Important facts

- Does the EUDR also apply to self-consumption in the company?

- Yes, anyone who imports EUDR-relevant products commercially and releases them for free circulation is subject to the Regulation, regardless of whether the goods are resold or only intended for internal use.

- What counts as "placing on the market" within the meaning of the EUDR?

- Placing on the market is the first making available of a relevant product for distribution, consumption or use on the Union market in the context of a commercial activity, in the case of imports usually after release for free circulation.

- Do companies also have to submit a due diligence statement for their own imports?

- Yes, a DDS is also required if EUDR-relevant products are imported from a third country without being resold.

- Are there exceptions for purchases within the EU?

- For purchases within the EU, a new DDS does not have to be created if the product has already been placed on the market with a DDS, but storage and transfer obligations as well as additional obligations for non-SME traders remain in place.

- What happens in the case of transit or direct export without use in the EU?

- In the case of pure transit or storage under certain customs procedures, the product is not considered to have been placed on the market; EUDR obligations only arise when the product is released for free circulation or exported from the EU.

Executive Summary

The EUDR affects more companies than initially expected. It applies not only to traditional trade transactions, but also to own imports and in-house consumption, such as for canteens, production or training. The decisive factor is whether a relevant product is made available on the EU market for the first time as part of a commercial activity. Private use is not covered.

The obligations depend on the role: the initial distributor must carry out due diligence and submit a DDS. Downstream actors generally do not have to prepare a new DDS, but remain subject to documentation and information obligations. Pure transit without release for free circulation is generally exempt; export constellations are critical, as EUDR obligations can arise both when placing on the market and exporting. In order to minimize liability risks, a risk-based approach with clear responsibilities, systematic documentation and close involvement of the compliance and legal departments is recommended.

Never miss an update on the EUDR again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

When does the EUDR Regulation apply?

The EUDR does not only apply to traditional retailers and producers

Numerous companies are currently finding that they are considered market participants within the meaning of the EUDR, even though they are neither traditional traders nor primary producers. Particularly in the case of intra-group uses, service providers with their own imports and independent operating sites, there is a lack of clarity:

- When is something considered "placing on the market"?

- Does the due diligence declaration (DDS) also have to be followed for own use of raw materials or own materials?

The relevance of these questions is increasing due to the threat of sanctions and the expectations of business partners. Particularly in sectors such as production, food processing, office supplies or packaging, uncertainties regularly arise: when is an intra-group or internal use subject to EUDR despite own use (because commercial activity / free movement) and when is a non-commercial case outside the scope of application?

Similar questions arise when exporting outside the EU or importing for special projects. The internal purpose is less relevant for classification than whether and when a product is made available on the EU market for the first time as part of a commercial activity; in the case of imports, this is typically only after release for free circulation.

EU Deforestation Regulation: you can find the complete overview here.

What does "placing on the market" mean according to the EUDR?

"Placing on the market" is the first making available on the Union market in the context of a commercial activity. Even without sale (e.g. import for internal use only), this may be covered. Private use and consumption, on the other hand, are not covered. This means that even if a company only imports raw materials for its own use, for example for the canteen or production, this can already be considered "placing on the market" according to the EUDR. And if a product is imported from a non-EU country for own use, the EUDR regulations apply as normal.

In the case of EU purchases, no new DDS is usually created if a valid DDS already exists. However, depending on the role (trader, downstream operator), documentation and disclosure obligations remain. Since the changes at the end of 2025 (including the introduction of the 'downstream operator'), the delimitation of roles along the supply chain has become even more important.

"Placing on the market" means the first making available of an EUDR-relevant product on the Union market in the context of a commercial activity, irrespective of whether the product is sold or only used internally.

The legal basis is Article 2(16) and (18) of the EUDR, which deliberately define the term broadly. Accordingly, "placing on the market" also includes cases in which products are imported into the EU internal market for own use, internal processing or packaging. The regulation makes no distinction between commercial goods and internal use. The only decisive factor is that the product gains access to the EU market for the first time. Companies that have so far concentrated exclusively on internal company use often underestimate the scope of the regulation and therefore also their obligations to carry out due diligence.

Trade associations such as the Association of German Chambers of Industry and Commerce (DIHK) and consulting firms such as PwC expressly point this out in their interpretations: In-house consumption and intra-group transfers can also be considered "placing on the market" if they lead to the first making available on the EU market. The consequence: Due diligence obligations apply regardless of the intended use or planned further processing.

Where is the line between private and commercial?

The EUDR explicitly excludes private use from the scope of application - but the regulation itself does not specify where exactly the boundary between private and commercial lies. The FAQ version 5 published in April 2026 (point 3.16) now provides concrete indications for the first time.

The decisive factor is a case-by-case assessment by the authorities and customs, which is primarily based on two criteria: Quantity and frequency. A self-classification of the importer as "private" is therefore not sufficient - the decisive factor is whether the circumstances as a whole plausibly indicate private use.

Clearly private (C2C - not recorded):

- A person brings back a reasonable quantity of relevant products for their own use after a vacation outside the EU (no resale).

- A person in a third country sends products to a private individual in the EU, for example as a parcel between relatives.

Not private (covered by EUDR):

- B2C online orders from a third country: Here, a company delivers the goods - even if the end customer is a private individual and is listed as the "importer" on the customs declaration. The operator is the supplying supplier, not the consumer.

- Unusually large quantities or regularly recurring purchases, even if the formal term "personal use" is used.

- Any internal company consumption - regardless of whether the goods are sold or used exclusively internally. The company acts as part of a commercial activity, not as a private individual.

This makes it clear that "private" in the sense of the EUDR means exclusively consumer-to-consumer - person-to-person without a business context. As soon as a company is involved in the process, either as a supplier or as a recipient for its own operations, the regulation applies. The following section shows what this means in concrete terms for internal use.

Internal use may also be subject to EUDR

The EUDR does not differentiate between sale and internal use, but whether a product is made available on the EU market for the first time as part of a commercial activity. There is no privileged treatment of internal use. The only decisive factor is whether and when the raw material or product is made available on the Union market for the first time - in the case of imports, typically after release for free circulation.

This means that even if a company imports an EUDR-relevant raw material, such as wood, leather, cocoa or soy, exclusively for its own operations from a non-EU country, this may already fall under the regulation.

Typical cases, if import or first provision in the context of a commercial activity:

- Imports for technical trials or model production

- Use of materials for internal training or testing processes

- Use of products as office or laboratory equipment

- Procurement for own use, e.g. in canteens or for internal company events

All of these scenarios can be considered "placing on the market" within the meaning of the EUDR, even if the products are never placed on the free market. This shows that The regulation does not privilege internal use, but consistently focuses on the first market access within the EU.

This harbors considerable risks: Companies that do not provide clarity here not only expose themselves to possible fines, but also risk reputational damage and exclusion from supply chains if they do not comply with EUDR requirements.

The central recommendation is therefore: Every first-time provision of an EUDR-relevant product on the EU market, regardless of the intended use, must be checked to see whether the due diligence obligations of the EUDR apply. This is the only way to minimize legal risks and ensure the trust of partners and authorities.

Own consumption of paper, coffee or cocoa

Companies often import everyday materials such as paper, coffee or cocoa exclusively for their own use. Many companies assume that the EUDR does not apply in these cases. However, a closer look at the regulation and its interpretation shows that EUDR obligations can be triggered when importing from a third country (especially after release for free circulation). In the case of EU-related goods, documentation/evidence obligations apply depending on the role. A separate DDS is often not required.

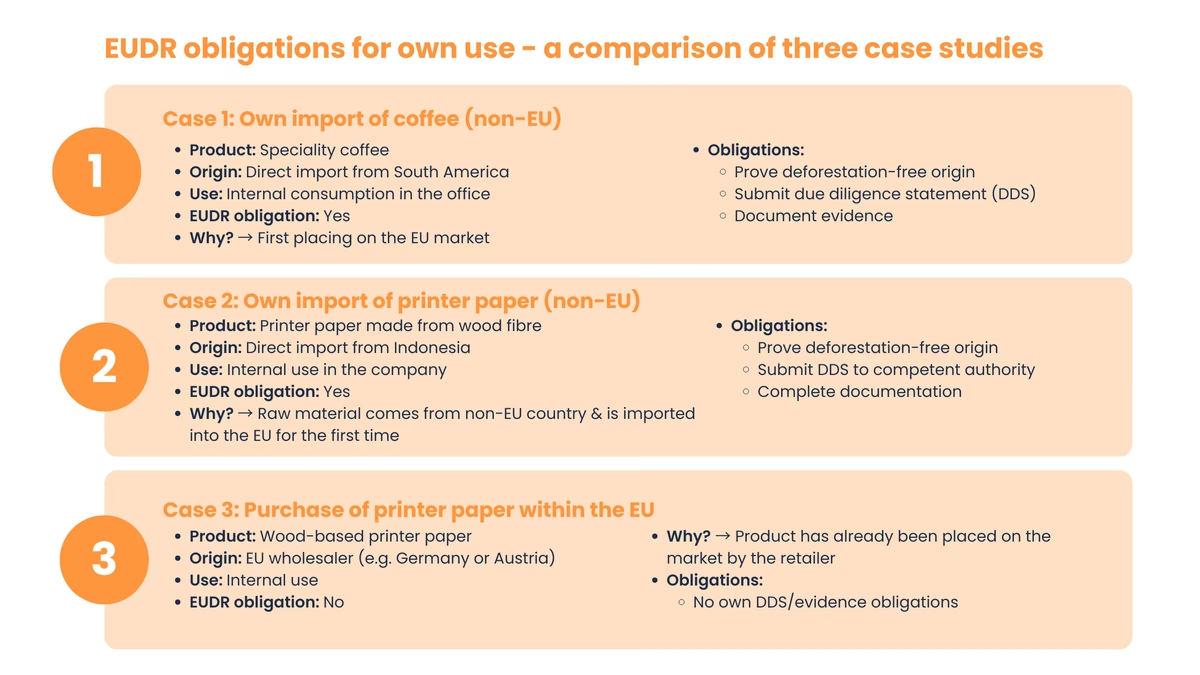

Case study 1: What applies to own consumption of imported coffee?

A medium-sized software company regularly purchases specialty coffee directly from a coffee farm in South America. The coffee is imported exclusively for the company's own use, as it is distributed to employees in the office and not sold on. Despite the purely internal purpose of use, the EUDR applies here. With the import from a third country, the coffee is made available on the EU internal market for the first time and is therefore considered to be "placed on the market" within the meaning of the regulation. The fact that the coffee is not sold is irrelevant. The decisive factor is the first making available in the context of a commercial activity. Private use or consumption, on the other hand, is not covered.

The company must therefore:

- prove that the coffee was produced without deforestation and in compliance with the law

- submit a due diligence statement

- document the necessary records and checks

Other own imports from non-EU countries, e.g. cocoa, palm oil products or packaging materials made of wood, are also subject to the same obligations, regardless of their intended use in the company.

Case study 2: What applies to own consumption of imported printing material?

An industrial company imports printer paper directly from a manufacturer in Indonesia. The paper is used exclusively within the company, for example for internal communication, documentation and accounting. The paper is therefore not sold. Despite the purely internal use, the EUDR also applies in this case. The printer paper consists of wood-based fibers, one of the seven raw materials covered by the regulation. When the product is imported from a third country, it is placed on the EU internal market for the first time and is therefore considered to be "placed on the market" within the meaning of the EUDR.

This means for the company:

- It must prove that the paper comes from deforestation-free and legally compliant sources

- it must submit a complete Due Diligence Statement (DDS) to the competent authority

- it must carefully document all relevant evidence

The fact that the paper is only used within the company does not change the due diligence obligation. Only the first market access within the EU is decisive - not how or by whom the product is subsequently used. Printer paper can be a relevant product (depending on the CN/HS Code according to Annex I, often Chapter 47/48).

Case study 3: What applies when purchasing printer paper within the EU?

The situation is different for a company that purchases printer paper from a European retailer. Even if the paper is wood-based, it is purchased within the EU internal market, for example via a wholesaler in Germany or Austria. In this case, the EUDR no longer applies, as the paper has already been placed on the market by the retailer. The company is therefore not a "market participant" within the meaning of the EUDR, but merely a downstream user. In the case of EU-related goods, a separate DDS is usually not necessary if the goods have already been placed on the market with a DDS. Depending on the role, however, there are still documentation/verification or reference obligations (trader/downstream operator).

Important: The distinction is therefore not in the purpose of use (e.g. own use), but in the place and time of first placing on the EU market.

Self-consumption does not protect against obligations - market access counts

The EUDR assesses the first placing on the EU market. Whether for sale or internal use: the decisive factor is the first making available in the context of a commercial activity - in the case of imports, regularly after release for free circulation. The same logic applies to pure rental: not covered within the EU without transfer of ownership - but very much covered when importing or exporting, even if the product is subsequently only rented out.

The following therefore applies:

→ Imports from third countries may also be subject to EUDR for purely internal use if they are made available on the Union market for the first time as part of a commercial activity (typically: after release for free circulation).

→ EU purchases usually do not require their own DDS if the product has already been placed on the market by a first operator with DDS. Depending on the role, however, there are still documentation and reference number obligations (downstream operator/trader).

Even if the import is declared as "own consumption", the verification and documentation requirements remain high. However, whether a separate DDS must be submitted depends on the role (first operator vs. downstream/trader). Experts therefore advise that all processes relating to import, own use and documentation should be closely coordinated with the legal department and compliance. The same also applies to technical materials made of wood, cardboard packaging or other EUDR raw materials that are used for internal operations, production or facility management.

Special case of letting: when ownership is not transferred

One constellation that is often overlooked in practice is the pure rental of relevant products. A separate logic applies here: renting within the EU is not placing on the market, as there is no transfer of ownership. The EUDR presupposes a "making available" in the context of a commercial activity for its obligations and this is typically linked to the transfer of ownership.

However, the flip side is crucial: as soon as the rented goods are imported into the EU from a third country or exported from the EU, the EUDR applies in full - even if the subsequent use consists exclusively of renting. Market access remains the triggering moment, regardless of whether the product is later sold or "only" leased.

Brief example: A furniture rental company that rents out furniture that has already been cleared through customs within the EU is not subject to the EUDR - no transfer of ownership, no obligation. However, if the same rental company imports furniture directly from Indonesia for its stock or exports it to a partner outside the EU, the regulation applies in full - including due diligence and DDS levy. This does not change the fact that the furniture is then only rented out and never sold.

The logic is therefore the same as for self-consumption: it is not the intended use after market access that is decisive, but the market access itself.

Export and sales within and outside the EU

The situation is often even more complex when raw materials or products made from them are both sold within the EU and exported to third countries. The question of whether the EUDR obligations also apply to exports to non-EU countries and the clear delineation of what counts as "placing on the market" within the EU is therefore highly relevant for internationally active companies.

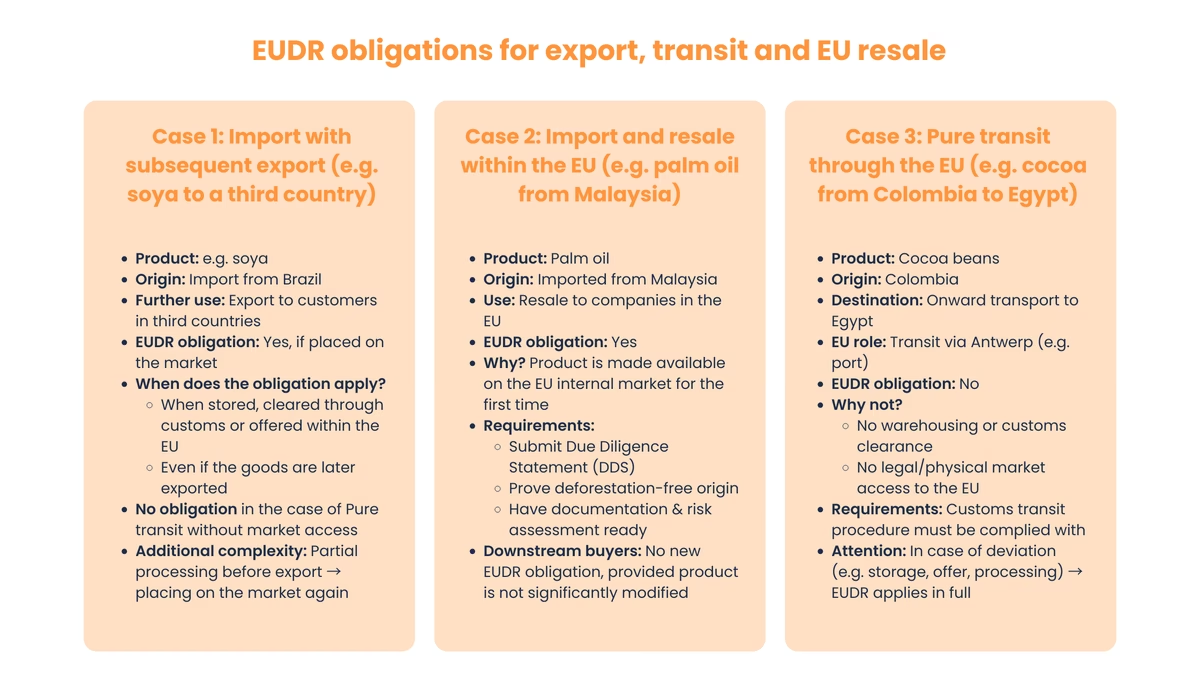

Case study 1: Does the EUDR also apply to exports to non-EU countries?

The EUDR is geared towards the EU internal market, but export scenarios can also trigger EUDR obligations under certain conditions. An internationally active trading company imports an EUDR-relevant product, for example soy from Brazil, to Germany. The product is not used or sold domestically, but is to be exported directly to a customer in a third country. The central question is: Does a due diligence check in accordance with EUDR also have to be carried out in this case, even though no domestic distribution is planned? EUDR obligations arise either when a relevant product is placed on the market for the first time or when it is exported from the EU - depending on which action is involved. According to the EUDR, the regulation only applies when a product is made available on the EU market for the first time.

This means:

- If the goods are only transported through the EU (e.g. in transit), there are no EUDR obligations.

- Pure transit or special customs procedures (e.g. bonded warehouse, inward processing) do not typically trigger a release for free circulation. The release for free circulation or, alternatively, an export process is usually decisive.

At this point, the due diligence obligations apply in full. The company must then carry out a full due diligence check and submit a DDS (Due Diligence Statement), even if the product is subsequently exported to a third country.

It becomes even more complex if the imported goods are first partially processed or repackaged before they are partially or completely exported outside the EU. We would like to illustrate this with an example: a raw material is converted into a semi-finished product in the EU and is then partially exported, while another part is further processed or sold internally. Not every internal step is a new placing on the market. New obligations arise in particular when a new relevant product is created through processing and this is subsequently placed on the market or exported.

Special case of dual role: A single legal entity can take on both roles at the same time - operator during import and downstream operator during subsequent processing. Example: Company A imports raw timber (operator role with full due diligence and DDS), processes it into sawn timber in its own company and sells it on to a furniture manufacturer (downstream operator role). DDS reference numbers do not have to be passed on within the same legal entity - they are available in the same company anyway. This constellation is particularly important for integrated companies with their own processing: both roles must be properly documented, even if the formal step of passing on reference numbers is omitted.

In the case of pure transit or direct export without placing on the market, no EUDR obligations must be complied with. However, if the product is stored, processed or offered in the EU, the EUDR obligations apply in full. Companies with international supply chains should therefore carefully examine their import, storage and export processes and work closely with customs, logistics and compliance, particularly in the case of intermediate solutions.

Case study 2: Does the EUDR apply if goods are imported from a non-EU country and then resold in the EU?

A wholesaler based in France imports palm oil directly from a producer in Malaysia. The goods are cleared through customs in France, stored in a warehouse and then sold on to various processing companies within the EU, for example in Belgium and Italy. In this case, the EUDR obligations clearly apply. This is because when the palm oil is imported from a third country and then made available on the EU internal market, the goods are deemed to have been "placed on the market" within the meaning of the regulation.

This means:

- The trader in France is a "market participant" within the meaning of the EUDR

- He is obliged to carry out a complete due diligence review

- A Due Diligence Statement (DDS) must be uploaded to the EU information system prior to import

- They must provide clear evidence that the palm oil was produced without deforestation and in compliance with the law

- The documentation and risk assessment must be able to be presented at the request of the authorities

When reselling within the EU, a new DDS is generally not required if a valid DDS from the first operator is available. Depending on the role, however, documentation or reference number obligations remain (downstream operator, trader). The prerequisite is that the product does not change significantly and a valid Due Diligence Statement (DDS) is available. The obligation lies with the first distributor.

The EUDR applies without restriction to imports from third countries with subsequent marketing within the EU. This applies regardless of whether the sale is made to end consumers, processors or other traders. Companies that are the first to import raw materials or affected products into the EU market are responsible for complying with all due diligence obligations.

Case study 3: Does the EUDR apply to pure transit through the EU?

A trading company from Switzerland organizes the transport of cocoa beans from the Ivory Coast to a customer in Egypt. The goods are imported into the EU via a port in Antwerp (Belgium), but are not stored or cleared through customs. Instead, they merely pass through EU territory as part of a customs transit procedure and are then exported on to Egypt by ship. In this case, the EUDR does not apply as long as the goods remain under transit or other special procedures and are not released for free circulation. There is no placing on the market within the meaning of the Regulation. The cocoa beans are neither sold, processed, nor used or offered internally, but merely transported onwards.

This means:

- There is no obligation to conduct a due diligence review.

- A Due Diligence Statement (DDS) is not required.

- The proof requirements of the EUDR also no longer apply.

However, it is important that the requirements of the customs transit procedure are clearly met. As soon as the goods are temporarily stored in the EU, cleared or made accessible to the internal market in any form, for example through internal processing or offering to customers, the EUDR would apply in full.

EUDR applies to placing on the market - not to pure transit

EUDR obligations can arise when products are placed on the market or exported from the EU; pure transit is generally not covered. It is irrelevant whether the product is subsequently sold, processed or exported. If a product is only transported through the EU, for example as part of a transit procedure, there is no EUDR obligation. The situation is different if the goods are released for free circulation or made available on the EU market or if a new relevant product is created through processing that is subsequently placed on the market or exported: in this case, the due diligence obligations apply in full. Due diligence is also required for intermediate solutions with downstream export as soon as the product has previously been made available on the internal market.

Re-import: When exported goods return to the EU

A constellation of particular practical relevance arises when products are first exported from the EU, further processed or temporarily stored in a third country and then re-imported into the EU.

A classic example: An EU manufacturer exports chipboard to Norway, where it is used to make furniture that is later returned to the EU. The key question is: does a full due diligence check have to be carried out again in this case, or is the reference to the original placing on the market sufficient?

The basic rule: downstream operator instead of full readjustment

The Commission's answer is clear: anyone who re-imports a product that has demonstrably already been carefully placed on the Union market and subsequently exported is not considered a new operator, but a downstream operator. This also expressly applies if the goods have been further processed in a third country, provided that the relevant components were previously covered by a DDS.

As a result, the re-importer does not have to carry out its own due diligence and does not have to submit a new DDS. Instead, they can use a conventional reference number in the customs declaration, in the format 99EU999999999999. The obligations are limited to being able to prove to the competent authorities on request that the product was actually previously placed on the EU market and exported from there.

The flip side is important: if the earlier placing on the market cannot be proven, the product is deemed to have been imported into the EU for the first time. This means that the full operator obligation applies, including due diligence, risk assessment and DDS submission. The paper trail therefore directly determines the burden of duty.

Case study 1: Chipboard from the EU, furniture from a third country

A German forest owner cuts wood in his own forest and delivers it to an EU manufacturing company, which uses it to produce chipboard and markets it properly with DDS. The chipboard is then exported to a furniture manufacturer in Switzerland, which uses it to produce seating furniture. This furniture is later brought back into the EU by a German importer and resold domestically.

In this constellation, the German importer is considered the downstream operator. Prerequisite: He can provide full proof that the chipboard used in the furniture was previously placed on the EU market with DDS. If this proof is available, the conventional reference number 99EU999999999999 is sufficient in the customs declaration. A separate due diligence check is not required, as the due diligence obligation has already been fulfilled by the original EU operator.

Important: If the returned furniture also contains components that do not originate from the original EU export (such as wood parts from third country sources), a full due diligence check must be carried out for these components.

Case study 2: Re-import without supporting documents - the full obligation applies

A trading company imports cocoa products from Turkey which, according to the supplier, were originally made from EU cocoa. However, the supplier is unable to provide concrete evidence - such as customs declarations for the original export, supply chain documents or invoices linking the origin of the cocoa back to the time it was placed on the EU market.

In this case, the conventional reference number does not apply. Without reliable proof of previous placing on the market, the product is legally deemed to have been imported into the EU for the first time. The importer thus becomes an operator within the meaning of the EUDR and must:

- carry out a full due diligence check,

- submit their own DDS to the EU information system,

- prove that all components are deforestation-free and legally compliant,

- Document risk assessment and, if necessary, risk mitigation measures.

The supposed "re-import" is therefore in fact a fully-fledged first import with all the associated obligations and liability risks.

Which proofs are accepted

The Commission accepts a wide range of supporting documents, provided they can be clearly assigned to the specific product. In particular, the following are eligible

- Customs declarations of the original export and the current re-import

- Contracts between the parties involved, even if the re-importer itself was not a party to the contract

- Order documents and order confirmations

- Delivery bills and shipping documents

- Freight documents: CMR (road transport), Bill of Lading (sea transport), Air-Way-Bill (air transport)

- Invoices along the entire transport chain

- any other credible documentation that establishes a direct link to the relevant product

The decisive factor is not the form, but the traceability: the authority must be able to reconstruct the "placing on the market in the EU → export → re-import" chain without gaps on the basis of the documents. Blanket statements of origin or supplier assurances are not sufficient.

Re-import is not a new placing on the market - if the paper trail is in place. Anyone who can fully document the previous EU placing on the market is a downstream operator and works with the conventional reference number 99EU999999999999. Those who cannot are operators with full DDS obligations. The verification process determines the company's role at customs.

Recommendations for action

Companies should check all imported and circulated raw materials for their EUDR relevance, regardless of their intended use. A role-based analysis is particularly recommended for complex groups of companies in which several legal entities, subsidiaries or permanent establishments are involved in the movement of goods. The key question here is always: When will the first entry or export of relevant products from the EU take place - and in which role (first operator vs. downstream/trader)? Important: According to FAQ 2.10 and 3.15, logistics service providers, freight forwarders and customs representatives are never operators, downstream operators or traders - the EUDR responsibility always remains with the actual market participant, even if the customs declaration is delegated.

And: Does this take place as part of a trade, an intra-group transfer or an alleged own consumption? Only a detailed mapping of all affected flows creates legal certainty and prevents sanctions. In this context, it is advisable to create procedural documentation that documents the risks and obligations along the entire value chain in the form of process manuals, flow charts or supplier audits.

A common mistake is to assume that due diligence obligations only apply to commercial sales. In fact, own use can also be EUDR-relevant. However, whether a separate DDS must be submitted depends on the role (first operator vs. downstream/trader). Downstream operators often have to maintain and pass on DDS references/information. This applies in particular to products that are only used or processed internally after import. Companies should check at an early stage whether their procurement, internal processing or transfer to closed user groups falls within the scope of the EUDR. In addition to the formal creation of a DDS, this also includes setting up processes for supplier verification, risk analysis and verification management. Industry-specific software and templates can reduce the effort involved and enable standardized implementation.

Clear communication about EUDR-compliant processes and obligations is crucial for both external partners and internal stakeholders. Companies should involve purchasing, logistics, production, facility management and internal service providers in the documentation and compliance processes in good time. Securing evidence is becoming more legally relevant due to the potential fines under the EUDR. It is advisable to archive all relevant process steps, decisions and checks electronically in an audit-proof manner and to monitor them regularly through internal audits. An unexpected risk arises, particularly in the case of in-house consumption, as many highly qualified employees are not familiar with the documentation requirements of the EUDR. Finally, open communication with business partners, suppliers and relevant authorities is a must. This is the only way to avoid compliance pitfalls and ensure sustainable, trustworthy supply chain management.

To Do:

→ Systematically analyze all imported raw materials and flows of goods for their EUDR relevance, regardless of their intended use, and document roles, obligations and risks along the entire value chain.

→ Check at an early stage whether own use and internal processing also fall within the EUDR scope of application and ensure that DDS references and all necessary evidence are kept and passed on in full.

→ Involve all relevant internal areas, from purchasing to logistics to facility management, in the compliance processes at an early stage and archive all decisions and checks in an audit-proof manner.

Conclusion

The EUDR goes further than many people think: it applies not only to traditional importers, but also to companies that use EUDR-relevant products exclusively internally, for example in production, canteens or administration. The decisive factor is not the intended use, but whether a product is made available on the EU market for the first time as part of a commercial activity.

The distribution of duties is role-based: The first operator bears the main responsibility for due diligence and DDS, while downstream players remain involved in documentation and information obligations. EUDR obligations may also arise during export, but pure transit remains exempt.

Companies should systematically record their goods flows, clearly assign responsibilities and involve all affected teams at an early stage. Digital, audit-proof documentation is not a nice-to-have, but a key success factor.

Frequently asked questions

Yes, if the company is the first operator to place a relevant product from a third country into free circulation and thus makes it available on the EU market for the first time, it must carry out due diligence and submit a DDS in the EU information system. For purchases within the EU, no new DDS is usually required if a valid DDS already exists, but depending on the role, documentation/reference obligations (downstream/trader) may still apply.

The EUDR applies to raw materials as well as to intermediate and end products made from them, provided they contain the listed materials and are made available on the EU market for the first time. Internal processing is not automatically "new placing on the market"; it is particularly relevant if this results in a new Annex I product and this is subsequently placed on the market or exported.

Imports from third countries are a typical trigger because the first operator must carry out due diligence and a DDS when accessing the market for the first time (usually after release for free circulation). No new DDS is usually required for intra-EU acquisitions if one already exists, but there may still be documentation and reference obligations for downstream operators/traders. In addition, the export of relevant products from the EU can also trigger EUDR obligations.

Yes, such own uses can be EUDR-relevant if the company as first operator transfers the goods from a third country into free circulation and thus makes them available on the EU market for the first time. Due diligence, DDS and evidence are then required, even without a sale.

If goods are released for free circulation from a third country and are thus made available on the EU market for the first time, the obligations apply even if they are exported later. If, on the other hand, a pure customs procedure without free circulation takes place (e.g. transit/customs warehouse/inward processing), there is typically no placing on the market; however, obligations may become relevant upon export or when a new Annex I product is created, depending on the constellation.

A product is "placed on the market" when it is made available on the Union market for the first time. In the case of imports, it is usually decisive that the goods are released for free circulation under customs law. A mere transit or storage under certain customs procedures (e.g. bonded warehouse) does not typically trigger this.

The core obligations do not differ for the first operator: due diligence, risk assessment and DDS are required regardless of whether the product is sold or used internally. For downstream operators (downstream/traders), on the other hand, the focus is usually on documentation/reference obligations; a separate DDS is often not necessary.

Downstream movements within the EU do not generally constitute a new placing on the market. Depending on the role, however, retention and transfer obligations (e.g. DDS references) remain in place. New operator obligations may arise if a new Annex I product is created through processing and this is placed on the market or exported.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.