Important facts

- What are the objectives of the EU Omnibus Directive?

- It is intended to simplify ESG rules, reduce the burden on companies and at the same time maintain the objectives of the Green Deal.

- What concrete benefits does it bring?

- The obligations are concentrated more on very large companies, deadlines are postponed and individual requirements are simplified.

- How do the obligations differ depending on the size of the company?

- Very large companies in particular remain in focus. Many SMEs and smaller companies benefit from reduced or voluntary reporting obligations.

- What deadlines are important now?

- For the newly defined CSRD, the reporting obligation will generally begin in 2027, the CSDDD will apply from 2029, and CBAM has already been in force in the definitive regime since January 1, 2026.

- How should companies use the extra time?

- They should now set up data structures, responsibilities, controls and their ESG management properly.

Summary

The EU Omnibus Directive brings new structure to European sustainability regulation. The course remains the same, but many requirements are being reorganized: Reporting obligations focus more on very large companies, deadlines are adjusted and requirements in the CSRD, EU taxonomy, CSDD and CBAM are made more practical.

Essentially, the CSRD applies to fewer companies, companies are given more time for implementation and the CSDDD focuses more on very large companies. In addition, since January 1, 2026, CBAM is no longer just a preparatory topic, but will be applied in practice. The EU taxonomy also remains important, but is to be applied more simply and appropriately.

For many companies, this primarily means more clarity, more planning scope and noticeable relief. It remains crucial to use the time gained to structure data, responsibilities and processes.

Never miss an update on CSRD or CSDDD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

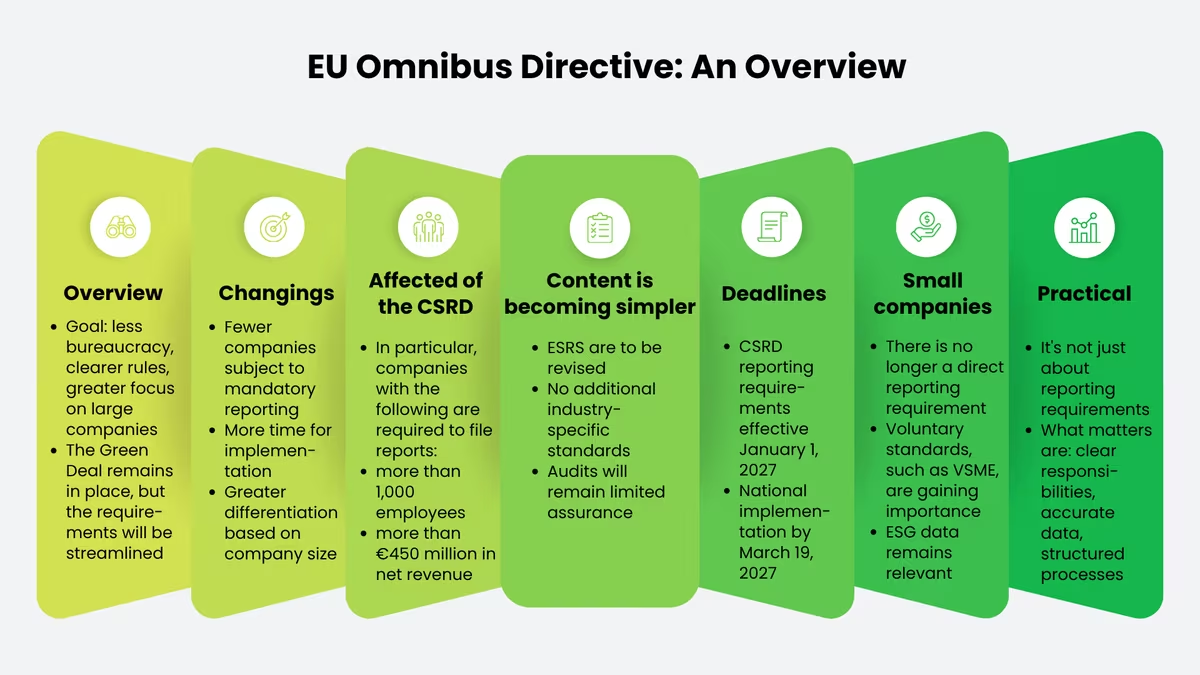

EU Omnibus Directive at a glance

With the EU Omnibus Package, the EU is reorganizing its sustainability rules. It is not about additional obligations, but about simplification and a clearer focus. Companies are to be relieved of unnecessary burdens and the regulations are to concentrate more on those companies that are particularly large and have a correspondingly strong influence. The direction of the Green Deal will remain the same, but the regulatory framework will become noticeably leaner.

The Omnibus I Directive sends three main signals to companies:

- fewer companies in the mandatory area, especially in the CSRD,

- more time due to postponed application times,

- greater proportionality between very large companies and smaller market participants.

This is particularly relevant for SMEs and corporate groups: Many companies gain time and planning leeway. At the same time, ESG remains a strategic issue because requirements from financing, customer relationships, supply chains and tenders continue to increase regardless of the formal reporting obligation. The time gained should therefore not be seen as a break, but as an opportunity to build up robust data and governance processes in a structured manner.

CSRD: Reporting obligations focus on very large companies

The reform focuses on the realignment of the CSRD. In future, the directive will essentially only cover companies with more than 1,000 employees and a net turnover of more than 450 million euros. This means that the scope of application will be much narrower than in the previous discussion about the general classification of company size. For many SMEs, this means a noticeable reduction in the burden, as they are no longer directly subject to the comprehensive CSRD reporting obligation.

However, the pressure has not completely disappeared for small and medium-sized companies. In many cases, ESG data continues to be requested by customers, investors, banks or reporting groups. The EU Commission wants to limit this so-called trickle-down effect and is relying on a voluntary standard to limit the scope of such information requests. This is particularly relevant for companies with up to 1,000 employees, as it provides a practicable framework for voluntary sustainability information (VSME).

Affected by CSRD:

In future, only companies with more than 1,000 employees and a net turnover of more than 450 million euros.

Deadlines are being reorganized

In addition to the narrower scope of application, the new time logic is one of the most important effects of the omnibus package. For companies that continue to fall within the scope of the CSRD following the new regulation, the reporting obligations will generally begin on January 1, 2027. Member states must transpose the CSRD-related amendments into national law by March 19, 2027. This shifts the focus for many companies from short-term implementation pressure to more structured preparation.

The content is also to be simplified. The EU Commission wants to revise the existing ESRS, dispense with additional industry-specific standards and leave it at the audit with limited assurance. For companies, this means above all: fewer new additional requirements and more manageable reporting overall.

Important facts:

- Reporting obligations start from January 1, 2027

- Member states must transpose the CSRD-related amendments into national law by March 19, 2027.

Requirements will differ more according to company size in future

The new rules are based even more strongly on the size of the company. Binding reporting obligations apply primarily to very large companies. Small and many medium-sized companies, on the other hand, will either be exempt from the obligation altogether or work with voluntary, significantly simpler standards. This reduces the workload without completely losing important information from the supply chain.

In practice, it is therefore not only important whether a company is officially obliged to report. Above all, it is crucial whether ESG data can be provided in a clean, comprehensible and easily usable form in the future. Those who create clear responsibilities now, structure data properly and set up internal processes properly are not only better prepared from a regulatory perspective, but also have an advantage over customers, banks and investors.

Background: Why the EU is making adjustments

The Omnibus I Directive is the EU's response to the growing complexity of sustainability regulation. In a short space of time, several comprehensive sets of regulations have been created in parallel with the CSRD, EU Taxonomy, CSDDD and CBAM. The political objective remains unchanged: Sustainability is to be managed in a binding manner and made transparent. However, the way in which these requirements are introduced and coordinated is being readjusted.

At its core, the omnibus package is therefore not a change of course, but a regulatory readjustment. The EU is sticking to its sustainability goals, but wants to make implementation more coherent, economically viable and administratively manageable.

From the CSRD to the Omnibus I Directive

With the CSRD, the EU fundamentally restructured sustainability reporting. Voluntary frameworks became binding requirements with European reporting standards, auditing obligations and digital preparation. In practice, however, it quickly became apparent that this reform did not work in isolation, but was linked to other ESG requirements. This is precisely where the omnibus package comes in: it aims to reduce overlaps, better coordinate the legal situation and make the regulatory framework more consistent.

Goal: Less bureaucracy, more competitiveness and simplification

With the Omnibus I Directive, the EU Commission is pursuing two main goals: less bureaucracy and more competitiveness for Europe. The sustainability rules should remain effective, but not unnecessarily burden companies with too many parallel requirements, unclear responsibilities and high implementation costs. The aim is therefore not to reduce sustainability, but to make regulation more practicable.

The political decision-making process

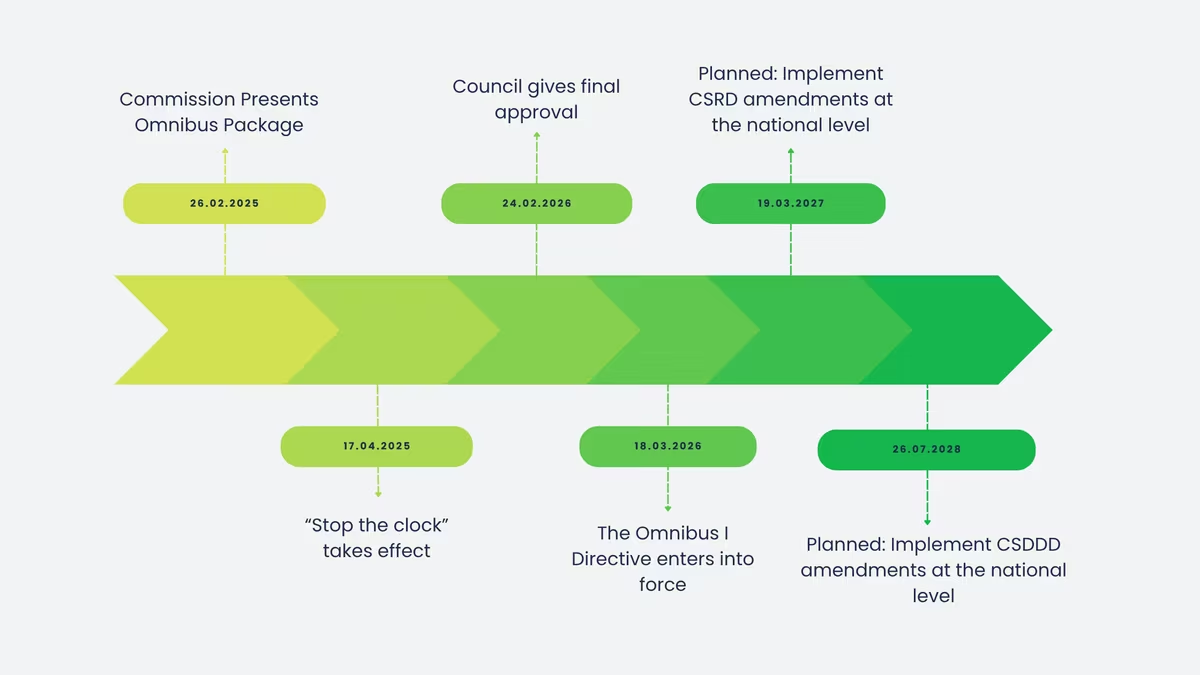

The impetus came from the European Commission's proposal of February 26, 2025, which was followed by the Stop-the-clock Directive, a first step towards easing the timeframe for companies to comply with CSRD and CSDDD. The next step was to negotiate the more far-reaching amendments to the Omnibus I package between the EU institutions.

The package was politically completed with the Council's approval on February 24, 2026. The Omnibus I Directive came into force on March 18, 2026. Since then, the European framework has been set; the main issue now is implementation in the member states. The implementation deadline for the CSRD-related amendments is March 19, 2027, while the deadline for the CSDDD is July 2028.

Core elements of the reform

With the Omnibus Directive, the EU is reorganizing key ESG regulations. What is particularly relevant for companies is which obligations will still apply in future, when they will take effect and how far-reaching the requirements are in practice.

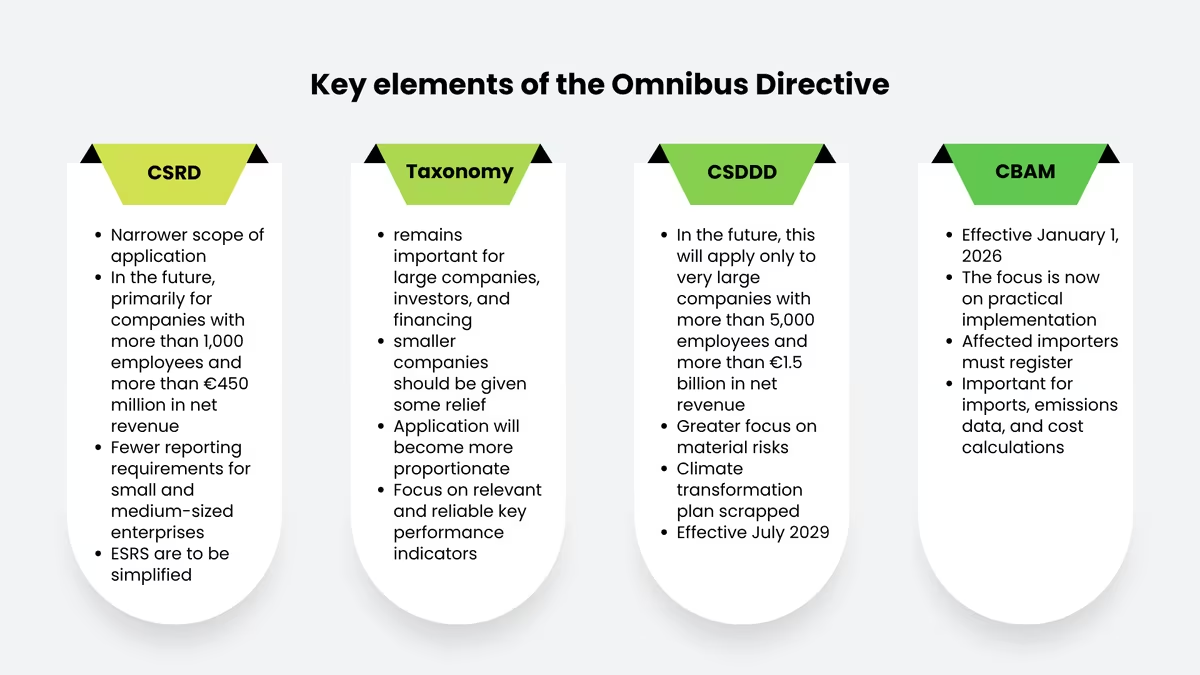

CSRD: narrower scope and leaner reporting logic

The most important aspect of the CSRD reform is the much narrower scope of application. In future, the directive will essentially only cover companies with more than 1,000 employees and a net turnover of more than 450 million euros. New thresholds also apply to third-country companies. This means that sustainability reporting will be more focused on very large companies.

For companies, this primarily means more clarity:

- In future, the CSRD will focus much more strongly on very large companies.

- Many SMEs fall outside the immediate obligation.

- Although smaller companies often remain data-relevant for customers, banks or reporting groups, they should be better protected from excessive information requirements.

The reform also focuses on simplification in terms of content. The Commission's aim is to revise the existing ESRS and limit additional reporting burdens. In practice, this means that companies should not focus their reporting on ever more detailed obligations, but rather on robust core processes - i.e. double materiality, clean data flows, clear responsibilities and audit-proof governance.

EU taxonomy: focus on large companies and proportionate application

The EU taxonomy also remains an important part of sustainability regulation. In future, however, it should primarily apply where the burden on companies is proportionate to their size and importance. The EU Commission therefore wants to significantly reduce the burden on smaller companies and focus reporting obligations more on large market players.

The most important thing in practice is this:

- The taxonomy remains relevant, especially for large companies, investors and financing.

- For smaller and many medium-sized companies, the application is to become more proportionate and partly voluntary.

- The focus is shifting from maximum depth of detail to relevant, reliable and economically usable key figures.

Especially for companies outside the narrower scope of mandatory disclosure, this means that the taxonomy will not disappear, but will more often become a topic of financing, investment planning and cooperation with business partners subject to reporting requirements, rather than a separate, comprehensive disclosure obligation. This practical classification is more helpful for many readers than a purely formal distinction.

CSDDD: Due diligence obligations are limited to very large companies

The limitation of the CSDDD is particularly clear. According to the final version of the Omnibus I package, the directive will only apply to companies with more than 5,000 employees and a net turnover of more than 1.5 billion euros. This means that the CSDDD will focus even more strongly on very large companies, which have the greatest influence on their value chains and are better able to meet the requirements from an organizational perspective.

The content of the directive has also been streamlined. The following points in particular should be emphasized:

- The requirements are more strongly focused on the most probable and significant risks.

- The obligation to draw up a climate transformation plan has been removed.

- The EU-wide harmonized civil liability regime has been removed.

- The upper limit for fines is 3% of global net sales.

The application date has also been postponed. Member states must implement the new rules by July 2028, with application for the companies covered beginning in July 2029. For companies, this means more preparation time, but no loss of importance for the supply chain. Large market players in particular must continue to set up their due diligence systems in such a way that risks can be identified, prioritized and documented.

CBAM: less transition logic, more operational implementation

The focus of the CBAM CO₂ border adjustment system has now shifted. The transition phase is over: CBAM has been in force since January 1, 2026, so for affected importers it is no longer just a matter of preparatory emissions reporting, but of operational implementation in the ongoing import process.

Above all, it is important for companies:

- The CBAM has been in force since January 1, 2026.

- Importers of affected goods must register as authorized CBAM declarants or meet the corresponding requirements.

- The practical implementation runs via the CBAM Registry and the associated reporting and verification obligations.

The relief here comes not primarily from later deadlines, but from clearer rules and simpler requirements for smaller importers. Nevertheless, CBAM remains important for the industry, especially when imports, emissions data and prices are closely linked.

What this means in practice

For companies, the core elements of the reform can be reduced to a simple denominator:

- CSRD and CSDDD are much more focused on very large companies.

- Taxonomy and CBAM remain relevant, but are more strongly oriented towards practical feasibility.

- For many companies, the focus is shifting from direct mandatory reporting to data-capable processes, robust governance and connectable ESG information.

This is precisely the actual effect of the Omnibus I Directive: less formal breadth, but higher requirements for companies that remain in scope and at the same time more pressure on all others to be able to provide ESG data in a structured and professional manner.

Germany: Focus on national implementation

For German companies, the practical impact of the omnibus package will not only be decided at EU level, but above all when it is transposed into national law. The European framework is in place, but the decisive factor is how quickly and in what form the changes are transposed into commercial, auditing and supervisory law. This is particularly relevant for the CSRD because German implementation had already stalled before the omnibus package.

National implementation remains the decisive lever

With the Omnibus I Directive coming into force on March 18, 2026, the European direction has been set. The national implementation deadline for the CSRD-related amendments is March 19, 2027, while the deadline for the CSDDD is July 2028. For German companies, this means that the relief will only take full effect once the new requirements have been incorporated into German law.

At the same time, the situation in Germany remains difficult. Because the CSRD Implementation Act was not passed in time, there is still uncertainty regarding the legal basis, the reporting format and the audit. As a result, many companies are primarily guided by European requirements, drafts and technical recommendations.

"Stop-the-clock" creates breathing space, but no all-clear

The so-called stop-the-clock rule was the first practical relief step of the omnibus package. It was intended to prevent companies from falling under a reporting framework in the short term, only for it to be changed again shortly afterwards. This was particularly important for Germany because the national CSRD implementation had not yet been completed and at the same time many companies had already started preparing the content.

In practice, this primarily means more time for:

- the development of resilient ESG data structures,

- coordination with auditors,

- embedding reporting in the management report and in existing governance processes,

- technical preparation for digital reporting obligations and ESRS requirements.

This breathing space is helpful for companies, but does not replace the actual implementation work. Anyone who remains affected or has to provide data indirectly should use the time to set up resilient processes now.

Questions remain unanswered in Germany

Even after the political agreement at EU level, important detailed questions remain unanswered in Germany. For companies, it is less about the fundamental "whether" and more about the practical "how" of implementation.

Particularly relevant at present are:

- embedding sustainability reporting in the HGB system,

- the delimitation of reporting obligations in groups,

- the organization of auditing and limited assurance.

For companies, this means above all that internal responsibilities, processes and controls must be clearly regulated. In practice, the decisive factor will not only be what data is available, but also whether it can be collected, documented and checked in a traceable manner.

The LkSG remains relevant for German companies

It is also important to note that national regulations such as the Supply Chain Due Diligence Act(LkSG) are not automatically abolished by the omnibus package. Even if the CSDDD has been toned down and postponed at EU level, the LkSG remains an independent frame of reference for the time being. This means that the topic of the supply chain remains practically relevant for many companies, regardless of whether they are later covered by the CSDDD.

Significance for German companies and SMEs

The Omnibus I Directive brings tangible relief for German SMEs in particular. Many companies are exempt from the immediate CSRD obligation or gain additional time. At the same time, ESG data will remain relevant for banks, investors, major customers and reporting groups. Companies should therefore not see the reform as a reason to wait and see, but as an opportunity to prioritize.

It makes particular sense to invest in the following basics now:

- clear data models and clean master data,

- binding responsibilities for ESG topics,

- internal controls for non-financial information,

- close integration with financial reporting, risk management and strategy.

Companies that lay these foundations now will not only improve their compliance capability, but also their management capability. For many German companies, this is precisely where the real added value of the omnibus reform lies: less direct pressure to comply, but more scope to integrate sustainability data into corporate management in a professional and economically sensible manner.

Practical help for reporting

The omnibus package does change deadlines, areas of application and the scope of individual obligations. However, there is little change to the actual task for companies:

- Important topics must continue to be recognized,

- Data cleanly structured and

- sustainability information can be reliably managed.

This is precisely why practical tools and clear methods remain important. Good environmental management, structured reporting tools and a properly conducted double materiality analysis are particularly helpful.

Help for implementation

EMAS enables companies to better organize and reliably record their environmental data. The system helps companies to review, further develop and openly present their own environmental performance. This often results in clearer processes, less resource consumption, more certainty with regard to legal requirements and external monitoring.

EMAS is particularly relevant for sustainability reporting because it is directly linked to ESRS topics in many environmental areas. The European Commission and EFRAG have explicitly identified the synergies between EMAS and ESRS. The interfaces are particularly close in the areas of emissions, water, biodiversity, material use and waste. Companies that already work with a structured environmental management system in these areas often create reliable data paths for their reporting more quickly.

For many companies, the biggest hurdle is not just data collection, but above all the introduction of a consistent reporting logic. This is exactly where the Sustainability Code platform can help. The German Sustainability Code (DNK) offers a free platform that companies can use to create sustainability reports digitally and step-by-step. The platform is now also geared towards voluntary reporting and supports both CSRD-oriented and VSME-oriented reporting approaches.

This is particularly relevant because the European Commission has recommended the VSME standard as a voluntary framework for small and medium-sized enterprises since 2025. The aim is to standardize ESG requests to smaller companies and limit unnecessary multiple requests from supply chains or financial institutions. For many SMEs, this is a sensible way to provide ESG data in a structured but proportionate form.

In addition to official platforms, additional tools can also help to maintain an overview. Solutions such as our module for sustainability and VSME reporting or lawcode's supply chain management help companies to implement requirements more easily and keep a better eye on compliance.

Regardless of tools and platforms, dual materiality remains the central methodological core of sustainability reporting. The CSRD requires companies to consider both the financial impact of sustainability issues on the company and the company's impact on the environment and society. It is precisely this logic that helps to focus reporting and avoid unnecessary depth of detail.

EFRAG has published its own guidelines for practical implementation. It is particularly important for companies not to treat the materiality analysis as an isolated compliance exercise, but as a management tool.

In practice, there is usually a clear three-step process:

- identify relevant topics along the value chain,

- Systematically assess impacts, risks and opportunities,

- Link results with objectives, measures and responsibilities.

Companies that proceed in this way usually not only report more clearly and in a more organized manner. They also create a better basis for internal decisions, priorities and investments. Especially in the current regulatory environment, this is often more helpful than a report that is as long as possible.

Outlook: What companies should do now

The omnibus package brings noticeable relief, but no loss of importance for ESG. Sustainability information remains relevant for many companies. Be it through direct reporting obligations, requirements from banks and investors, expectations of major customers or requirements along the supply chain. The difference is that regulation is more focused on very large companies, deadlines have been reorganized and smaller companies are given more leeway for proportionate preparation.

For companies, this means above all that now is the right time to thoroughly examine their own impact and to set up the reporting architecture in such a way that it can withstand both regulatory requirements and practical market demands. Those who use the additional time wisely will not only create compliance security, but also improve data quality, internal control and decision-making ability.

These dates are currently particularly relevant for business practice:

- Omnibus I in force: since March 18, 2026.

- Implement CSRD amendments into national law: by March 19, 2027.

- Implement CSDDD amendments into national law: by July 2028.

- CBAM definitive phase: in use since January 1, 2026.

This means for planning:

Companies should no longer work with the old CSRD logic, but adapt their roadmap to the new status. The Omnibus I Directive, national implementation, CBAM and possible requirements from financing and the supply chain should be considered together. This is particularly important for corporations and medium-sized company groups in order to realistically plan budgets, IT projects and responsibilities.

In practice, these steps in particular have proven their worth:

Preparatory steps for affected companies

Check which companies are still directly affected by the new thresholds and where there are indirect requirements from group structures, financing or customer relationships.

Material topics should be identified, evaluated and documented in a comprehensible manner. Even with less reporting pressure, this remains the basis for reliable ESG management.

ESG data should be consistent, auditable and compatible with financial reporting, risk management and operational management. It is particularly worthwhile now to streamline master data, responsibilities and interfaces.

Anyone importing affected goods should firmly anchor the registration, verification and process requirements of the definitive CBAM phase in purchasing, customs and product costing.

Even with a more proportionate regime, it remains crucial that data, processes and controls are documented in a comprehensible manner. This applies in particular to companies that remain in scope or have to supply as part of a group.

Practical tips for implementation

For many companies, a pragmatic start makes more sense than immediately setting up a highly complex ESG system.

In practice, this is particularly helpful:

- to start with a few reliable core KPIs,

- Clearly define responsibilities between sustainability, finance, legal and IT,

- standardize supplier and customer queries at an early stage,

- and to closely link its own ESG roadmap with budget, risk and investment planning.

SMEs in particular benefit from relying on robust but lean structures now. Because even where the formal reporting obligation no longer applies or comes into effect later, ESG data remains an important topic in tenders, financing and business relationships. Those who make orderly preparations today will avoid hectic retrofitting later.

Conclusion

The EU omnibus package brings tangible relief without changing the direction of sustainability regulation. Reporting obligations are concentrated more on very large companies, deadlines are reorganized and individual requirements are made more practicable. For companies, this means more time and more clarity - but no reason to postpone ESG issues. Those who use the time they have gained to properly establish data, responsibilities and processes will not only create regulatory certainty, but also strengthen their own competitiveness

Frequently asked questions

No, not in every practical detail. Although the European legal framework has already been adopted, many of its effects depend on when and how the member states transpose the changes into national law. For companies, this means that the European direction is clear, but the concrete application in everyday life can take shape at different speeds depending on the country and national legislation. In Germany in particular, it is therefore important to look not only at Brussels, but also at national implementation in commercial, auditing and supervisory law.

Usually not. Even if the formal reporting obligation no longer applies or applies later, sustainability information remains relevant in many cases. Banks request ESG data in the context of financing, large customers expect information from the supply chain and reporting groups require data from their subsidiaries or business partners. For many companies, the topic is therefore shifting from a direct statutory reporting obligation to an indirect market requirement.

Because ESG is no longer just a regulatory issue. Today, sustainability information also plays an important role in tenders, customer requirements, financing discussions, supplier evaluations and investment decisions. Although SMEs often benefit from the fact that they are no longer directly subject to mandatory reporting, the expectation of being able to provide relevant data in a structured and comprehensible manner is also increasing. The relief therefore reduces the formal pressure, but does not take away the economic relevance of the topic.

A big one. Especially where companies are no longer required to report directly by law, requirements often come via the market. Banks want to better understand how sustainable a company is positioned, investors pay attention to risks and transformability, and large customers need ESG data for their own reporting or supply chain management. For many companies, it is therefore becoming crucial not only to possess information, but also to provide it in a form that is plausible, consistent and connectable.

In groups, the data issue usually remains more complex than the pure individual company perspective would suggest. Even if individual subsidiaries are not required to report on their own, they may still have to provide relevant data at group level. This applies in particular to emissions, personnel and social data, supply chain information or taxonomy-relevant key figures. For corporate groups, this means that reducing the burden at individual unit level does not automatically reduce the need for clean data structures across the group.

Sustainability reporting is not a task that a single specialist department can solve alone. In practice, several departments usually have to work together, especially sustainability, finance, legal, IT, purchasing, risk management and, depending on the business model, product management or HR. The reason is simple: ESG data is generated at very different points in the company, but must ultimately be consistently merged, evaluated and documented. The earlier these responsibilities are clearly defined, the more robust the subsequent process will be.

This can be useful as an introduction, but it is usually not enough as a permanent solution. Individual key figures such as energy consumption, emissions or supplier structure do help to create initial transparency. However, reliable reporting and control depend on how this data is collected, documented, checked and integrated into decisions. Without clear responsibilities, standardized definitions and comprehensible processes, a patchwork quilt is quickly created that later has to be corrected at great expense.

A common mistake is to confuse relief with the all-clear. If you do nothing now, you risk hectic reworking later when data is needed at short notice. It is equally problematic to treat ESG in isolation as a pure reporting issue. Sustainability information should be dovetailed with controlling, risk management, governance and operational processes as early as possible. Overly complex solutions at the beginning can also be a hindrance - it is often better to start with a clear, pragmatic structure and then gradually expand it.

Companies that are part of a group, work closely with large customers, purchase internationally or have an emissions-intensive business model should act at an early stage. ESG data also often plays an important role in tenders. Even if a company's own reporting obligation decreases, such information is still needed in many cases. Early preparation is therefore particularly worthwhile for companies with more complex structures and supply chains.

The most important first step is a thorough impact analysis. Companies should first clarify which regulations affect them directly, where indirect requirements arise and which units within the company or group have to provide relevant data. Based on this, it is possible to check which data is already available, where there are gaps and which responsibilities need to be regulated internally. If you take this step properly, you create the basis for everything else - from materiality analysis and data architecture to governance and audit assurance.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.