief is considerable: no DDS, no risk assessment, no geolocation obligation for the leather delivery. The logic of the by-product and the separate value chain is responsible here.

Coffee importer with instant range

An importer brings roasted beans (always in scope) and soluble coffee (HS 2101 11 00) onto the market. Due diligence is already underway for the beans. With the delegated act, he must extend it to soluble coffee, including traceability of the beans used back to the cultivation area.

Economic classification

The Commission expects that the entire simplification package, including the changes introduced by the delegated act, will reduce the annual compliance costs for affected companies by around 75%. At the same time, the environmental protection measures of the EUDR are expected to generate annual economic benefits of around €7 billion by avoiding 208,000 hectares of deforestation and 49 million tons of greenhouse gas emissions.

The Commission will also introduce two new directories: one for relevant legislation in the producing countries and one for certification systems. Both are intended to facilitate access to proof of legality.

Practical consequences for importers and system users

Two points are particularly relevant for affected companies.

- Firstly, Article 7 EUDR creates a double operator situation for imports from third countries: If a company based outside the EU places relevant products on the EU market, the first natural or legal person based in the EU who makes these products available on the market is also deemed to be an operator with full due diligence obligations. Both must carry out due diligence independently of each other and submit a DDS. The background to this is the consideration that there must be an operator in every EU supply chain who can be held liable for violations within the EU. For import structures with group companies outside the EU, this means twice the effort, but also reliable accountability.

- Secondly, it is worth taking a look at the key functions of the EUDR information system (TRACES NT), which will go live again in the second half of the year following updates in the first half of 2026. A DDS can cover several physical consignments and remains usable for a maximum of one year from submission, but only for products that have already been produced or harvested, not for purely planned deliveries. DDSs and simplified declarations can be changed or withdrawn up to 72 hours after the reference number has been assigned, as long as they have not yet been used in a customs declaration. Submission is made manually via the TRACES web interface or automatically via API, geodata exclusively in GeoJSON format (WGS-84/EPSG-4326). The maximum file size is 25 MB, which covers over one million geopoints.

Schedule

The next steps are clear. The public consultation on the draft delegated act will run until June 1, 2026. In the first half of 2026, the EUDR information system will be temporarily closed so that necessary updates can be installed; the reopening with new functions is planned for June 2026. From December 30, 2026, the EUDR will apply in full to large and medium-sized companies, and from June 30, 2027 also to micro and small enterprises.

Important special rule: Micro and small companies that were already covered by the previous EU Timber Regulation (EUTR) must already comply with the EUDR obligations for timber products by December 30, 2026, i.e. by the same date as large and medium-sized companies. The extended deadline of June 30, 2027 only applies to these companies for products made from other raw materials.

The entry into force of the delegated act itself is linked in the draft to publication in the Official Journal of the EU; it does not provide for a transitional period. This is a tight timeframe for companies that are included in the scope for the first time as a result of the new additions, such as importers of soluble coffee or certain palm oil derivatives.

Conclusion

The Delegated Act 2026 is not a fundamental reform of the EUDR, but it shifts the scope in several important places. Anyone involved in soluble coffee, frozen beef tongues or palm oil oleochemicals should check the HS code mapping now, with the note "probably" pending publication in the Official Journal. Conversely, leather processors and manufacturers of retreaded tires can look forward to noticeable relief. And all companies will benefit from the clarifications on packaging, samples, marketing material and correspondence - they create certainty of interpretation where the EUDR had previously left room for interpretation.

Next steps: Update HS code mapping, prepare supplier communication for the newly included codes, adapt DDS templates, keep an eye on publication in the Official Journal and keep the Commission's EUDR FAQ (version 5, April 2026) to hand as an interpretation aid.

Frequently asked questions

The "ex" indicates that only an excerpt of the product group is included. Not all seats fall under "ex 9401", but only wooden seats. Under "ex 0102", only cattle of the genus Bos and its subgenera are included, not buffalo or bison. The "ex" is therefore an important filter criterion for HS code mapping.

No. The regulation only applies to cattle of the genus Bos (subgenera Bos, Bibos, Novibos, Poephagus). Buffalo(Syncerus) and bison(Bison) are not covered.

The due diligence only has to be fulfilled for the proportion of the seven relevant raw materials. A tire made of natural rubber and synthetic rubber is only tested for the natural rubber portion. If non-compliant parts cannot be clearly delimited, the entire product is considered non-compliant - mass balance is expressly not permitted.

Packaging that serves solely to support, protect or carry is excluded - including reusable and non-wooden packaging. It is only covered if it is placed on the market independently (e.g. new sale of pallets) or if used packaging is repaired with new wooden components; in the case of repair, only for the new components.

No. Bamboo, rattan, reed, rushes, willow reed, raffia, cleaned/bleached/dyed cereal straw and lime bark are not included in the wood scope, even if they are classified under a wood-related HS code.

Although these fatty acids were tested, the cost-benefit analysis was negative - the estimated compliance costs exceeded the expected environmental benefits. The same applies to acyclic polyamines (2921 29 00).

As of May 2026, only the draft is available; the public consultation runs until June 1, 2026. The amendments will only become binding upon publication in the Official Journal of the EU. The draft does not provide for a transitional period.

Alexander Hilmar

LinkedInESG compliance expert - lawcode GmbH

Alexander Hilmar advises companies on the implementation of ESG compliance, sustainable reporting and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.