Important facts

- What is the GHG protocol?

- The Greenhouse Gas Protocol (GHG Protocol) is the globally recognized standard for recording and reporting greenhouse gas emissions for companies.

- What are emission scopes?

- Emission scopes are categories used by the GHG Protocol to systematically classify a company's direct and indirect greenhouse gas emissions.

- Which scopes do companies need to record?

- According to the GHG Protocol, Scope 1 and Scope 2 are mandatory, while Scope 3 was previously voluntary.

- Which scope is most relevant for companies?

- Scope 3 accounts for the largest share of the corporate carbon footprint in most industries and is therefore essential for a complete climate strategy.

- What is Scope 4?

- Scope 4 covers so-called avoided emissions. In other words, the positive climate contribution that a company enables others to make through its products or services.

Abstract

The GHG Protocol is the international standard for recording greenhouse gas emissions and divides them into Scope 1, 2 and 3 emissions. Scope 1 covers direct emissions from the company's own sources such as vehicles or heating systems. Scope 2 coversindirect emissions from purchased energy such as electricity or district heating. Scope 3 covers all other indirect emissions along the value chain, from raw material extraction to product disposal at the customer. Although Scope 3 is the most complex category, it accounts for the largest share of the climate footprint in most sectors.

Scope 4 is also becoming increasingly relevant, i.e. the emissions that are not even produced by others thanks to the company's own products or services. There are no uniform standards for this yet, but interest is growing, especially among companies whose core business actively contributes to reducing emissions.

Climate change and corporate responsibility

Risks and opportunities for companies

Climate change is no longer an abstract issue for the future, as it now has a direct impact on business decisions. Companies are confronted with a broad spectrum of risks, ranging from physical damage to regulatory and reputational challenges.

Physical risks: Extreme weather events such as heatwaves, floods and droughts are on the rise. This is no longer a forecast, but a reality. This means problems for companies: production facilities can be damaged, supply chains can break down and operations can come to a standstill. And it's not just about short-term events, because long-term changes such as rising sea levels also hit entire industries with full force.

Regulatory risks: The legal requirements relating to emissions are becoming stricter. Companies are increasingly feeling the effects of this in their day-to-day business. CO₂ pricing makes emissions-intensive processes directly more expensive. In addition, the CSRD is forcing more and more companies to report transparently. Those who ignore this will pay the price: either through penalties or because they simply lose touch with market standards.

Reputational risks: Customers, investors and business partners are taking a closer look today than they did a few years ago. Sustainability is no longer a nice-to-have; it influences purchasing decisions, lending and the choice of suppliers. Companies that cannot demonstrate a credible climate strategy lose trust. And, as we all know, trust is easier lost than won back.

Companies are affected by climate change on three levels: physical, regulatory and reputational. Those who act early can turn risks into competitive advantages.

But climate change does not only entail risks. Companies that act early and invest in climate-friendly technologies, processes and business models can gain real competitive advantages. They open up new markets, reduce their operating costs in the long term and strengthen their resilience to future regulatory tightening. Strategic and forward-looking climate management is therefore not just a cost factor, but a lever for sustainable growth and long-term competitiveness.

Greenhouse gases and their impact on the climate

A basic understanding of greenhouse gases and how they work is essential in order to understand the impact of business activities on the climate.

Greenhouse gases (GHGs) play a central role in the Earth's climate system. They form a natural protective layer around the planet that stores the sun's heat and prevents it from escaping completely into space. This so-called greenhouse effect ensures that the Earth's average surface temperature is around 15 °C and thus makes the basis for life as we know it possible in the first place.

Since the beginning of industrialization, however, humans have significantly disturbed this natural balance. Through the massive burning of fossil fuels such as coal, oil and natural gas, as well as large-scale deforestation, far more greenhouse gases are released into the atmosphere today than natural processes can break down. According to the sixth assessment report of the Intergovernmental Panel on Climate Change (IPCC), the climate has warmed to an extent that has not been observed for around 2,000 years.

Greenhouse gases keep the earth warm. However, since industrialization, human activities have dangerously upset this balance.

The most important greenhouse gases in the corporate context

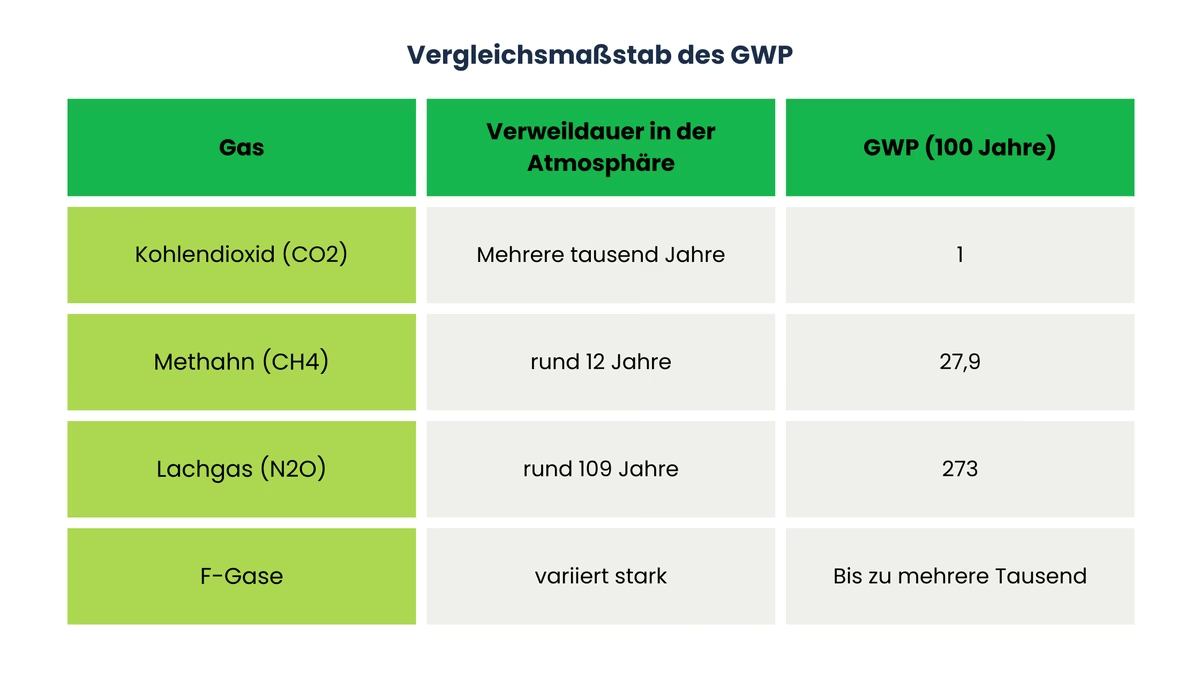

Carbon dioxide (CO₂) is the most significant man-made greenhouse gas in terms of quantity. It is mainly produced through the burning of fossil fuels and the clearing of forests. CO₂ remains in the atmosphere for several thousand years and serves as a reference value for the assessment of other greenhouse gases.

Methane (CH₄) is mainly released by agricultural activities, especially livestock farming, and by the decomposition of organic materials in landfills and wetlands. Although methane has a significantly shorter residence time in the atmosphere (around 12 years) than CO₂, its climate impact is around 27.9 times greater in a 100-year comparison.

Nitrous oxide (N₂O) is mainly produced in agriculture, for example through the use of nitrogen-rich fertilizers, as well as in various industrial processes. It remains in the atmosphere for around 109 years and is 273 times more potent than CO₂. This makes it one of the most powerful greenhouse gases.

Fluorinated gases (F-gases) include hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF₆). They are used in industrial applications such as refrigeration systems or switchgear and have an extremely high global warming potential, which, depending on the compound, is several thousand times higher than that of CO₂.

The Global Warming Potential (GWP) as a benchmark

As the various greenhouse gases contribute to global warming to different degrees and remain in the atmosphere for different lengths of time, the concept of global warming potential (GWP) was developed. It enables a standardized comparison of the climate impact of individual gases over a defined period of time, usually 100 years. CO₂ serves as a reference value with a GWP of 1.

Based on the GWP, all of a company's emissions are converted into CO₂ equivalents (CO₂e). This uniform indicator forms the basis for the corporate carbon footprint (CCF), i.e. the total of all direct and indirect greenhouse gas emissions of a company.

Consequences of climate change and relevance for companies

The consequences of rising greenhouse gas concentrations have long been noticeable and they affect companies at very different levels. Extreme weather events are becoming more frequent, glaciers are melting and sea levels are rising. Coastal regions are coming under pressure, marine ecosystems are suffering from the increasing acidification of the oceans, which is directly affecting industries such as fishing and tourism. And habitats on land are also changing at a pace that poses enormous challenges for many ecosystems.

For companies, this means They are affected both directly by physical damage and indirectly by regulatory measures such as CO₂ pricing. Knowing and systematically recording your own contribution to these emissions creates the basis for targeted countermeasures to minimize risks and take advantage of opportunities.

Guide to the GHG protocol and Scopes 1-3

The GHG protocol

What is the GHG protocol?

The Greenhouse Gas Protocol (GHG Protocol) is the most widely used standard worldwide when it comes to recording and reporting greenhouse gas emissions. It was developed in 1998, jointly by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). The aim was to create a uniform and comparable basis for emissions accounting. The fact that it is now also recommended by the Global Reporting Initiative (GRI) is proof of this: It has long since established itself as a standard in corporate reporting.

The GHG Protocol covers all relevant greenhouse gases that are also regulated by the Kyoto Protocol, including carbon dioxide (CO₂), methane (CH₄), nitrous oxide (N₂O) and fluorinated gases. To ensure uniform comparability, all emissions are converted into CO₂ equivalents (CO₂e).

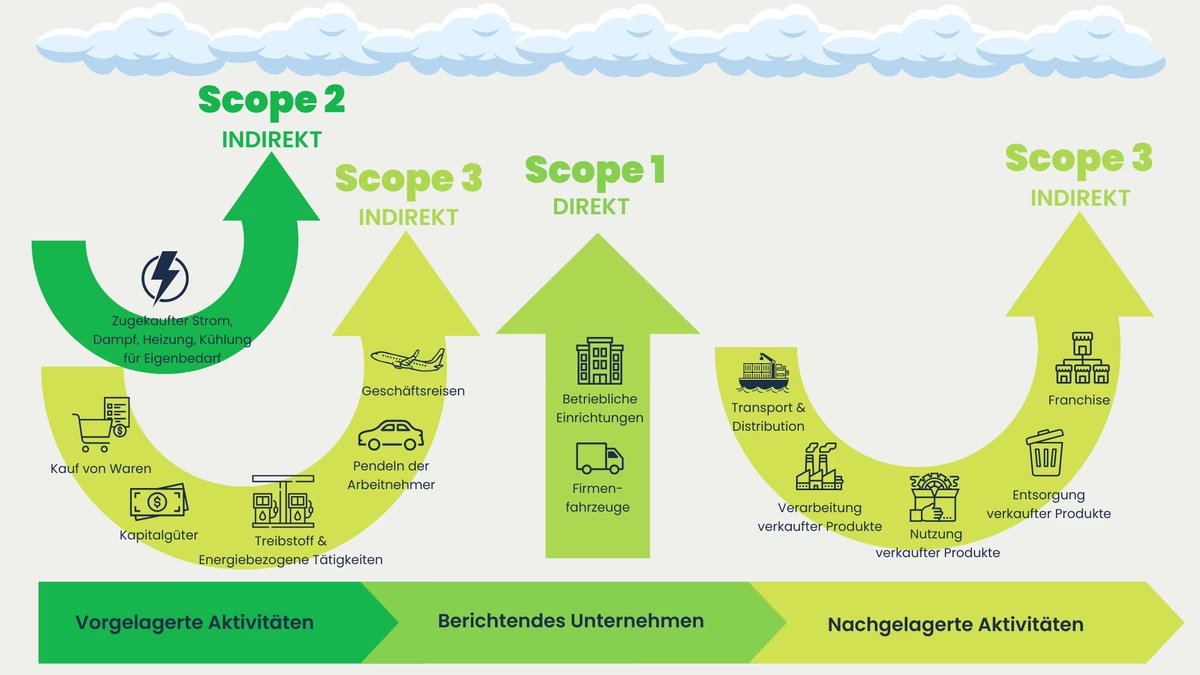

The actual core of the GHG Protocol is the classification of all emissions into three categories, the so-called scopes. This structure helps companies to understand, classify and target their emission sources.

- Scope 1 covers all direct emissions from company-owned or controlled sources.

- Scope 2 comprises indirect emissions caused by the consumption of purchased energy.

- Scope 3 includes all other indirect emissions along the entire value chain.

An important basic principle of the GHG Protocol is the distinction between direct and indirect emissions. Direct emissions are caused by what a company does itself, for example by operating its own facilities or vehicles. Indirect emissions are generated elsewhere, but are nevertheless related to the company's own business activities. Only by keeping an eye on both sides can you get a truly complete picture of your emissions balance.

The Corporate Carbon Footprint (CCF) represents the total of all direct and indirect greenhouse gas emissions (GHG emissions) of a company. It provides information on where emissions are generated in the operating processes and the value chain and to what extent. On this basis, specific reduction targets can be defined and measures prioritized.

What does the GHG Protocol expect from companies?

Scope 1 and Scope 2 are mandatory, the GHG Protocol leaves no doubt about that. The reason is simple: the data required for this, such as fuel consumption or energy bills, is already available in most companies. The effort required to collect this data is therefore limited, which makes these two categories a good introduction to emissions accounting.

Although the recording of Scope 3 emissions is not mandatory under the GHG Protocol, it is playing an increasingly central role in comprehensive climate protection strategies. The reason for its voluntary nature to date lies in its complexity: Scope 3 encompasses a large number of actors and processes along the entire value chain, which makes data collection considerably more difficult. Supplier data is often incomplete, methods are not standardized and the effort required for complete data collection is considerable.

Scope 1 and 2 are mandatory. Scope 3 was previously voluntary, but is becoming a mandatory requirement for more and more companies as a result of the CSRD.

Nevertheless, hardly any company can avoid Scope 3. At least not if it really wants to understand its corporate carbon footprint. In many industries, this is where the largest share of emissions is to be found. Anyone who ignores Scope 3 is simply ignoring reality. And with the CSRD at the latest, what was previously voluntary will become mandatory for many companies anyway.

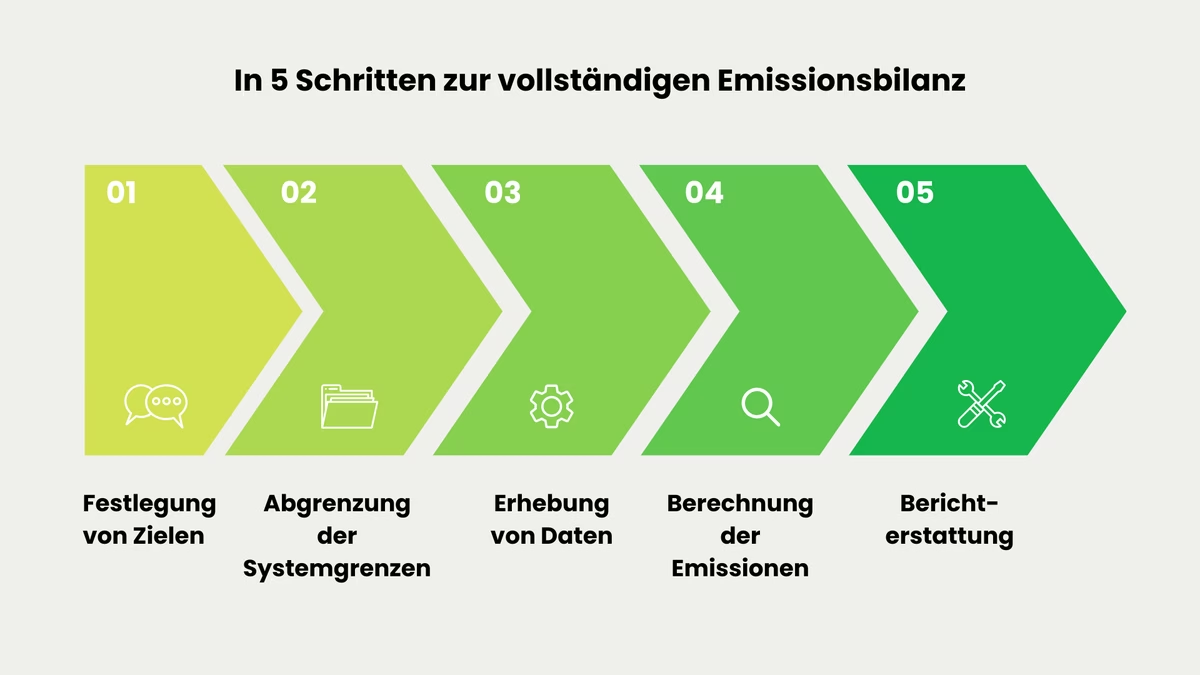

The GHG Protocol recommends a clear five-step process for drawing up a complete emissions balance sheet:

- Objective

- Delimitation of the system boundaries

- Data collection

- Calculation of emissions

- Reporting.

It sounds like a lot at first, but in practice it helps enormously to proceed in a structured manner and to end up with results that also stand up to external scrutiny.

Regulatory framework: CSRD & ESRS E1

With the introduction of the Corporate Sustainability Reporting Directive (CSRD), the European Union has fundamentally tightened the requirements for sustainability reporting. The directive came into force on January 5, 2023 and replaces the previous Non-Financial Reporting Directive (NFRD), which had applied to companies with more than 500 employees since 2014. The CSRD considerably expands the group of persons subject to reporting requirements and significantly specifies the content requirements.

In future, reporting must be included in the management report in accordance with the European Sustainability Reporting Standards (ESRS). The ESRS E1 Climate Change is particularly relevant for emissions: It obliges companies to fully disclose their Scope 1, Scope 2 and Scope 3 emissions. Incidentally, a rough estimate is not enough here. The figures must be methodically determined, comprehensible and externally verified.

Who is affected?

The EU Commission's Omnibus I package has fundamentally changed the original deadlines and thresholds of the CSRD. In future, only companies with more than 1,000 employees and an annual turnover of more than 450 million euros will be required to report - this means that an estimated 80% of the companies originally affected will no longer be covered.

The current deadlines at a glance:

- Wave 1 - Capital market-oriented companies with more than 500 employees that were already subject to the NFRD: No change, reporting obligation continues to apply from financial year 2024.

- Wave 2 - Large companies with more than 1,000 employees and over 450 million euros in annual revenue: reporting obligation postponed to financial year 2027.

- Wave 3 - Listed SMEs: Reporting obligation postponed to financial year 2028.

The EU amendments still have to be transposed into national law. Until this is done, the NFRD will continue to serve as the basis. However, it is expected that Germany will largely adopt the new EU requirements on a one-to-one basis.

Scope 1: Direct emissions

Definition and examples

Scope 1 emissions are a company's direct emissions. These include everything that is produced by the company's own facilities, processes or vehicles. In short, anyone who burns fuel or operates machinery is directly responsible for these emissions. Not a supplier, not an energy provider, but the company itself.

Typical sources of Scope 1 emissions are:

Boilers, ovens, generators or industrial production plants that are operated with fossil fuels such as natural gas, heating oil or coal.

The entire company fleet - from cars and delivery vans to trucks, forklift trucks and special vehicles - falls into this category if it is powered by fossil fuels.

In certain industries, greenhouse gases are not produced through combustion, but as a direct by-product of chemical or physical processes. A well-known example is cement production, where large quantities of CO₂ are released through the conversion of limestone.

Leaks in air conditioning or refrigeration systems release fluorinated gases, which have a much higher global warming potential than CO₂ and can therefore contribute significantly to the emissions balance despite small quantities.

Methane emissions from livestock farming, nitrous oxide from fertilizers and the combustion of biomass are also direct emissions from agricultural operations.

The specific sources of emissions vary considerably depending on the sector. In the manufacturing industry, combustion processes in production plants dominate, while in the service sector, heating systems and company vehicles are particularly relevant. In the energy industry, Scope 1 emissions arise directly from the combustion of fossil fuels in power plants and from the extraction and processing of crude oil, natural gas and coal.

Calculation and challenges

In principle, there are several methods available to companies for recording and calculating Scope 1 emissions:

- Direct measurement: The use of measuring devices for continuous monitoring of emissions directly at the source offers the highest accuracy. However, this method is technically demanding and involves considerable investment costs, which is why it is mainly used in emission-intensive industries.

- Activity data and emission factors: The most widely used method. Consumption data, such as fuel consumption, is multiplied by standardized emission factors in order to calculate the resulting greenhouse gas emissions. This approach is based on recognized standards such as the GHG Protocol and is practicable for most companies.

- Mass balance approach: In the chemical industry in particular, the quantity of emissions is determined by comparing the input and output quantities of a process.

- Modeling: Computer-aided models estimate emissions on the basis of process parameters and operating conditions. This is particularly useful when direct measurements are not possible.

However, companies face a number of challenges when collecting data. Consumption records are often not standardized or incomplete, meaning that a precise database must first be established. Added to this is the large number of possible emission sources: Heating systems, production facilities and vehicle fleets require different measurement or estimation methods, which makes data collection complex. Older companies often lack the technical infrastructure to measure emissions directly or document consumption in detail.

For smaller companies, the cost of implementing suitable measurement systems or software solutions can also represent a significant hurdle. Finally, in complex corporate structures with several locations or subsidiaries, there is a risk of double counting or unintentional omissions when allocating emission sources.

Reduction strategies

As companies have direct control over Scope 1 emissions, there are particularly effective levers for reduction here. At the same time, many measures go hand in hand with efficiency gains and long-term cost savings.

This can be changed to reduce the scope 1

Replacing fossil fuels with renewable energy sources is one of the most effective approaches. This can be achieved by installing your own solar systems, using heat pumps or using biogas as an alternative energy source. There is often considerable potential for savings here, particularly in the heat supply of buildings and production facilities.

The gradual conversion of the company's own fleet to electric vehicles reduces direct emissions from transportation enormously. In combination with self-generated green electricity, emissions in this area can be significantly reduced.

By modernizing systems, optimizing production processes and using energy-efficient technologies, energy requirements and therefore fuel consumption can be significantly reduced. Regular energy audits help to identify hidden savings potential.

Industry often has more potential in its own processes than is apparent at first glance. New technologies or a change in process management can significantly reduce process-related emissions without having to turn everything upside down. A good example is the cement industry, where intensive efforts are being made to replace emission-intensive clinker with alternative binding agents. This is a promising approach to tackling one of the most persistent sources of emissions in the industry.

This point is often underestimated, yet it is one of the simplest levers of all. If you regularly maintain your air conditioning and refrigeration systems and check them for leaks, you can prevent F-gases from escaping unnoticed. The effort involved is manageable, but the effect on the emissions balance is definitely noticeable.

If you know your Scope 1 emissions, you can reap the benefits several times over. The analysis shows where specific action can be taken. Those who do this early on are better prepared for upcoming regulatory requirements than the competition. Being a pioneer in sustainability is not only good for the conscience, but increasingly also a tangible competitive advantage.

Scope 2: Indirect emissions

Definition and examples

Scope 2 emissions are not produced in the company's own operations, but rather in the generation of energy that a company purchases externally - i.e. electricity, district heating, district cooling or steam. Even if this technically happens elsewhere, these emissions are directly linked to the company's own energy consumption. They can therefore not be ignored, as they are a significant part of a company's own carbon footprint.

An important distinction: Anyone who generates energy themselves - for example via their own combined heat and power plant or a photovoltaic system on the company premises - records these emissions under Scope 1, not Scope 2. Scope 2 only applies to energy that is purchased externally. The same applies to energy suppliers that produce electricity in their own power plants and feed it into the grid: their emissions also end up in Scope 1, not Scope 2.

Important note on differentiation:

Emissions that occur before the energy even reaches the company - for example during natural gas extraction or due to line losses in the electricity grid - do not belong to Scope 2, but to Scope 3. The difference sounds technical, but it is definitely relevant for a clean emissions balance.

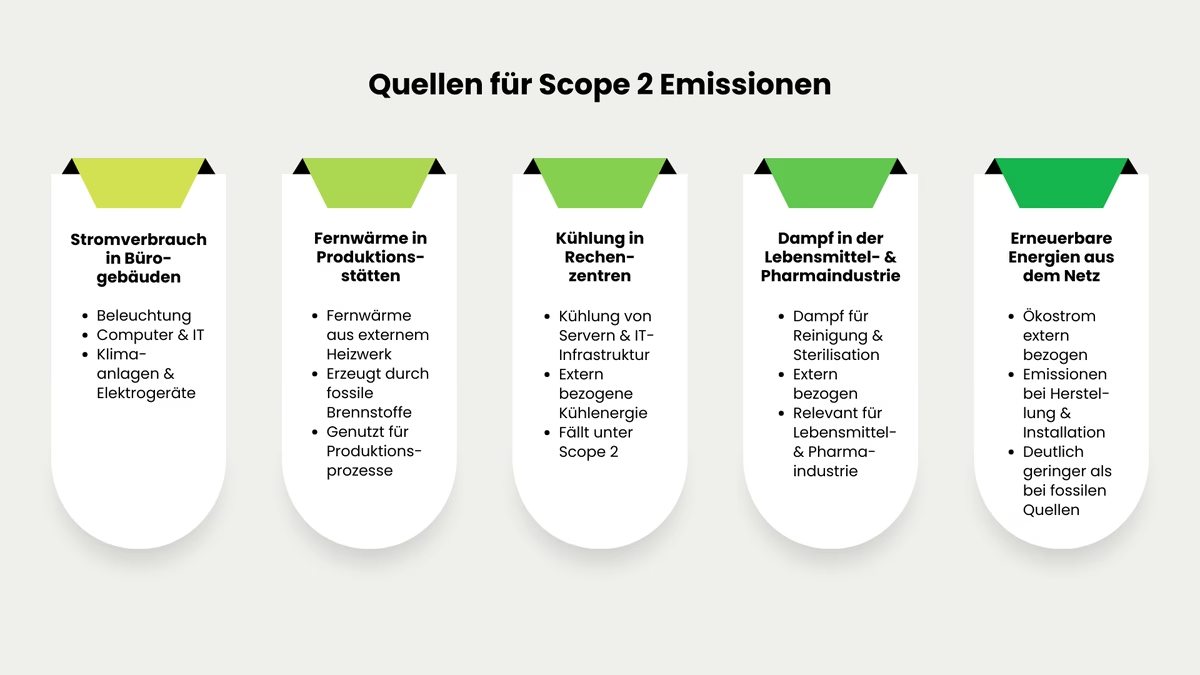

Typical examples of Scope 2 emissions

Lighting, computers, air conditioning systems and other electrical appliances cause indirect emissions that depend on the composition of the respective electricity mix.

If a manufacturer procures thermal energy via a district heating network that is generated in an external heating plant by burning fossil fuels, the resulting emissions count as Scope 2.

IT companies and data center operators require large amounts of energy to cool their server infrastructure. If this cooling energy is sourced externally, it falls under Scope 2.

In industries where steam is required for cleaning and sterilization processes and this is purchased from an external supplier, corresponding Scope 2 emissions are generated.

Companies that purchase electricity from renewable sources also have to deal with Scope 2 emissions. Although the operation of renewable energy systems is generally emission-free, greenhouse gases are produced during the production and installation of the systems. However, these are significantly lower than with conventional fossil energy sources.

Location-based vs. market-based approach

The GHG Protocol provides two methods for calculating Scope 2 emissions. It is recommended to use both and to report the results separately. This is the only way to obtain a truly complete picture.

Location-Based Method

The location-based method uses the average emission factors of the regional or national electricity grid. It reflects the actual emissions intensity of the electricity mix generated in the respective region. The calculation is made by multiplying the company's total electricity consumption by the corresponding emission factor. These factors are usually published and regularly updated by national or regional authorities.

The location-based method has the advantage that it is easy to use and is based on publicly available data. However, it does not provide any information on whether a company actively purchases green energy, as it only takes into account the average mix of the grid.

Market-Based Method

The market-based method, on the other hand, looks at what a company has actually purchased. Anyone who can prove that they have purchased electricity from a wind power plant and can prove this with a guarantee of origin or supply contract applies an emission factor of zero. If there is no such contract, so-called residual mix factors are used, i.e. the electricity mix that remains after deducting all certified renewable energies.

The market-based method thus gives companies a direct incentive to actively procure renewable energy and make this visible in their emissions balance sheet. However, it is more complex to apply and requires reliable evidence of the origin of the energy procured.

Both methods basically answer different questions. The location-based method shows how dirty or clean the regional electricity mix is. The market-based method shows which energy sources a company actively supports through its purchasing decisions. Both perspectives are valuable and together they provide a much more complete picture.

Reduction strategies

Companies have more control over Scope 2 than Scope 3, as the energy they purchase is a key factor here. Those who consciously opt for renewable energy sources can have a direct and tangible impact on their Scope 2 emissions.

This can be changed to reduce scope 2

One of the most effective measures for reducing Scope 2 emissions is switching to green electricity. By concluding electricity supply contracts with renewable energy sources - such as wind or solar parks - companies can significantly reduce their market-based emissions factor. Guarantees of origin and power purchase agreements (PPAs) provide a transparent and verifiable basis for this.

Anyone who installs solar panels on their own premises or uses other renewable energy systems generates their own electricity, which is emission-free. This not only reduces Scope 2 emissions, but also makes you less dependent on external energy suppliers. Especially in times of fluctuating energy prices, this is an argument that goes beyond sustainability.

Less consumption automatically means fewer emissions - that is the simplest equation in climate protection. More modern buildings, more efficient lighting, optimized production processes: All of this quickly adds up to tangible savings. If you don't yet know where to start, an energy audit is a good idea. It often shows surprisingly concretely where there is untapped potential.

Renewable alternatives are now also increasingly available in the heating and cooling sector. Heat pumps, solar thermal systems or the use of waste heat can reduce the consumption of fossil-fuel-generated district heating and thus improve the Scope 2 balance.

For many companies, the reduction of Scope 2 emissions is a comparatively controllable lever on the way to a comprehensive climate strategy. It not only reduces the ecological footprint, but also signals a serious commitment to climate protection to customers, investors and business partners.

Scope 3: Emissions along the value chain

Definition and the 15 categories

Scope 3 emissions are all indirect emissions that do not come from our own facilities or purchased energy, but from everything that happens along the value chain. In other words, from suppliers, transportation, the use of our own products by customers or their disposal. The company does not control these sources directly, but it does influence them through its decisions. The US Environmental Protection Agency (EPA) puts it in a nutshell: it is about emissions from facilities that the company neither owns nor operates, but which are nevertheless part of its value chain.

Although companies have no direct influence on Scope 3 emissions, they make up by far the largest share of the total corporate carbon footprint in many industries. If you want to understand your entire carbon footprint and develop effective reduction strategies, there is no way around Scope 3.

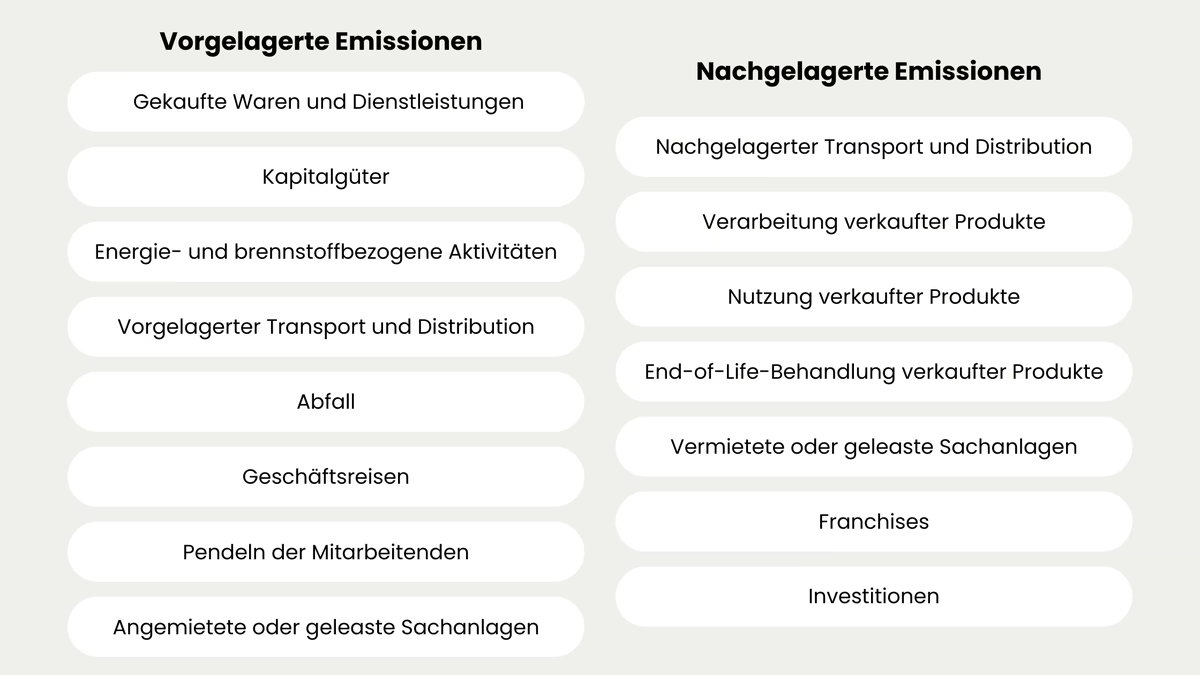

The GHG Protocol divides Scope 3 emissions into a total of 15 categories, which are subdivided into upstream and downstream emissions:

Upstream categories (upstream)

- Category 1 - Purchased goods and services: Emissions resulting from the production of raw materials, materials and services that a company purchases for its own production or operations. For many companies, this category has the greatest weighting of emissions within Scope 3.

- Category 2 - Capital goods: Emissions from the production of plant, machinery, buildings and other long-term capital goods that a company uses for its operations.

- Category 3 - Energy and fuel-related activities: Emissions that arise from the extraction, processing and transportation of fuels and from grid losses, i.e. all upstream processes that are not already included in Scope 1 or 2.

- Category 4 - Upstream transportation and distribution: Emissions from the transportation of raw materials, materials and goods from the supplier to the company, regardless of the mode of transport used.

- Category 5 - Waste: Emissions resulting from the disposal and treatment of waste generated as part of the company's own business activities, such as landfill gases or waste incineration.

- Category 6 - Business travel: Emissions from business travel by employees, regardless of whether by plane, train or car.

- Category 7 - Employee commuting: Emissions generated by employees' daily commutes between home and work.

- Category 8 - Rented or leased property, plant and equipment (upstream): Emissions from the operation of buildings, machinery or vehicles that a company leases or rents and that do not already fall under Scope 1 or 2.

Downstream categories (downstream)

- Category 9 - Downstream transportation and distribution: Emissions from the transportation of own products from the company to the customer or end consumer.

- Category 10 - Processing of products sold: Emissions generated when customers further process the purchased goods, for example through the use of energy in their production facilities.

- Category 11 - Use of products sold: Emissions generated during the use of products by customers or end users, such as the energy consumption of electrical appliances or vehicles in operation.

- Category 12 - End-of-life treatment of products sold: Emissions from the disposal or recycling of products at the end of their useful life.

- Category 13 - Property, plant and equipment rented or leased (downstream): Emissions from the operation of assets that a company rents or leases to other companies.

- Category 14 - Franchises: Issues arising from the business activities of franchisees operating under the franchisor's brand.

- Category 15 - Investments: Issues from the business activities of companies in which investments are made. This is particularly relevant for financial institutions, funds and investment companies.

Upstream and downstream emissions

The distinction between upstream and downstream emissions follows a clear logic along the product life cycle.

Upstream emissions occur before a product or service even reaches your own company. This includes everything from the extraction of raw materials to processing and delivery. In technical terms, this is known as the "cradle-to-gate" approach - from the cradle to the company gate. For manufacturing companies with global supply chains in particular, this area can be frighteningly extensive.

Downstream emissions, on the other hand, occur after the products have left the company, i.e. through transportation to the customer, their use and their disposal at the end of their life cycle. This approach is referred to as "gate-to-grave". For manufacturers of consumer goods or vehicles, the use phase by end customers in particular - category 11 - can represent the largest single item within Scope 3.

The interplay between the two areas makes it clear why Scope 3 is so complex and at the same time so important: although a company is not directly responsible for these emissions, it has a considerable influence on them through its purchasing decisions, product design and customer relationships.

Calculation and challenges

The GHG Protocol provides four recognized methods for quantifying Scope 3 emissions:

- Supplier-specific method: Emission data is provided directly by the suppliers. This method provides the most precise results, but requires close cooperation with the suppliers and assumes that they themselves have reliable emissions data.

- Environmental Economic Input-Output Analysis (EEIO): This estimates emissions based on economic input-output tables and average values. The method is useful when specific data is missing, but provides less accurate results.

- Hybrid method: A combination of supplier-specific data and EEIO average values. It combines the strengths of both approaches, but requires more effort to collect the data.

- Process-based life cycle analysis (LCA): This detailed method analyzes the emissions along the entire life cycle of a product or service. It offers the highest accuracy, but is also the most resource-intensive.

The biggest challenges in recording Scope 3 emissions lie in data availability and quality. Supplier data is often incomplete, not standardized or simply not available. Global supply chains with a large number of players make seamless traceability considerably more difficult.

Added to this is the considerable amount of human and financial resources required for a complete survey. Many companies are also faced with the question of which of the 15 categories are actually essential for their business model and where they should start collecting data.

The CSRD turns the previous voluntary nature of Scope 3 into an obligation for many companies. However, it is not mandatory to include all 15 categories, but only those that are classified as material for the company's own business model. Sounds like a relief, but it is still complex in practice. If you rely on external support here, you will save yourself a lot of effort and avoid costly mistakes.

Reduction strategies

Reducing Scope 3 emissions is not a task that one company can tackle alone. It requires a view of the entire value chain and cooperation with suppliers, partners and customers.

This can be changed to reduce scope 3

Those who select their suppliers specifically have one of the most effective levers for upstream emissions directly in their hands. Suppliers who pursue their own climate targets and are open about their emissions data have a clear advantage. Joint reduction targets, training and the exchange of proven approaches also help to make the entire supply chain more climate-friendly step by step.

Products that are more energy-efficient in use, last longer, are easier to repair or are easier to recycle at the end of their life reduce emissions in several downstream categories simultaneously. Product design is therefore one of the most effective levers for downstream Scope 3 emissions.

By analyzing and redesigning transport routes, bundling deliveries and using lower-emission modes of transport - such as rail instead of truck - both upstream and downstream transport emissions can be significantly reduced. The use of sustainable packaging materials also contributes to the reduction.

Companies can actively support their customers in using and disposing of products in a more environmentally friendly way by providing clear instructions for use, take-back systems or incentives for reuse. In this way, emissions in categories 11 and 12 can be reduced in a targeted manner.

Sometimes the biggest levers are in everyday life. Home office options, job tickets for local public transport or simply easily accessible bicycle parking spaces, all of which noticeably reduce emissions from daily commuting. And if you consistently replace business trips with video conferences where it makes sense, you also save time and travel costs.

Certified climate protection projects can be considered as a supplementary compensation measure for unavoidable Scope 3 emissions. However, this should always be seen as a last resort after all direct reduction potentials have been seriously exhausted.

Scope 4: Avoided emissions

Definition and relevance

In addition to the three established emission categories, another concept is becoming increasingly important: Scope 4, also known as "avoided emissions". While Scope 1 to 3 record the emissions that a company causes directly or indirectly, Scope 4 reverses this perspective: It measures the positive climate contribution that a company makes through its products or services, i.e. the emissions that are not generated elsewhere in the first place because innovative or more efficient solutions are used.

Specifically, it is about emissions that are not even generated by others thanks to the company's own products or services. Companies that develop energy-efficient technologies, provide renewable energies or offer low-emission mobility solutions help their customers to reduce their own carbon footprint. It is precisely these savings - not your own - that Scope 4 makes visible.

Important: Scope 4 is not a free pass for downscaling your own emissions. It does not change the values from Scope 1, 2 and 3 and should not do so. Scope 4 is an independent category that shows the positive contribution a company makes beyond its own borders. Similar to CO₂ offsetting, it is about completing the overall picture and not about calculating away unpleasant figures.

For companies whose business model is geared towards helping others to reduce emissions, Scope 4 is a real opportunity. At last there is a framework for not only claiming this contribution, but also quantifying it in concrete terms for customers, investors and the public. This creates credibility where previously there were often only promises.

Scope 4 emissions can be identified in almost all sectors.

Examples from practice

Anyone who produces and installs solar panels or wind turbines can calculate quite precisely how many emissions are avoided through their operation - compared to conventional electricity generation from fossil fuels. The logic behind this is simple: every kilowatt hour of renewable energy installed is a kilowatt hour that no longer has to come from coal or gas.

Providers of energy-efficient servers or data center components can measure the extent to which their products reduce their customers' energy consumption and therefore CO₂ emissions compared to older, less efficient technologies. In view of the rapidly growing energy requirements of the digital economy, this leverage is considerable.

Scope 4 is particularly tangible for car manufacturers who rely on electric vehicles. They can specifically calculate how much CO₂ their vehicles save compared to conventional combustion engines over their entire service life. These are impressive figures and make communicating your own contribution to climate protection much more credible than any general sustainability promise.

Better insulation, more efficient windows, smart control systems: it sounds unspectacular, but it has a measurable effect. Anyone offering such products can show exactly how much energy and CO₂ is saved. A comparison with conventional construction methods provides the figures. And they often speak for themselves.

A new fridge, a more efficient washing machine, hardly worth mentioning in everyday life. Yet you can calculate exactly how much electricity and CO₂ modern appliances save compared to older models. For manufacturers, these are strong arguments both for consumers who want to make conscious purchases and for investors who are looking at the sustainability profile.

The Covid-19 pandemic has shown what hardly anyone previously thought possible: A large proportion of business trips can easily be replaced by video conferencing. Providers of such platforms can calculate how many flights and journeys their services make superfluous and therefore how much CO₂ is saved. A Scope 4 contribution that can be quantified very concretely in many cases.

Less fertilizer, less fuel, the same or better yield. Anyone who achieves this with innovative cultivation methods or new fertilizer technologies can provide concrete evidence of the emissions saved as a result. Particularly in agriculture, where the use of resources and emissions are closely linked, this is a contribution that pays off for the environment and as an argument to customers and partners.

Current status of standardization

Scope 4 sounds convincing, but there is a catch. Unlike Scope 1, 2 and 3, there is currently no generally recognized standard according to which avoided emissions are uniformly accounted for. The concept is still in its infancy. Anyone reporting on Scope 4 today is on less secure ground in terms of methodology and must also communicate this transparently.

In practice, this means that if you want to report on Scope 4, you have to use existing frameworks and tailor them to your own situation. Many people resort to a life cycle analysis because it compares the avoided emissions with a clearly defined reference scenario. Sounds like a neat solution, but there is a catch: the choice of this reference scenario has a significant impact on the result. Different assumptions can lead to very different figures and this is precisely what makes Scope 4 so methodologically challenging.

If you still want to report on avoided emissions, you should take three things to heart: communicate openly which methods and assumptions were used, keep the calculations consistent from year to year and ensure that the figures can be verified externally. Only then will Scope 4 figures be more than just marketing - they will be credible.

Despite the lack of standardization, interest in Scope 4 is growing steadily, both on the part of companies and among investors and political decision-makers. Companies whose core business is geared towards reducing emissions have a legitimate interest in making this contribution visible. It is therefore to be expected that the development of more binding standards will continue in the coming years.

Conclusion

Recording greenhouse gas emissions is no longer an optional extra. Today, it is part of the mandatory program of every company that takes responsibility seriously. The GHG Protocol provides the framework for this and, with its classification into Scope 1, 2 and 3, ensures that emissions are not only visible at obvious points, but along the entire value chain.

Scope 1 and 2 form the mandatory entry point, Scope 3 is essential for an honest climate strategy and Scope 4 completes the picture with the question of what positive contribution a company can actively make. With the CSRD, the European legislator has also sent out clear signals: Those who act early gain valuable time to leverage reduction potential and secure competitive advantages. The first step begins with understanding your own sources of emissions, and this article is intended to help you do just that.

Frequently asked questions

The three scopes complement each other to form a complete picture of a company's climate impact: what is a Scope 1 emission for one company, such as electricity generation in a power plant, becomes a Scope 2 emission for the purchasing company. Emissions that are generated by suppliers as Scope 1 or 2 are in turn included in Scope 3 for the purchasing company.

The CCF is determined in a five-stage process: Objective setting, delineation of system boundaries, data collection, calculation of emissions based on activity data and emission factors and final reporting. All emissions are converted into CO₂ equivalents (CO₂e).

The difference lies in what is used as the basis for the calculation. The location-based approach simply takes the region's electricity mix, i.e. the average of what flows in the local grid. The market-based approach, on the other hand, looks at what a company has actually purchased. Those who can prove that they have purchased green electricity can apply an emission factor of zero. The GHG Protocol recommends calculating both values and reporting them separately. This provides a more complete picture.

Put simply, upstream means everything that happens before a product or service reaches your own company, for example the extraction of raw materials from the supplier or transportation to your own production facility. Downstream is everything that happens afterwards - how the customer uses the product and how they dispose of it at the end. Scope 3 therefore basically covers the entire life cycle of a product, far beyond your own four walls.

Not mandatory; under both the GHG Protocol and the CSRD, only those categories that are classified as material for the respective business activity must be reported. A materiality analysis helps to identify the relevant categories.

The GHG protocol recognizes four approaches - depending on what data is available. The most accurate option is to ask suppliers directly, but this requires their cooperation. If this data is not available, average values from economic input-output tables are used. Many companies combine both approaches in a so-called hybrid method. For very detailed analyses, there is also the life cycle analysis - time-consuming, but particularly precise.

The obligation applies in stages: Companies that are already subject to the NFRD will be affected from the 2024 reporting year. Large companies will follow from 2025, listed SMEs from 2026 - with the possibility of a deferral until 2028.

A pragmatic approach is to focus on Scope 1 and 2, as the database is usually available directly in the company. Energy bills, fuel consumption and fleet data form the starting point. For Scope 3, a step-by-step approach is recommended, starting with the categories that are essential for your own business model.

In practice, this takes place on several levels. Companies have their reports verified by independent auditors - often in accordance with ISO 14064. Authorities can impose sanctions in the event of false statements. And investors and ESG rating agencies are now also taking a very close look: Anyone working with inaccurate data quickly loses credibility.

Yes, definitely. If you know where your emissions are generated, you can take targeted countermeasures - and often save costs as well. What's more, customers, banks and business partners are increasingly asking for sustainability data, even outside of legal obligations. And those who only deal with the issue when the obligation arises simply have less time to act.

Larissa Ragg

LinkedInMarketing Managerin · lawcode GmbH

Larissa Ragg verantwortet die Content-Strategie bei lawcode und erstellt Fachbeiträge zu den Themen EUDR, ESG-Compliance, HinSchG, Supply Chain und CSRD. Ihre Beiträge auf dem lawcode Blog machen komplexe regulatorische Anforderungen verständlich und liefern Unternehmen praxisnahe Orientierung.